Rising catastrophe claims put fresh pressure on premiums, affordability and rebuilding plans

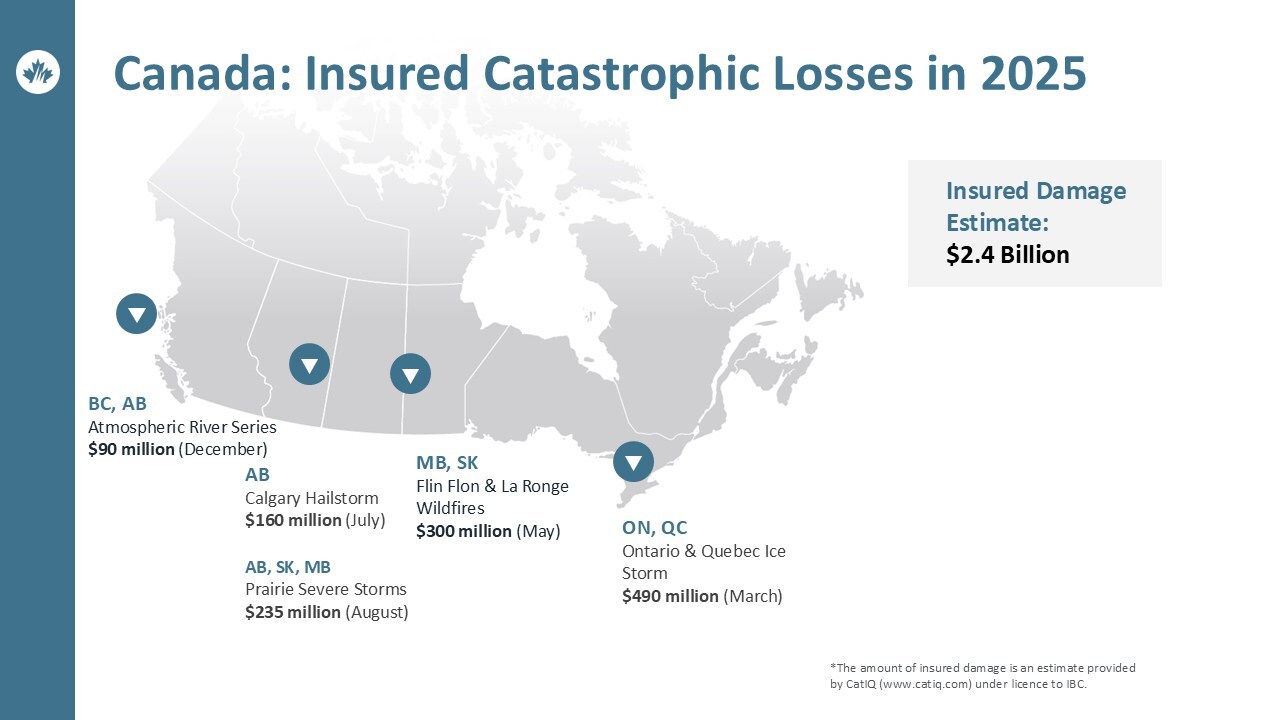

Insured damage from severe weather in Canada surpassed $2.4 billion in 2025, the tenth‑costliest year on record. New figures from Catastrophe Indices and Quantification Inc. (CatIQ) show how climate risk has become a structural issue for housing and mortgage markets, not just insurers.

CatIQ data showed 2025 losses were driven by a late‑March ice storm in Ontario and Quebec, wildfires near Flin Flon, Manitoba and La Ronge, Saskatchewan in May, a July hailstorm in Calgary, severe August storms across the Prairies, and December flooding in British Columbia.

The March ice storm alone caused an estimated $490 million in insured damage, with other named events pushing the total past the $2.4 billion mark.

Over the longer term, weather‑related insured losses has accelerated. Between 2006 and 2015, catastrophic weather and wildfire losses totaled $14 billion (inflation‑adjusted); from 2016 to 2025, that figure jumped to $37 billion, with claims volumes nearly doubling over the same period.

“Severe weather events continue to intensify. Two decades ago, insured losses seldom surpassed $500 million in a year. Today, annual costs exceeding $1 billion have become the norm. This shift demands that we fundamentally rethink how we build, plan and restore communities across our country,” said Celyeste Power, president and CEO of the Insurance Bureau of Canada (IBC).

“The best way to keep communities safe and insurance widely available and affordable is to invest seriously in resilience now.”

Calls grow for resilience as housing plan advances

IBC urged governments to tie Canada’s “historic” housing build‑out more closely to risk reduction.

“We must stop putting Canadians in harms way. As Canada embarks on a historic housing plan, investing in community and household resilience is significantly more cost‑effective than paying to rebuild following every disaster,” Power added.

“That’s why IBC and its members continue to urge governments at all levels to invest in infrastructure that defends against floods, adopt land‑use planning rules that ensure homes are not built on flood plains, facilitate FireSmart initiatives in communities in high‑risk wildfire zones, and implement long‑delayed changes to building codes that better protect homes and livelihoods.”

Mortgage affordability increasingly reflects climate exposure

Extreme weather‑driven claims has already pushed personal property losses to record levels and contributed to underwriting losses for Canadian home insurers in 2023 and 2024, with carriers paying out slightly more than they collected in premiums in those years.

Rising home insurance costs have increasingly eaten into mortgage capacity in high‑risk markets, with premiums in some wildfire‑exposed cities taking up close to a fifth of typical mortgage payments.

In Kamloops, BC, one of the cities facing the highest wildfire risk, insurance premiums nearly doubled between 2023 and 2025.

“The average annual insurance premium in Kamloops ($3,743) now works out to nearly a tenth of a typical mortgage payment on a home in the city, roughly five times the national average,” the joint report from Wahi and MyChoice found.

Four other cities—Prince George, BC, Timmins and Kenora in Ontario, and Lethbridge, Alberta—have seen insurance premiums exceed 10% of the average local monthly mortgage payment.

“Homeownership costs are no longer just about mortgage payments—climate risk is rapidly becoming a key financial factor,” said Aren Mirzaian, CEO of MyChoice.

“Our joint study with Wahi shows that in Canada’s wildfire-prone cities, insurance premiums are rising faster than home values, directly impacting housing affordability.”

The 2025 tally followed a record‑shattering 2024, when insured severe‑weather losses exceeded $8 billion nationwide and were nearly triple 2023 levels.

Make sure to get all the latest news to your inbox on Canada’s mortgage and housing markets by signing up for our free daily newsletter here.