With payday super, CGT changes and rising SME issues reshaping the market, Connective's Brent Starrenburg says brokers who act now will separate themselves from the pack

The new financial year arrives on 1 July carrying more moving parts than most for commercial brokers.

Regulatory change, a cost-of-living squeeze on SME customers and a property market recalibrating around capital gains tax (CGT) and negative gearing reforms are creating a complex backdrop for commercial brokers.

For Brent Starrenburg (pictured), head of commercial and asset finance at Connective, the challenge is also an opportunity – but only for brokers putting the work in now.

"The smart ones are actually having the conversations with their clients now and setting them up to ensure that they don't run into cash flow problems, as opposed to waiting until there is a problem," Starrenburg said in an interview with MPA. "It's better to be prepared than to try and fix it after the fact."

The payday super problem

Nothing should be concentrating broker attention more sharply heading into EOFY than the federal government's payday super reforms. From 1 July, employers will be required to pay superannuation contributions at the same time as wages – a structural shift that eliminates the quarterly payment buffer most SMEs have relied on for years.

MPA reported in June that 60% of SMEs are confident they can remain cash flow positive over the next 12 months – down sharply from 70% in February – with nearly four in 10 heading into the 1 July deadline either unprepared or unsure.

According to Starrenburg, approximately 68% of SMEs “have made zero preparations for what that means for their cash flow”.

He said the problem stems from a fundamental shift in business rhythm. "Most of the time it was on a quarterly basis – you can build that up over time to have a buffer. With these changes, all of that disappears."

NAB executive, small business Olivia Brosca agreed that payday super timing mattered for how businesses managed their cashflow.

“This is a structural change to when payments are made, and, for some businesses, it will change the rhythm of money moving in and out,” Brosca said. “The earlier businesses understand the impact and plan for it, the more comfortable they’ll feel when the changes come into effect.”

The broker's role, in Starrenburg’s view, is not to give advice but to be the first call that prompts action. "We're suggesting brokers reach out and talk to their clients… to be there to help them structure cash flow lending accordingly to ensure that they've got the funds there to pay the super and not fall foul of any legislation in that space."

He outlined a range of structures available depending on the client's business: "That could be done through an overdraft facility, it could be done through a working cap facility where it's unsecured, but it could also be done through trade and debtor. There are a number of ways it can be done, depending on the type of business."

Asset and equipment finance: focused, not falling

Broader market data points to a challenging first half of 2026 for asset and equipment (A&E) lending. MPA's commercial lending report in May 2026 found that some lenders had deliberately prioritised deal quality over volume, targeting applications from more resilient sectors in a bumpy market.

Connective's experience differs slightly from that macro narrative. Starrenburg said the aggregator is up year-on-year in A&E, citing “a more challenging but also a more focused market”.

The businesses still investing, he said, are those with clear income-generating rationale, including agribusiness, manufacturing and automotive assets.

The consumer side of A&E is a different story. "With cost-of-living pressures, RBA announcements and fuel costs, we've seen a decrease in consumer lending,” said Starrenburg.

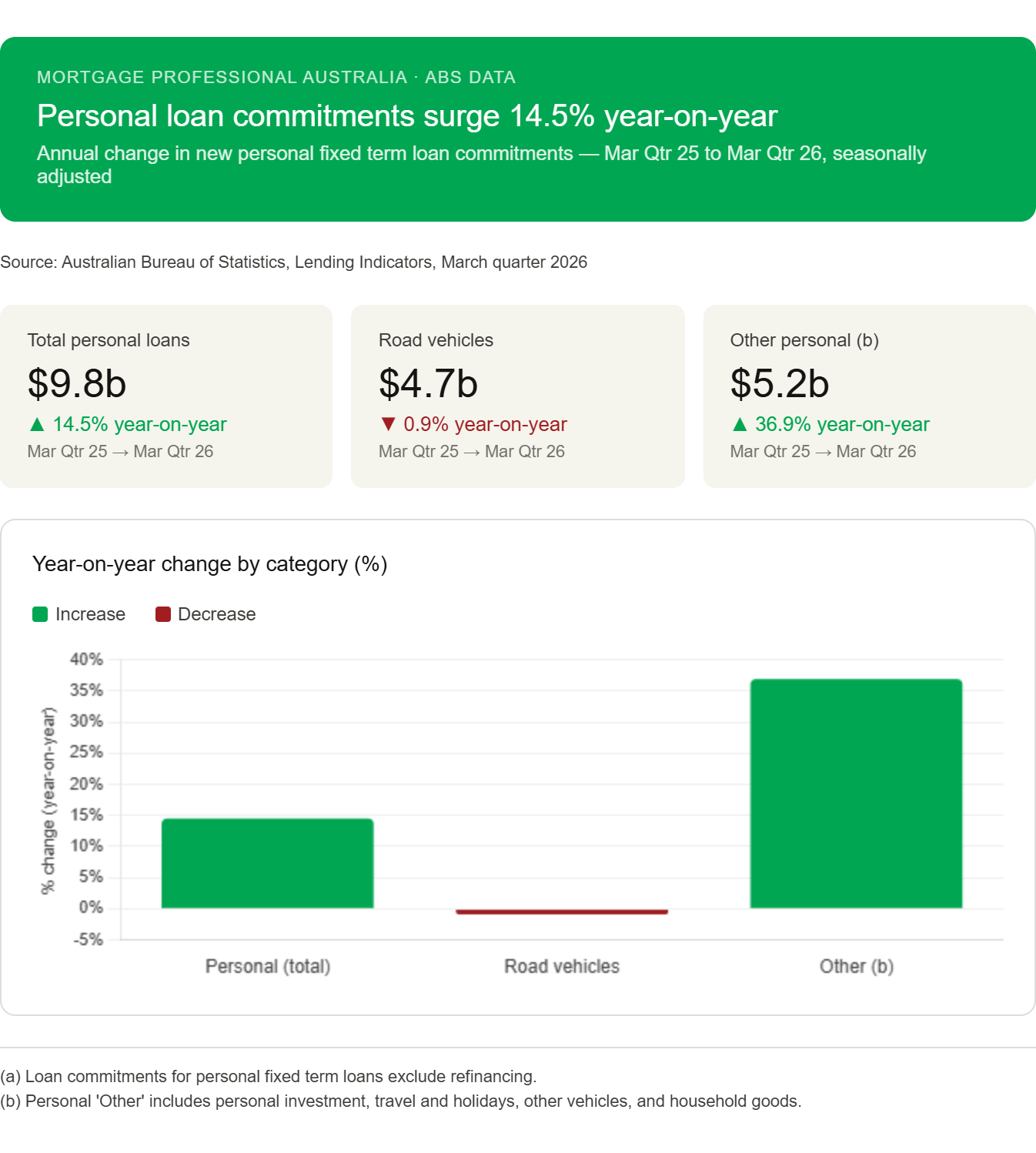

What concerns him more is an uptick in personal loan activity. Australian Bureau of Statistics (ABS) data shows a 14.5% uptick in new personal loan commitments in the quarter ending March 31. "To me, that points to financial stress – short-term credit card debt, consolidation, trying to tidy things up,” said Starrenburg.

He cautioned brokers to think carefully before rolling personal debt into home loans for clients. "Yes, it might be more affordable or manageable – but it's the most expensive way to do it over the long run."

According to Equifax chief solutions officer Kevin James, personal borrowing volumes could move even higher. He said: “With global uncertainty, supply chain disruptions, higher consumer borrowing rates and rising fuel prices, it is easy to suggest that we could expect to see a dramatic decrease in credit demand.

“However, it’s important to recognise that we can draw parallels to conditions consumers experienced in 2022 and 2023. The data demonstrates the resilience of Australia’s credit market, as long as factors such as unemployment remain low.”

Equifax data shows that personal loan arrears remain stable or even improving, with credit card 90+ days past due (DPD) delinquency rates down nearly 3% year on year in the March quarter.

Budget impacts and commercial property's new appeal

On the federal budget, Starrenburg noted mixed signals for SME clients – but a potential upside for commercial property as CGT and negative gearing changes reshape investment appetite.

"We might see a shift in demand for commercial, whether it be warehousing, offices or factories, with a decrease in appetite on the resi property side. I actually think (the Budget) could be a good thing for the commercial sector."

For brokers looking to capitalise, Starrenburg called on brokers to understand the client's business, not just their loan. "The biggest thing is to ask the right questions. If you're dealing with an SME, genuinely understand who they are, what they're doing, and what they're trying to do. What is in that business's growth plans for the next 12 to 24 months?"

He also flagged the budget's $20,000 permanent instant asset write-off and loss carryback provisions – which allow businesses to offset losses against two previous tax years – as potential tools for clients carrying Australian Tax Office (ATO) debt.

The fee model question

MPA recently reported that brokers are working harder than ever to get deals across the line amid growing policy uncertainty – raising questions about whether the current fee model reflects the full scope of broker work.

Starrenburg agreed that brokers are doing “a lot more ad hoc work that isn't revenue generating because there's no actual deal being made, including a lot more advisory, guidance-led work”.

He believes mandate letters and fee-for-service arrangements as the logical response, but stressed the need for brokers to earn those fees. "They can't just put out a mandate saying 'I'm going to charge you X thousand dollars' and then not give them anything in return for that. There's got to be something tangible that the client feels value in."

With payday super, a repriced commercial property market, and SME financial stress all converging, it sounds like the new financial year will reward those who have already had the conversations their clients haven't thought to ask for.