Stalled demand and a long rate pause kept Canada’s housing reset in focus

TD Economics’ latest outlook painted a cooler picture for Canada’s housing market, even as it argued the Bank of Canada is likely to sit tight at a 2.25% policy rate.

Chief economist Beata Caranci said the mortgage “renewal cliff” has turned into “looking like a hill,” but warned that softer demand and regional imbalances still weighs on any recovery.

“Canadian average home price growth is likely to be closer to 1% rather than the 4% we expected in the December outlook, with tumbling condo prices being the main weight in BC and Ontario,” she said.

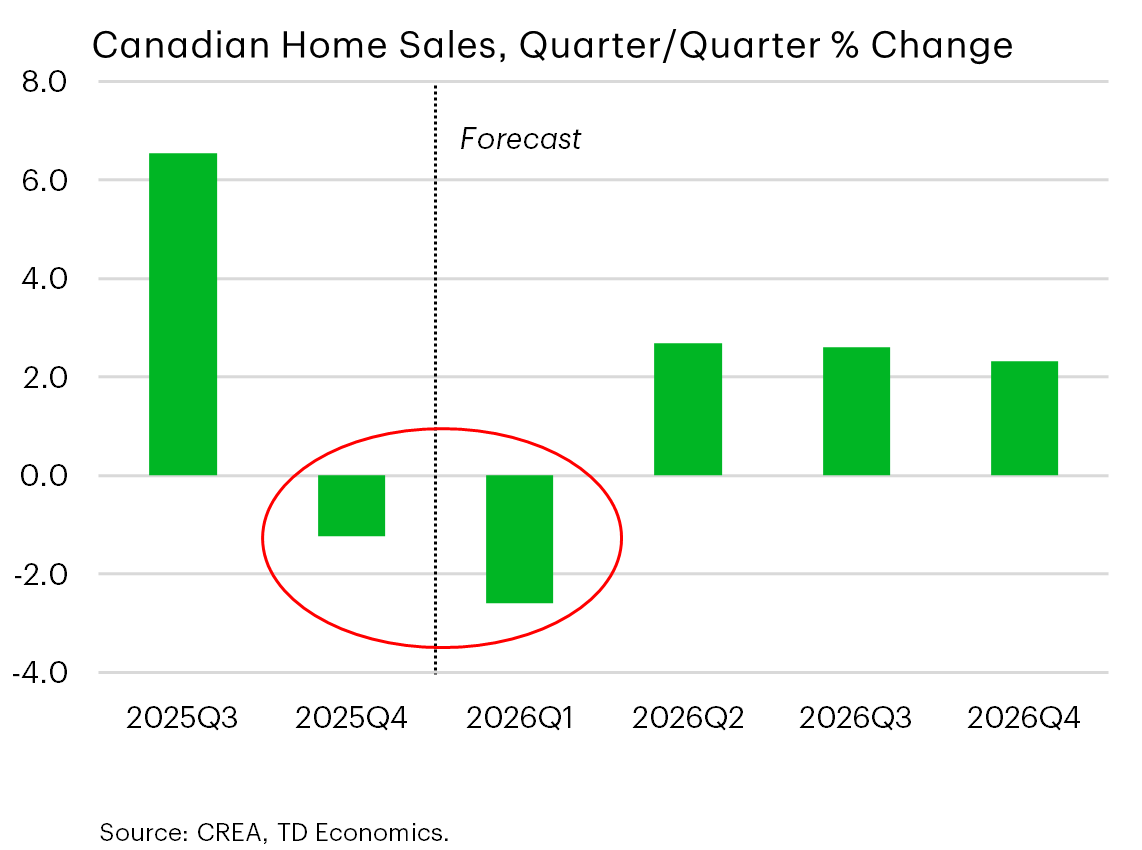

TD’s presentation showed home sales dropping sharply into late 2025 before only a “gradual and modest recovery” through 2026, with high inventory and slower population growth keeping a lid on gains.

BoC seen parked at 2.25%

Caranci said TD expected the Bank of Canada to “hold at 2.25% unless there’s a material and sustained deterioration in the job market that’s accompanied with an unemployment rate that breaches well above 7%,” adding that she was “thinking around 7.5% from the current level of 6.8%” as a trigger.

That view echoes a January Bank of Canada decision that kept rates unchanged and described 2.25% as “at about the right level” to support modest growth while keeping inflation near target.

Market surveys and major bank economists similarly projected a long pause through 2026, arguing the economy remained soft but not recessionary.

Still, mortgage professionals warned the January hold risks deepening a “housing slowdown” in Ontario and keeping renewal pain elevated for existing borrowers, even as national averages look manageable.

Meanwhile, BoC opened the door to future rate hikes even in a soft economy. In a speech in Oslo on Monday, deputy governor Sharon Kozicki said supply shocks such as United States tariffs, artificial intelligence and population aging pushed Canada into a new era where weak growth no longer guaranteed low interest rates.

Renewal shock cushioned, not cancelled

Behind the headline, TD highlighted how income growth and stretched amortizations have eased the feared payment spike. The report noted that the household debt‑service ratio already sat below its 2023 peak, with after‑tax income having grown “two percentage points faster than in the three years preceding the pandemic.”

Earlier TD research has also found that many borrowers have “moved away from the cliff edge” by refinancing early or increasing payments, reducing the need for “jumbo rate cuts” to rescue households.

Make sure to get all the latest news to your inbox on Canada’s mortgage and housing markets by signing up for our free daily newsletter here.