Occupancy low across Australian CBDs

Australia's commercial property sector is experiencing a stark performance divide, with industrial assets surging ahead while office markets struggle under the weight of elevated vacancies and shifting work patterns, according to CreditorWatch's latest industry report.

The industrial and logistics sector delivered total returns of 8.6% and capital growth of 4.1% in 2025, significantly outperforming office and retail categories. Transaction volumes in the sector reached $29.6 billion last year, representing a 44.9% increase from 2024, with Queensland almost doubling its volumes to $7.8 billion.

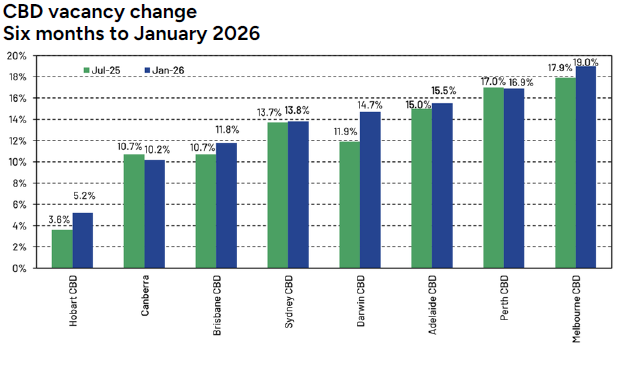

In contrast, office vacancy rates remain stubbornly high across Australia's major CBDs. National office vacancies increased from 15.2% to 15.9% in the six months to January 2026, with Melbourne recording the highest vacancy rate at 19%. Sydney CBD sits at 13.8%, while Perth stands at 16.9%, though market conditions are expected to tighten with no new supply anticipated for three years.

Credit: Property Council of Australia

"At the macro-level, recent interest rate rises along with March's energy price spikes, produce a more cautious outlook for commercial property," says Ivan Colhoun (pictured), CreditorWatch chief economist. "Within the sectors, the outlook for industrial remains strongest, supported by low supply and structural tailwinds reflecting both e-commerce, automation and now AI data centre demand."

Growth sub-sectors within industrial include cold storage facilities, last-mile logistics operations and data centres, each presenting distinct investment and leasing opportunities.

A structural shift

The performance gap is being driven by fundamental structural shifts in the Australian economy.

Industrial demand continues to be supported by e-commerce growth, supply-chain restructuring, and exceptionally low vacancy rates of approximately 2-3% nationally. The sector is also benefiting from AI and technology integration, with modern warehouses increasingly requiring enhanced power capacity, high-speed fibre connectivity, and sustainable energy infrastructure to support automated systems.

On the other hand, "office markets, except for the highest-rated buildings, generally remain somewhat challenged from prior oversupply and the sustained working-from-home phenomenon”, Colhoun notes. "Lower-grade buildings have considerably higher vacancy rates and often require considerable renovation or are demolished."

The challenging environment is reflected in business failure data, with arrears and payment defaults in office-heavy sectors including professional services, retail trade, and transport and logistics continuing to escalate through 2025.

A record 14,649 businesses become insolvent in 2025. Retail insolvencies recorded the third highest number of insolvencies at 1,010, followed by construction at 3,561 and accommodation and food services at 2,286.

Adding to the complexity, real estate professionals will face new compliance obligations from July 2026 when AML/CTF Tranche 2 regulations take effect, requiring comprehensive customer due diligence and beneficial owner identification.

The report highlights a pronounced "flight to quality" in office markets, with premium space filling faster than secondary stock. This trend is creating opportunities for repurposing secondary space for alternative uses such as residential or laboratory facilities.

Mixed-use sites gaining traction

Mixed‑use developments are rapidly gaining traction as landlords seek to future‑proof assets and smooth income in a volatile commercial market. Developers are increasingly converting or expanding single‑use retail and office properties to incorporate residential, hotel and community elements, creating resilient, amenity‑rich precincts that appeal to tenants, residents and investors alike.

Vicinity’s flagship project at Bankstown Central in Sydney’s west typifies the shift, with plans for 1,300 residential units, 226,000sqm of retail and commercial space, a hotel and student accommodation integrated into one master‑planned hub. Scentre Group is pursuing a similar strategy, rolling out a $4 billion pipeline to bolt office and residential components onto its Westfield centres.

“These developments require careful demand assessment across multiple asset classes but deliver significant opportunities for agents to provide comprehensive property services spanning residential, commercial, and retail sectors,” says the CreditorWatch report.