Jump to winners | Jump to methodology

As interest rates climbed and credit conditions constricted throughout 2024, a significant number of borrowers chose to hit pause. Yet New Zealand’s leading mortgage brokerages continued to forge ahead, demonstrating that resilience and client service remain the cornerstones of success in an increasingly volatile market.

Lending policies shifted constantly, yet these firms didn’t lose their footing, showing a remarkable ability to adapt. Rather than falter, they sharpened their focus, maintaining robust performance while ensuring that clients were not left adrift. By placing long-term decision-making at the heart of their advice, they reinforced the essential role of trusted brokers navigating uncertain financial waters.

“The number of consumers approaching advisers is very much on the increase, and increasingly, people appreciate the independent advice that an adviser can give,” explains iLender’s Jeff Royle, who earned the moniker “Financial Paramedic” for providing “first aid” to clients’ finances. “The real benefit to the consumer is that advisers are independent of a lending source, and their role is very much to match the product to suit the consumer.”

Across the country, the leading firms and their teams dealt with reduced liquidity, longer sales timelines, and clients facing more demanding lending criteria. Frequent changes to interest rates and serviceability rules meant eligibility could change within weeks.

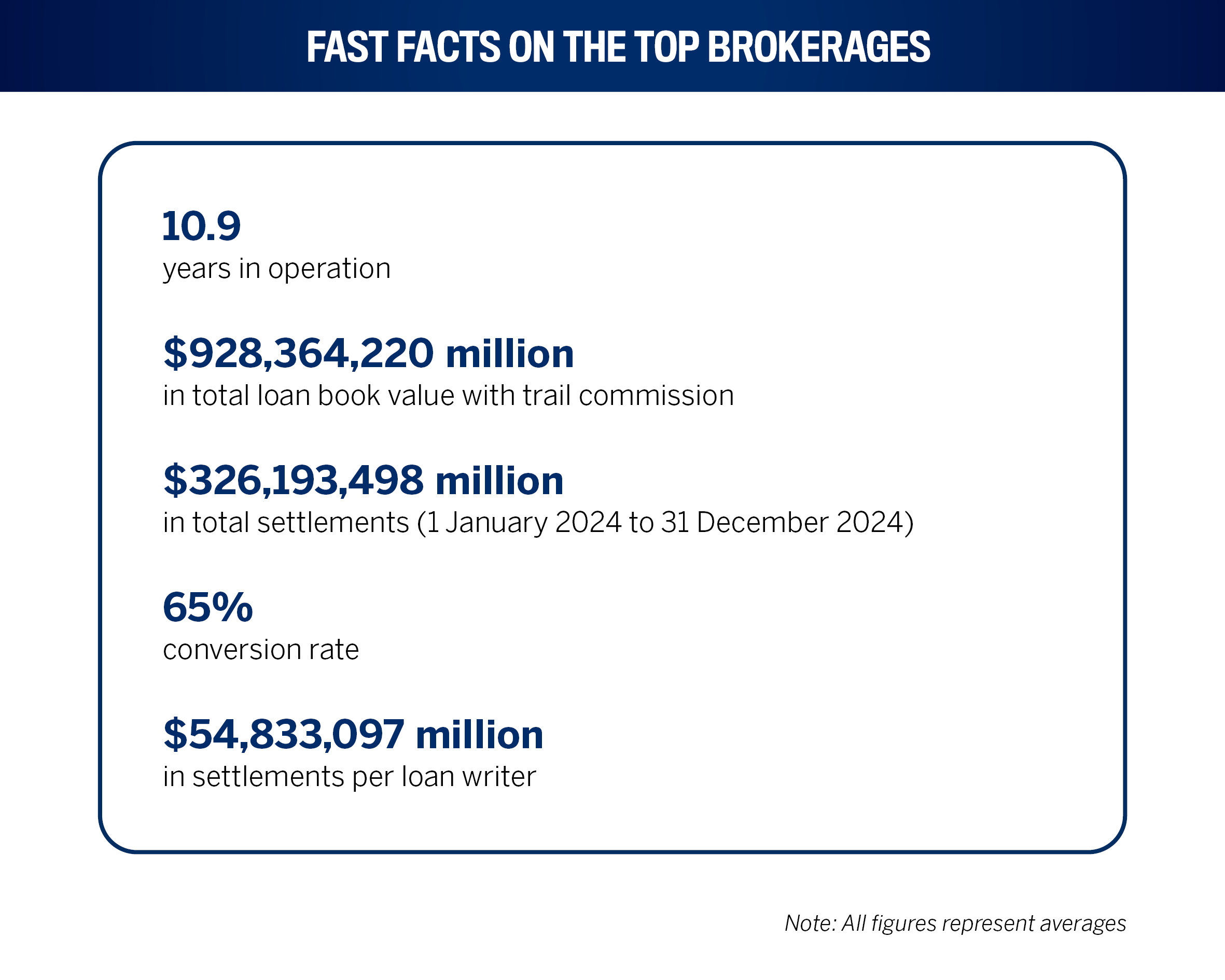

Despite this uncertainty, NZ Adviser’s 27 Top Brokerages of 2025 stand out for a few key reasons:

stayed close to their clients: from first home buyers to complex development deals, the best firms were thinking strategically, helping people make decisions that made sense. That level of care pushed the average conversion rate to 65%.

knew their stuff: many advisers came from banks, and they’ve kept learning. That collective knowledge translated into serious volume, with average loan books stretching well past the $900 million mark.

kept people in the loop: clients didn’t have to guess where things stood. These brokerages were known for regular check-ins, clear updates and solid communication all the way through. It’s part of why they were still closing strong, around $326 million a year, on average.

moved fast when things changed: rates jumped, serviceability rules shifted and the sales cycle slowed, but the top performers kept pace. Their teams stayed nimble, supported by good systems and strong internal workflows. Loan writers at these firms were still averaging more than $54 million each in settled volume.

On staying close to clients, Royle adds, “We’re not a transaction business; we don’t do a deal and say goodbye. We’re here long term, and we’ll be by their side to make sure everything’s on track.”

Regarding the importance of being nimble and solutions-driven, he speaks from firsthand experience as an expert in non-bank lending. “Our forte is when the bank says no,” says Royle. “Our role is about providing solutions, including short-term ones, to get them to where they want to go, and then the plan is always to get them back to the mainstream as quickly as possible.”

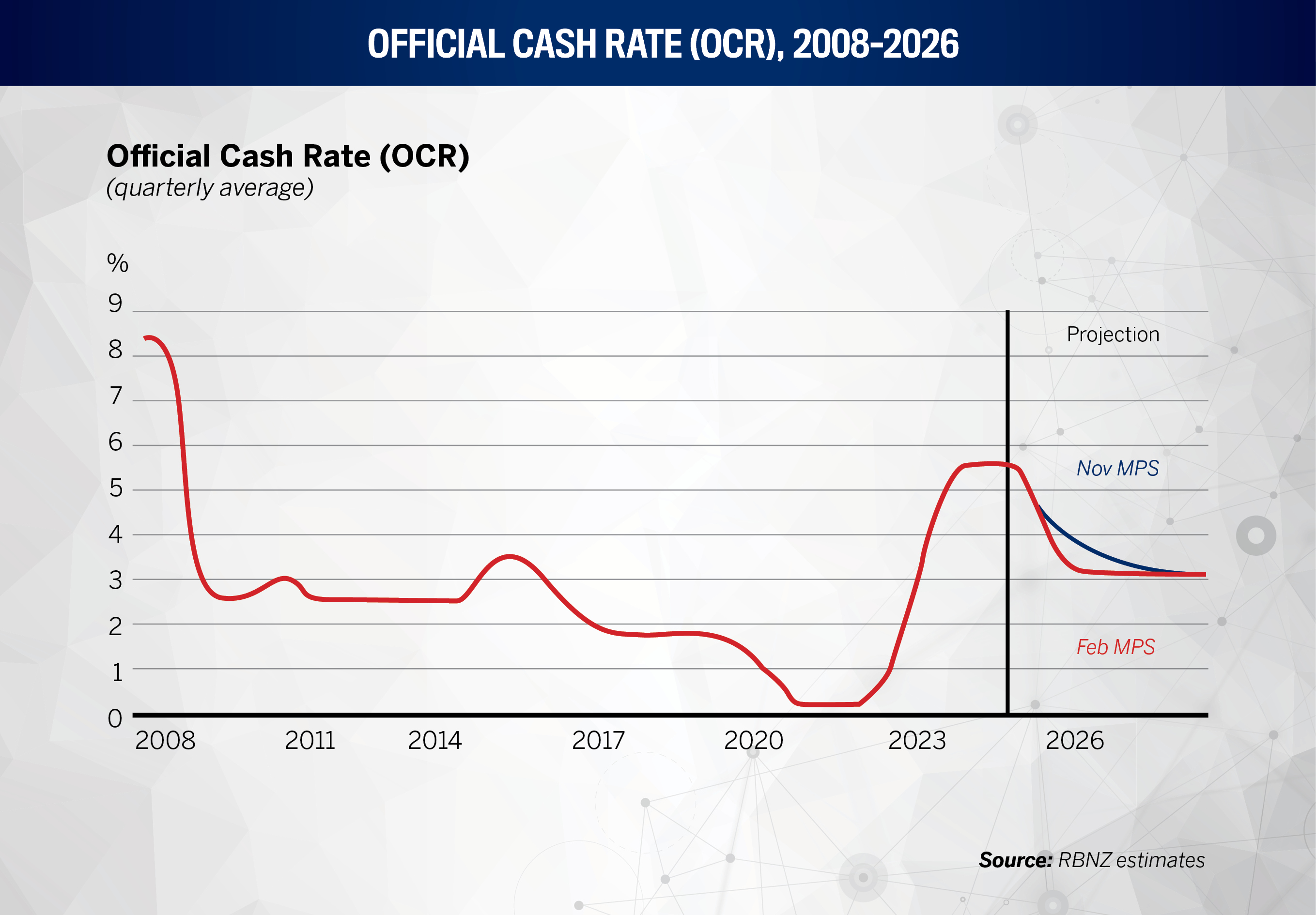

The Reserve Bank’s February and April 2025 statements outlined a lending environment still under pressure, but with cautious optimism building beneath it. After a steep GDP drop through mid-2024, driven by high interest rates and softened demand, mortgage activity slowed noticeably. But the best mortgage brokerage firms didn’t flinch. They remained committed to guiding clients through it.

Even as affordability tightened and borrowing power dropped, the top brokerages were still helping clients get across the line. They adjusted in a market where eligibility could shift month to month, and that kind of hands-on guidance became essential.

When the Reserve Bank cut the official cash rate again to 3.5% in April and signalled that more reductions could follow, the mood began to shift.

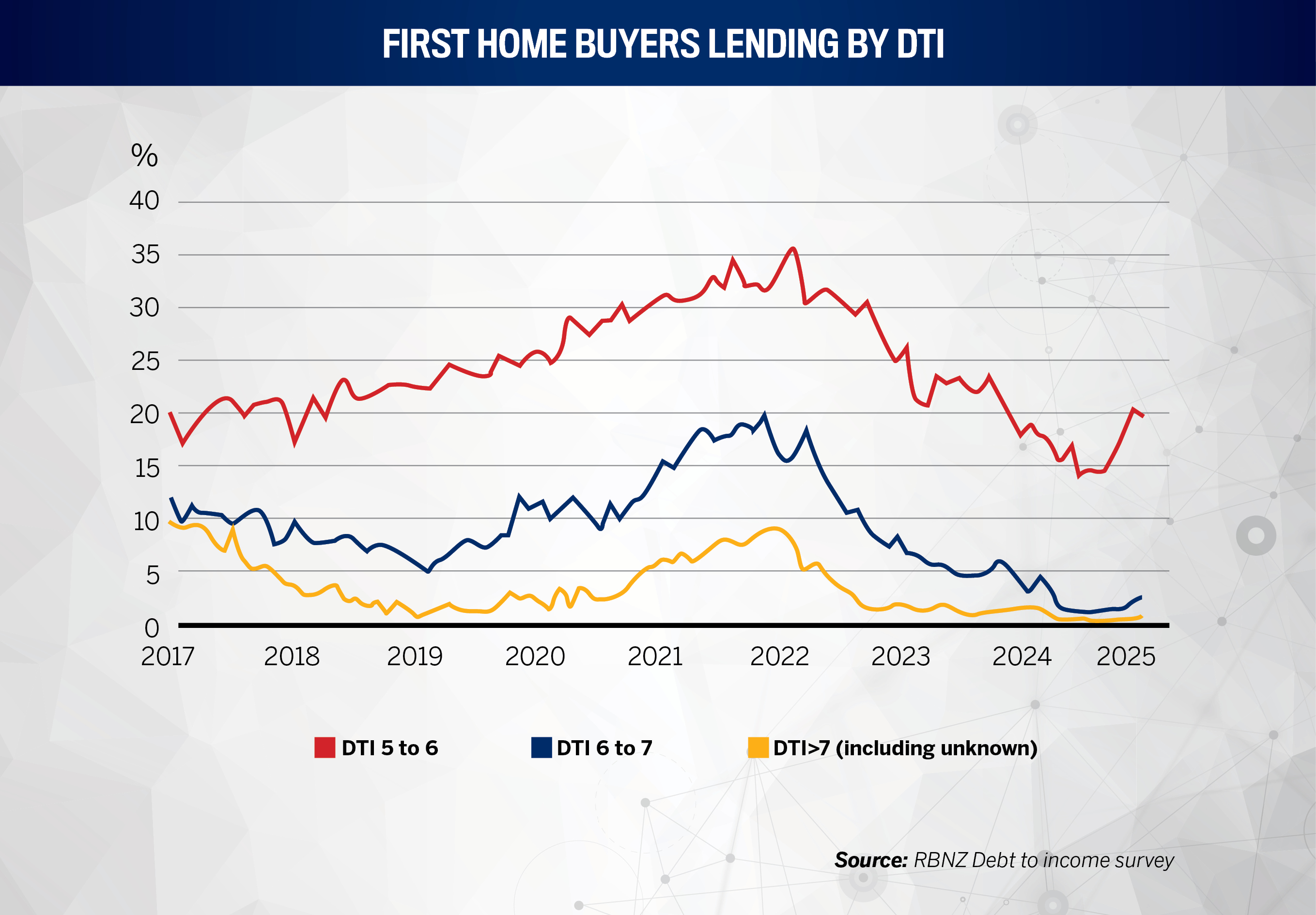

Mortgage professionals have played a big part in helping clients respond to the evolving policy space, particularly around debt-to-income limits. This has been especially critical for first home buyers, who now face stricter thresholds but are still finding ways forward with expert advice and support.

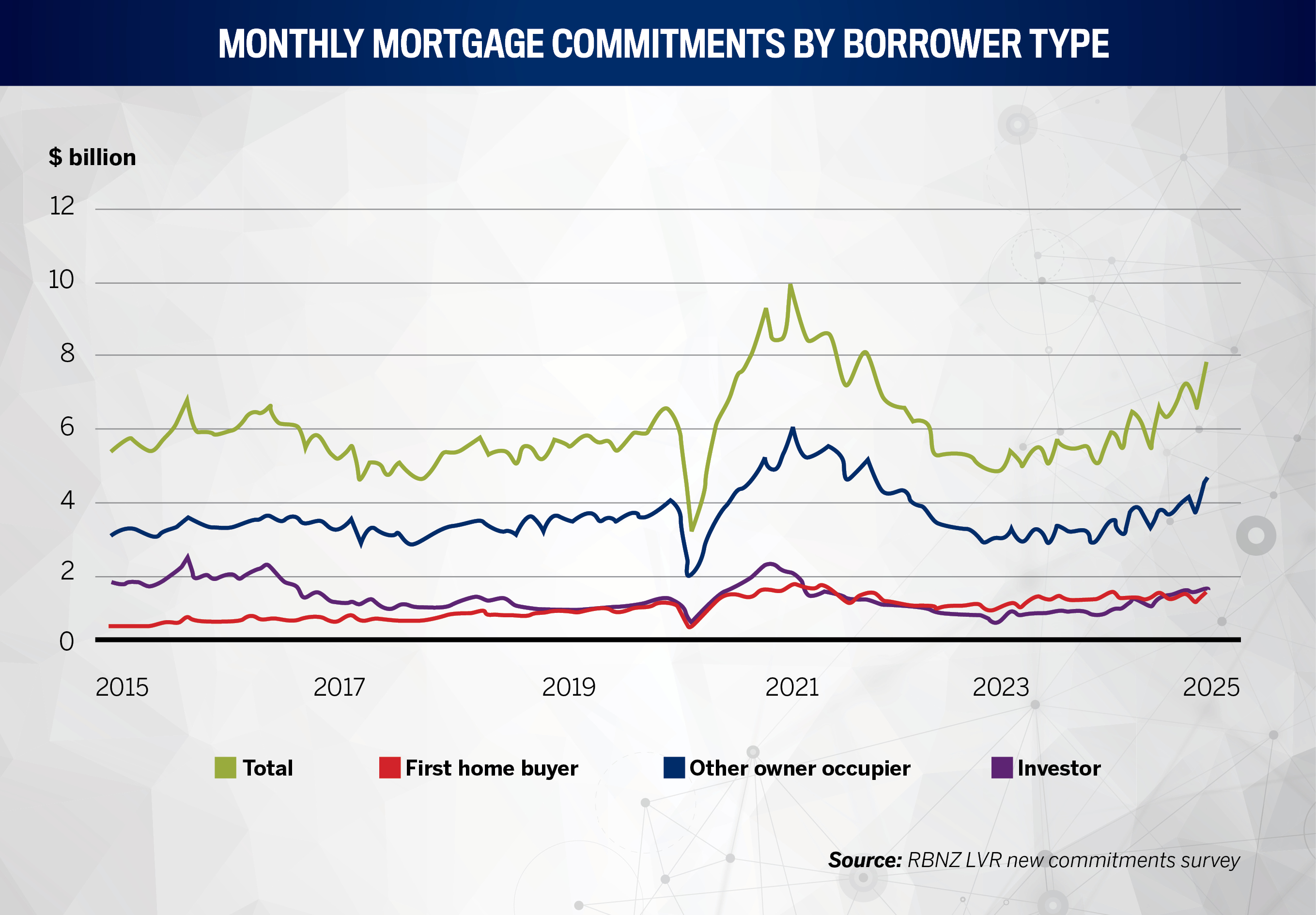

And it’s not just first home buyers. Owner-occupiers and other borrower segments are showing signs of renewed activity. Nearly halfway through 2025, new mortgage commitments are on the rise, a subtle sign that confidence is starting to return.

To determine this year’s Top Brokerages, NZA invited brokerages nationwide to submit performance data for the 2024 calendar year. To qualify, each brokerage needed at least one active loan writer based in a New Zealand-headquartered office. Aggregators were then asked to verify submissions.

The evaluation focused on four key metrics:

total loan book size

average settlements per loan writer

total settlements during the year

conversion rate

The firms that rose to the top delivered strength across all four. Among them were two standout brokerages maintaining high performance, keeping clients at the centre of everything they do.

In a market where rate sheets and turnaround times often dominate the conversation, the top-ranked brokerages are proving that long-term performance comes from sustained effort to understand the scope of each client’s financial goals.

For EverBright Finance managing director Frank Cui, whose firm ranked No. 7, the difference begins with knowledge of lending products and people.

“There are two things we’re proud of at our brokerage over the past 10 years, two things that set us apart. The first is knowledge,” Cui says. “At face value, a mortgage might seem like a simple financial transaction. But underneath, it’s often tied to deeply personal goals, sometimes even the wellbeing of a whole family. It might be someone’s first home, or it could be a business-critical decision. That context matters.”

The situation informs the leading brokerage’s entire approach. Cui and his team begin every client conversation by uncovering what’s driving the borrowing decision.

“If it’s a first home, then we think about the wider picture: budgeting, insurance and involving the right professionals. If it’s development or business lending, we look at tax impacts, liquidity and how one project might affect other parts of their financial life,” he explains. “It’s our job to structure things so that one move doesn’t put everything else at risk.”

Understanding the client’s situation is just one part of EverBright’s formula. The second, Cui says, is consistent, proactive and always personal communication.

“We update clients at every stage, even after funding has settled,” he adds. “That might sound simple, but it makes a huge difference. The biggest frustration we see is when clients feel left in the dark. They don’t know where their application stands or what the conditions mean for their life. Even when we don’t have answers yet, we check in. Just a short update gives people confidence. They know what’s happening, and we haven’t forgotten about them.”

At the No. 1 ranked Plaxo Mortgages, director York Zhang shares a similar philosophy shaped by nearly two decades of service, especially within New Zealand’s Asian community.

“Our strength comes from focus,” he explains. “We are a company that has spent nearly two decades doing one thing exceptionally well, which is providing mortgage advice.”

Plaxo’s long-term emphasis has given the team a deep, practical understanding of what clients need at every stage of their journey. “We’ve built up a large and strong client base, but more importantly, we understand our clients,” notes York. “We know their goals, their challenges and their unique needs. That experience helps us provide solutions tailored to each person.”

Like EverBright, Plaxo’s team thrives on seasoned financial expertise and constant learning. “Most of our advisers used to work at different banks, so they bring a lot of knowledge and insight,” he adds. “We have regular training to keep their knowledge sharp and up to date. That way, they can always offer clients the most current and competitive solutions.”

Whether the team is helping a first-time buyer or supporting a multigenerational family through property transitions, Plaxo focuses on understanding clients’ loan needs and the life behind them.

For New Zealand’s top mortgage brokerage firms, 2024 was about holding steady and supporting clients through longer timelines, tighter policy settings and a market defined by hesitation.

While others scaled back or froze hiring, mortgage industry leaders such as EverBright and Plaxo stayed active, adaptive and client focused, proving that resilience is as much about mindset as it is about process.

EverBright’s Cui points to what he calls a “liquidity slowdown” as one of the most pressing market challenges. He says, “The market isn’t moving like it used to; properties are taking much longer to sell. That affects everything.”

What was once a four-week turnaround now stretches into several months or longer. “You can’t reinvest, refinance or repurpose capital until the sale goes through, which used to be a three-month window and is now closer to a year,” he adds.

The brokerage’s strategy was to stay grounded and help clients manage the slowdown with informed, timely decision-making. “Our job is to work with the client’s goals, not push them into rushed decisions,” Cui says. “Sometimes that means extending pre-approvals or going back to lenders multiple times to rework the file.”

He adds that resilience starts with clear expectations and sound advice in a market full of uncertainty, including geopolitics, global trade disruptions and rate shifts. “No one ever gets the perfect deal. You must decide what matters most: speed, savings, or suitability. It’s about helping clients make informed trade-offs and stick to their purpose.”

That message applies to homeowners and developers. Cui says, “Sometimes, developers want to hold out for full profit, but the longer they wait, the tighter their cash flow gets. Maybe it’s better to take a smaller margin now to unlock the next opportunity rather than getting stuck in a liquidity trap that affects other projects.”

Over at Plaxo, York describes a different kind of complexity, one that comes not just from rising interest rates but from the noticeable slowdown in property transactions. He says, “Everyone is feeling the impact of high borrowing costs and a much cooler property market. Clients are becoming more selective and expect tailored solutions that fit their unique financial situation.”

This shift has significantly changed how brokers operate. A single loan file might now require more in-depth analysis, strategy adjustments, and multiple client discussions before the deal can be finalised.

“Today, it’s not uncommon for a home-buying journey to take many months,” York says. “During that time, the market changes, policies shift and client needs evolve. As a result, advisers are spending more time than ever ensuring every detail is right.”

Rather than buckle under the pressure, Plaxo focused inward, enhancing adviser training and client communication. York explains, “We upskill our brokers constantly and stay on top of policy changes. We also invite lenders for in-person updates and training sessions so our advisers are always informed of the latest rules.”

And in a rare move during a slow market, Plaxo kept growing its team. “We’ve brought in new advisers and placed strong emphasis on training, not just in product knowledge, but in how to connect with clients,” he adds. “We ensure our brokers have the time and support to offer personalised, high-quality service for every client.”

At the highest-performing brokerages, culture plays out in two distinct but equally powerful forms: one rooted in professionalism, the other in a strong sense of community.

For Cui, culture starts with clarity. “To me, culture is simply how you do things. That’s the heart of it. At our firm, our culture has always been built on professionalism,” he says.

It’s a word that can mean different things, but at EverBright, professionalism is about being prepared, precise, and quietly confident. Cui says, “We need to be seen as people who know what we’re talking about. If someone asks what a new economic policy or market shift means, we don’t guess. We explain it clearly and accurately. That’s the expectation we set for ourselves.”

And in a volatile market, professionalism also means resilience and choosing focus over fear. “In times of uncertainty, negativity can spread quickly,” adds Cui. “But our job is to find the opportunities, highlight the positives and stay focused on the long term. Buying a home or investing is about the future; it’s not like renting a car.”

For EverBright, culture also comes to life in how team members treat each other, especially when the numbers are down or the market is slow.

Cui says, “If someone feels like their performance has dropped compared to last year, we remind them that as long as you’re doing better than yesterday, you’re moving forward. That mindset helps us stay focused and motivated.”

Collaboration is another core value. With a portfolio that spans everything from residential lending to complex development funding, the top brokerage shares expertise internally.

“Not every adviser is the best fit for every type of transaction, and that’s okay,” explains Cui. “We often do joint visits with clients and share transactions between advisers. That ensures the client always gets the right solution, delivered by the person best suited to handle it.”

Beneath it all is an authentic connection built over time. Cui adds, “New team members often tell us they feel like they’ve joined a big family, not just a company. We encourage each other, mentor newer advisers and create an environment where people want to grow together. That bond is a big part of what defines us.”

At Plaxo, the word “family” is embedded in its culture. York says, “We believe in treating our clients the way we would treat our own family – genuinely looking out for their best interest, helping them find the loan structure that fits their needs, and guiding them with honesty and care.”

Its advisers and staff support one another with that same level of commitment. “Whether it’s mentoring new team members, sharing knowledge or working through challenges together, we believe that when our team grows together, our service gets stronger,” adds York.

It’s this culture that helps Plaxo build lasting client relationships. “Many of our clients come back to us again and again, not because of a rate, but because they feel understood and supported,” says York. “We often help families through multiple stages of life, from their first home to investment properties, and help their children into the market.”

That long-view approach to relationships has earned Plaxo its reputation for client loyalty. York says, “Our advisers recently completed a loan for the second generation of the same family. That level of trust comes from putting clients first, year after year.”

For Plaxo, becoming a long-term partner in people’s lives is the objective measure of success.

Top brokerages aren’t standing still in a market where change is constant and client expectations evolve just as quickly. They’re refining systems, investing in people and finding more innovative ways to deliver advice.

Industry expert Royle believes AI will play an increasingly important role in mortgage lending, but for simple, straightforward applications, he sees AI helping banks speed up “cookie-cutter” deals. However, he argues that complex cases, such as self-employed borrowers or clients with multiple investment properties, will still require human expertise for the foreseeable future.

For the best mortgage brokerage firms, staying ahead means planning with intention.

At EverBright, Cui starts every year by taking stock. “Every year, I reassess where my focus should be,” he says. “For 2025, I’ve narrowed it down to three key priorities. Any more than that, and I risk spreading myself too thin.”

His first priority is systems that work for clients and every person in the business. Cui says, “That means everything needs to run smoothly from the moment a client engages with an adviser to compliance, post-settlement check-ins, joint visits, training and professional development. If we’re using software, digital tools or automation, I need to ensure those systems are user-friendly, effective and meet compliance standards. That’s foundational.”

The second area of focus is product innovation, specifically, finding ways to offer more than just what’s available off the shelf.

“We’ve been working on a finance release product for the past two years that will allow us to offer something unique to the market,” explains Cui. “The idea is to create solutions that meet unmet customer needs and give our advisers more value to bring to their clients, going beyond the standard supplier options most brokers work with.”

Whether that means new funding lines or entirely new lending structures, the goal is the same, which is to expand what’s possible for advisers and clients. Cui says, “It’s about giving our team more confidence and choice in client conversations.”

People are Cui’s third and final focus. “You can have a room full of talented people, but that talent fades if there’s no clear leadership and no ongoing support or training,” he says. “If you’re a financial adviser, you need to know your craft inside and out. There’s no room for uncertainty in this role.”

At Plaxo, York is focused on a complementary track – tech with a human lens. “We’re paying close attention to how technology, especially AI, can support our work,” he explains. “We’re hopeful that the industry will see more AI-powered tools designed specifically to help advisers improve their efficiency and deliver even better client outcomes.”

York quickly points out that doesn’t mean sacrificing trust. Client privacy remains non-negotiable. “As we adopt more advanced tools, we remain conscious of client privacy. Protecting sensitive information is non-negotiable, and we’re careful about how we implement technology in ways that maintain that trust,” he says.

That cautious approach is already beginning to shape how the Plaxo team trains and supports its advisers. York says, “We believe technology can help us build a more complete and effective training system. At Plaxo, we’re working to integrate these tools into our onboarding and internal learning processes so that advisers can develop faster and more consistently.”

The industry is also beginning to explore how tech might enhance the client’s experience, particularly regarding financial literacy and application preparation. “For us, it is a tool, not a replacement,” says York. “It should help us strengthen our service, not take away the personal touch. That balance is what we’re aiming for.”

What separates a top-performing brokerage is discipline, clarity and a keen understanding of what matters most in a changing market.

iLender’s Royle emphasises that in today’s digital work, trust is the foundation of mortgage advising, even more than technical expertise. “Trust, to me, is the most important thing in dealing with people,” he reflects. “It’s interesting that as the percentage of broker-derived business goes up, the number of complaints goes down. I think the adviser network in New Zealand is extremely bright and very rosy indeed.”

EverBright and Plaxo’s leaders say their lessons can help any firm looking to build something that lasts.

Cui quickly distils it to one core principle: trust the process. He says, “If I had to pick one lesson that stands out, it’s trust the framework. I mean the structure and system behind engaging clients, sourcing opportunities, managing files and delivering results from start to finish.”

It’s not a new concept. He points out that these frameworks have been refined over decades, tested by experience, and proven by performance. “When you apply them consistently, day in, day out, you’ll do well. It’s about rhythm, not randomness,” adds Cui.

That, he says, is what carries brokers through even the toughest cycles. “Sometimes, especially for newer brokers, it can feel discouraging. Maybe the market’s slow, or life throws in some personal challenges. But I’ve seen people succeed through all of that. The ones who stick with the process, who show up consistently, keep performing. They don’t just survive; they actually enjoy the work.”

And over time, the structure becomes ingrained. Cui explains, “The system becomes your own, but the fundamentals stay the same. It’s not about working frantically one day and then doing nothing the next. You need steady action and consistent effort. That’s what builds results.”

It’s also about patience and endurance. “This business isn’t a sprint; it’s a marathon,” says Cui, who began his career in banking in 2003. “You might not start with perfect instincts, but if you repeat the right actions, they’ll become second nature.”

On the other hand, York offers a lesson of a different kind, one anchored in client service during volatile times. He says, “One of the biggest lessons we focused on last year was the importance of customer service.”

In a high-interest, low-transaction environment, good service includes responsiveness, clarity, care and putting clients’ wellbeing first. “Every client’s situation is different. Our role is to help them find a loan structure that’s right for them, based on what’s financially safe, sustainable and aligned with their long-term goals,” explains York.

As lender policies shifted and rate offers became more complex, Plaxo stayed focused on high standards of service. York says, “We spent more time understanding the client’s full picture, which includes their income, risks and future plans and presented the best available options clearly and professionally. That’s real customer service.”

At times, delays or confusion can occur, but York says that’s exactly where professionalism matters most. “When things take longer than expected, it’s often due to poor communication or lack of preparation. So, we’ve been training our advisers to be more proactive, transparent and focused on solving problems before they escalate.”

To establish this year’s line-up of the most prominent industry players, NZ Adviser invited brokerages in New Zealand to submit their accomplishments for the 2024 calendar year.

To be eligible, brokerages needed to have three or more loan writers in a single office headquartered in New Zealand. Aggregator information was also provided by applicants, and their aggregators were then required to verify the details submitted.

The application also asked for details such as the number of active brokers working at each company as well as the total loan book value and conversion rate. The nominees were evaluated across four areas: total loan book size, average settlements per loan writer, total settlements in the specified 12-month period, and conversion rate.