February data showed a quieter market as prices also fell

Canadian home sales edged lower again in February as buyers and sellers waited for clearer signals on interest rates and pricing, leaving activity subdued even as pressure from pent-up demand continued to build.

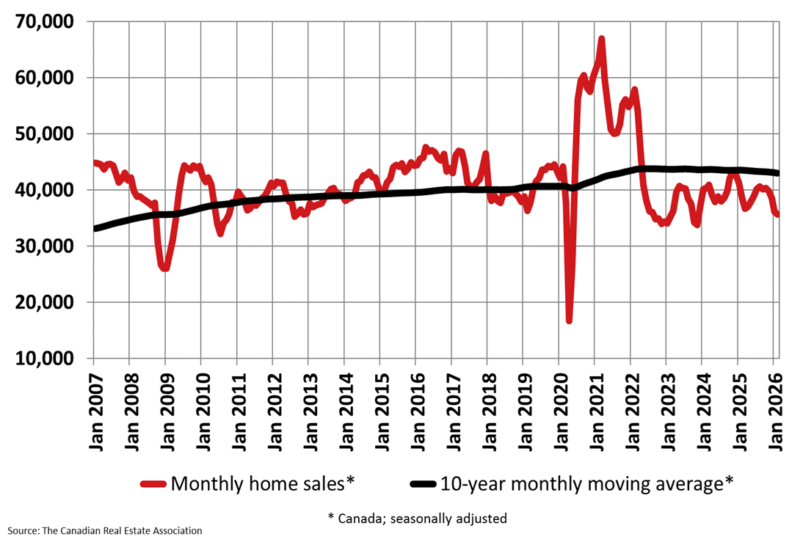

Data from the Canadian Real Estate Association (CREA) showed national home resales fell 1.3% month over month following January’s 5.8% decline.

Sales were 8.1% below February 2025 on an unadjusted basis, while the MLS Home Price Index dipped 0.6% from January and 4.8% year over year.

The national benchmark price stood at about $661,100, roughly in line with spring 2021 levels, and the sales-to-new listings ratio sat at 47.6%, well below its long-run average.

Pent-up demand stayed on the sidelines

“February saw a continuation of the quieter levels of activity recorded in January, although there was some indication things were starting to pick up speed toward the end of the month,” CREA senior economist Shaun Cathcart said.

“2026 is still ultimately expected to be a story about pent-up first-time buyer demand finally seeing a chance to enter the market. They’ve had to wait a long time for mortgage rates to find a bottom, but some will no doubt continue to hold off for a bottom in prices in some Ontario and British Columbia markets,” he said.

CREA chair Valérie Paquin said conditions in much of Ontario, particularly the corridor between Windsor and Toronto, remained slow.

“That said, the main event never really gets going until around April, so there’s still time to get ready to buy or sell this year,” she said. “Step one is getting in touch with a local REALTOR.”

Regional splits intensified

CREA’s figures showed price declines in British Columbia, Ontario and Alberta offset gains in other provinces, with markets such as St. John’s, Regina and Quebec City seeing stronger annual price growth.

In an interview with CBC News, economist Robert Hogue of RBC said home resales “are still fairly sluggish,” mainly in Ontario and B.C., “but we’re starting to see some moderation in other parts of Canada as well,” including Alberta and Quebec, where smaller and mid-sized markets had been hot in late 2025.

In earlier commentary, Hogue said the market might only “strengthen a little bit” later in 2026 as economic uncertainty eased, calling the outlook for the year “fairly kind of restrained” and highly dependent on sentiment and rates, he said.

Oxford warns the chill could last

Michael Davenport, senior Canada economist at Oxford Economics, said the latest figures underscore how entrenched the downturn has become, with sales having fallen for four straight months and the national benchmark price declining for 13.

New listings, he said, pulled back from January but remained above long-term norms, keeping months of inventory near a six‑year high and adding to downward pressure on prices.

“A spring thaw in Canada’s resale housing market looks unlikely,” Davenport said. “The labour market is deteriorating, trade policy and geopolitical uncertainty are elevated, and the population is shrinking, all of which will likely continue to weigh on housing demand and keep supply high in the coming months.”

“We expect house prices to fall further in the spring before finding a bottom around mid-year, thanks to a resumption of modest job growth, improved affordability, and fiscal stimulus that will increasingly support the economy in H2,” he said.

“However, there’s a growing risk that the slump in Canada’s housing market persists for longer. Prospects for a sustained pickup in resale housing hinge on the successful renegotiation of the USMCA that lowers tariffs and lessens trade policy uncertainty, and an early resolution to the US/Israel-Iran war,” he said.

Mortgage market looks to the Bank of Canada

Market participants now look to the Bank of Canada’s next policy decision, with many economists expecting a hold and some beginning to price in cuts later in the year after softer jobs data.

Resilient housing activity limits how aggressively the central bank could ease, tempering expectations for rapid rate cuts even as growth slows.

Any spring rebound is likely to be uneven, with Toronto and other major urban centres lagging regional markets and first-time buyers relying more heavily on extended amortizations and insured solutions to make purchases work.

Make sure to get all the latest news to your inbox on Canada’s mortgage and housing markets by signing up for our free daily newsletter here.