Jump to winners | Jump to methodology

In a market flooded with tools and information, more borrowers still choose mortgage advisers and stay loyal. It’s not about convenience; it’s about service. NZ Adviser’s Top 25 Brokers 2025 have found the balance clients want, combining expertise and a client-first approach to match needs with the right loan.

The renewed borrower focus shows in the numbers. According to the Reserve Bank of New Zealand, total new mortgage commitments hit $7.6 billion in April 2025, up 28% year over year. Despite a modest dip from March, the longer-term recovery points to a rebound, with more buyers turning to expert advice.

That advice carries weight, particularly in a lending environment where even minor oversights, whether in structure, timing or lender policy, can lead to delays, added costs or long-term financial strain.

And the stakes are rising. The average loan size climbed to nearly $393,000 in April 2025, up 4.3% from a year earlier. That kind of commitment leaves little margin for error for buyers working to meet deposit thresholds or manage repayments.

Unsurprisingly, first home buyers, who are facing the most complexity with the least experience, are increasingly turning to expert help. FAMNZ’s 2024 Consumer Access to Mortgages report found that nearly 60% of first home buyers went through a mortgage adviser in the 12 months to July 2024, up from 42% across all first home buyers. This shift signals a growing preference for hands-on advice over self-directed banking, particularly among younger borrowers entering the market for the first time.

Reserve Bank data backs this trend, showing the total value of lending to first home buyers rose by 22.4% in April 2025 compared to the year prior, pointing to a clear rebound in buyer activity despite tighter market conditions.

FAMNZ also found that among borrowers who took out a mortgage in the 12 months to July 2024, 46% went through an adviser, up from 35% across all borrower groups, including those with earlier loans.

And that growth is expected to continue. Nearly 1 in 2 future first-time buyers (49%) say they plan to use a mortgage adviser for their next loan, well ahead of those opting for direct lender channels. Women, in particular, show even stronger preference, with 56% favouring the adviser route.

NZA’s two-year data confirms that the trend lines point to growing market share and that borrowers are no longer focused solely on rates or speed.

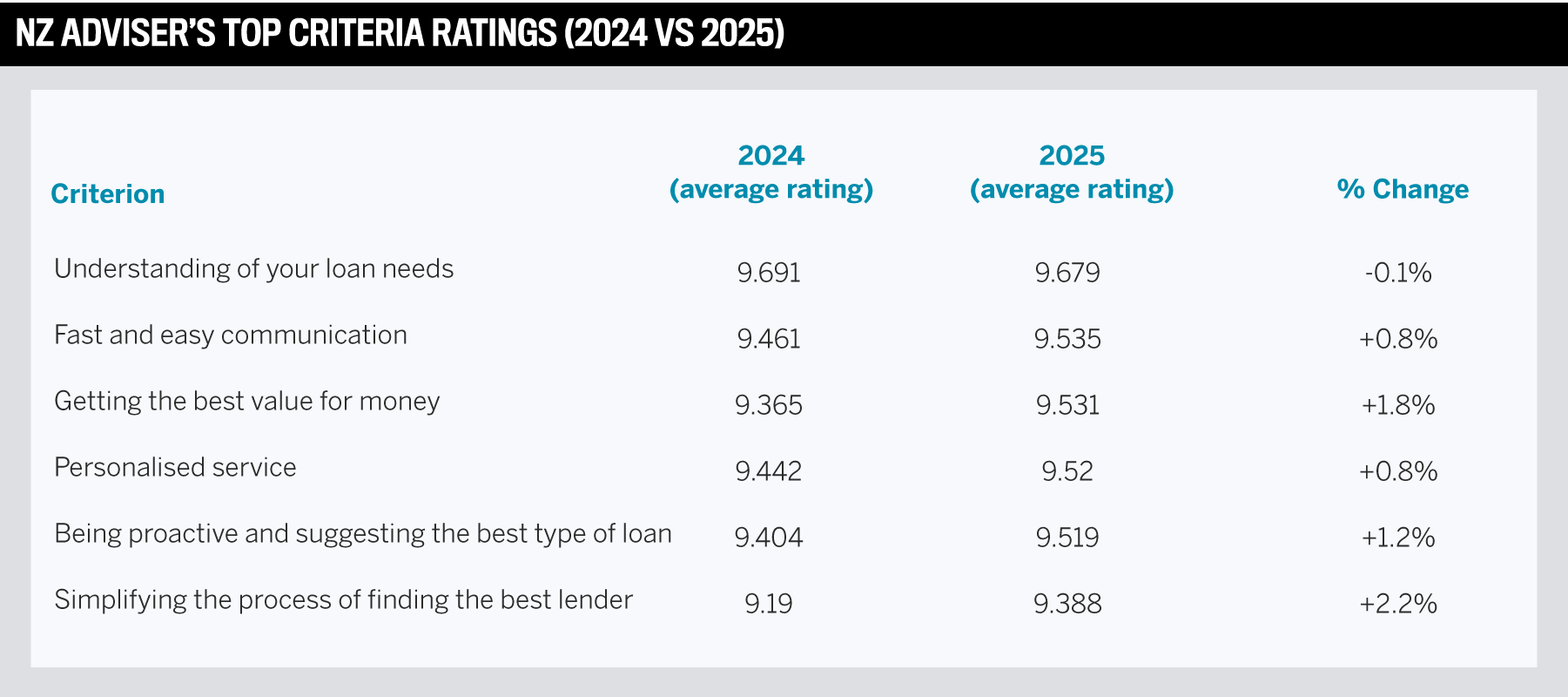

When asked to rate what matters most in their adviser relationship, respondents ranked understanding their loan needs far above all other criteria. They also gave high marks to communication, service and tailored guidance, which speaks to trust.

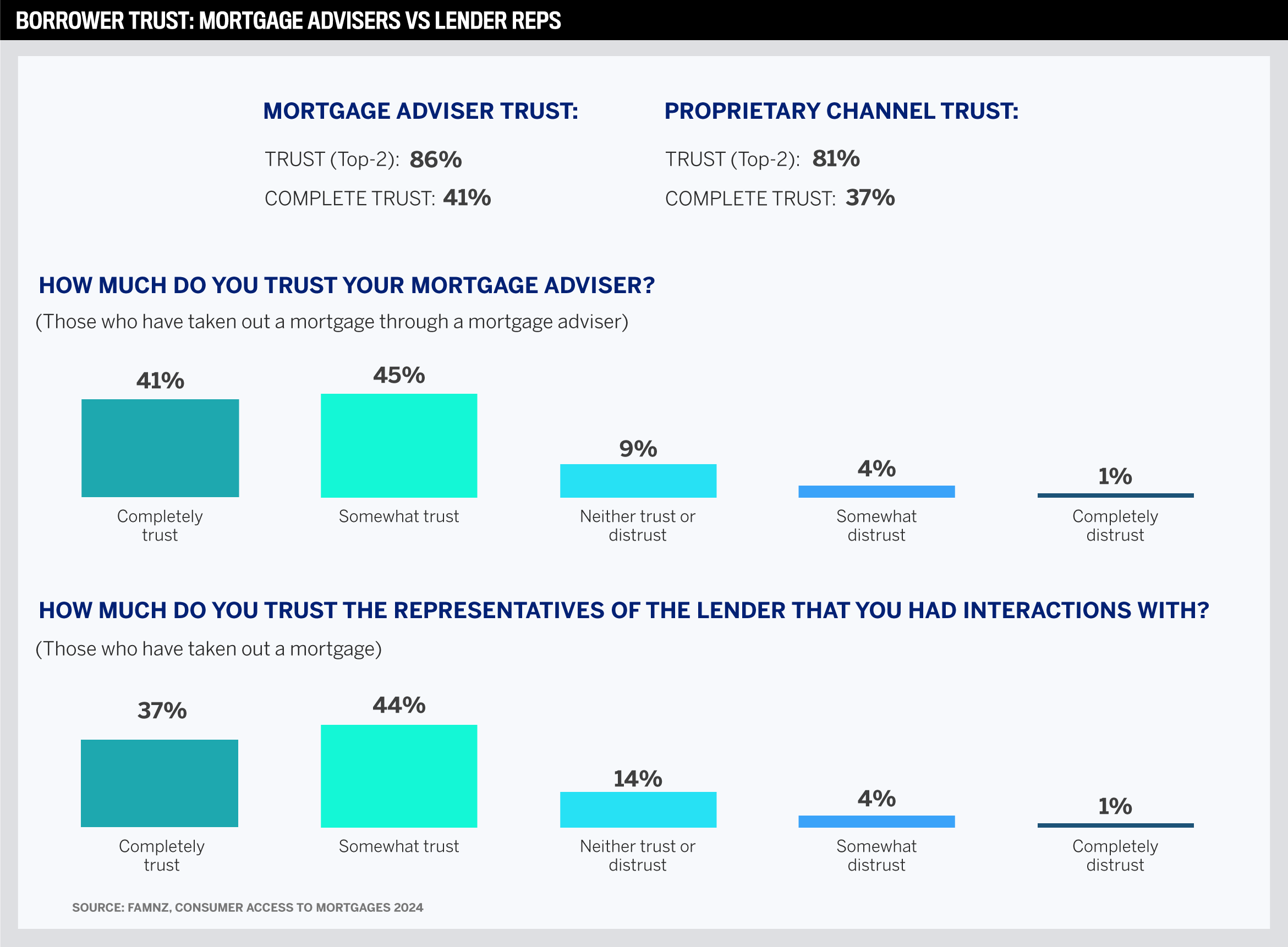

According to FAMNZ, 86% of adviser clients trust their adviser, including 41% who said they “completely trust” them. That’s a stronger result than lender reps received and reflects the importance clients place on being heard.

It follows that more borrowers are turning to advisers. Clients want someone who understands their goals and can turn financial decisions into meaningful outcomes.

Link Financial Group’s national growth manager, Luke Roberts, puts it plainly, “Leading advisers are distinguishing themselves through consistency, proactive client engagement and a commitment to delivering holistic financial advice. Rather than focusing solely on mortgages, they’re positioning themselves as full-service financial advisers, building strong referral networks and trusted, scalable brands.”

This year’s best mortgage advisers are thriving in a market where clients expect:

competence, insight, and responsiveness

an adviser personally invested in the outcome

The Top 25 Advisers of 2025 have embraced these expectations. They actively participate in the process, guiding and advocating for their clients. NZA’s data shows that clients recognise and value that difference.

With mortgage products becoming harder to distinguish, the adviser’s skill in tailoring advice, explaining options and building trust makes a real impact. That approach defines this year’s winners and continues to resonate with clients.

“The standout factor is clear, consistent and timely communication,” Roberts adds. “Top advisers set realistic expectations from the outset. If a process is expected to take seven business days, they communicate upfront and keep clients informed throughout. This level of transparency, combined with expert guidance, builds trust and ensures clients feel supported every step of the way.”

The data confirms what the Top 25 advisers are getting right. Clients care most about being understood. They want advisers who listen first and recommend later. Service delivery also plays a central role, with fast, clear communication and personalised support high on the list. Value has become an expectation and has seen the most significant rise. And while lender comparisons still matter, they’re not what wins trust. Clients seek insight they can act on, advice that fits their needs, and advisers who can connect the dots.

Broker rating: 10.00

Top scoring for all categories

A two-time Top 25 winner, Jack Hou has built a reputation for integrity, insight and advice that makes a difference. Drawing on nearly two decades of experience at New Zealand’s major banks, he brings technical expertise and empathy to his work, especially for clients with complex financial situations.

“Trust starts with listening and understanding without judgement; that’s my number one,” he says. “Many of my clients are migrants, just as I was when I came to New Zealand as an international student. They’re navigating complex life, business, career and education changes. The systems are unfamiliar.”

His approach draws strength from patience, explaining things in plain language and staying accessible beyond standard business hours. That commitment showed in a recent case involving a client juggling multiple income streams, including a property management business, vehicle advisory services, and rental, Airbnb and PAYE incomes.

They’d just lost their dedicated banker and needed to swap securities, restructure lending, refinance and get preapproval for another property within one month. The banks said no, but Hou got to work. He analysed the structure, prioritised needs and liaised directly with credit teams. His efforts paid off. Thanks to his persistence, the client secured finance and avoided disruption to their portfolio.

“I’m not just a mortgage adviser,” he says. “My role is to build tailored solutions, stay hands-on and be strategic and innovative to bring a holistic outcome.”

Clients echo this mindset. One described him as “the best adviser I have ever met with high ethics and professionalism.” Another appreciated his direct, personalised style: “He explained things clearly and simply.” That blend of clear communication and professionalism helped drive his perfect scores.

Hou’s work also extends beyond single transactions. He regularly collaborates with solicitors, accountants and developers, coordinating strategies that turn complex borrowing needs into achievable outcomes, and serves clients not only across New Zealand but also in Singapore, China and the US.

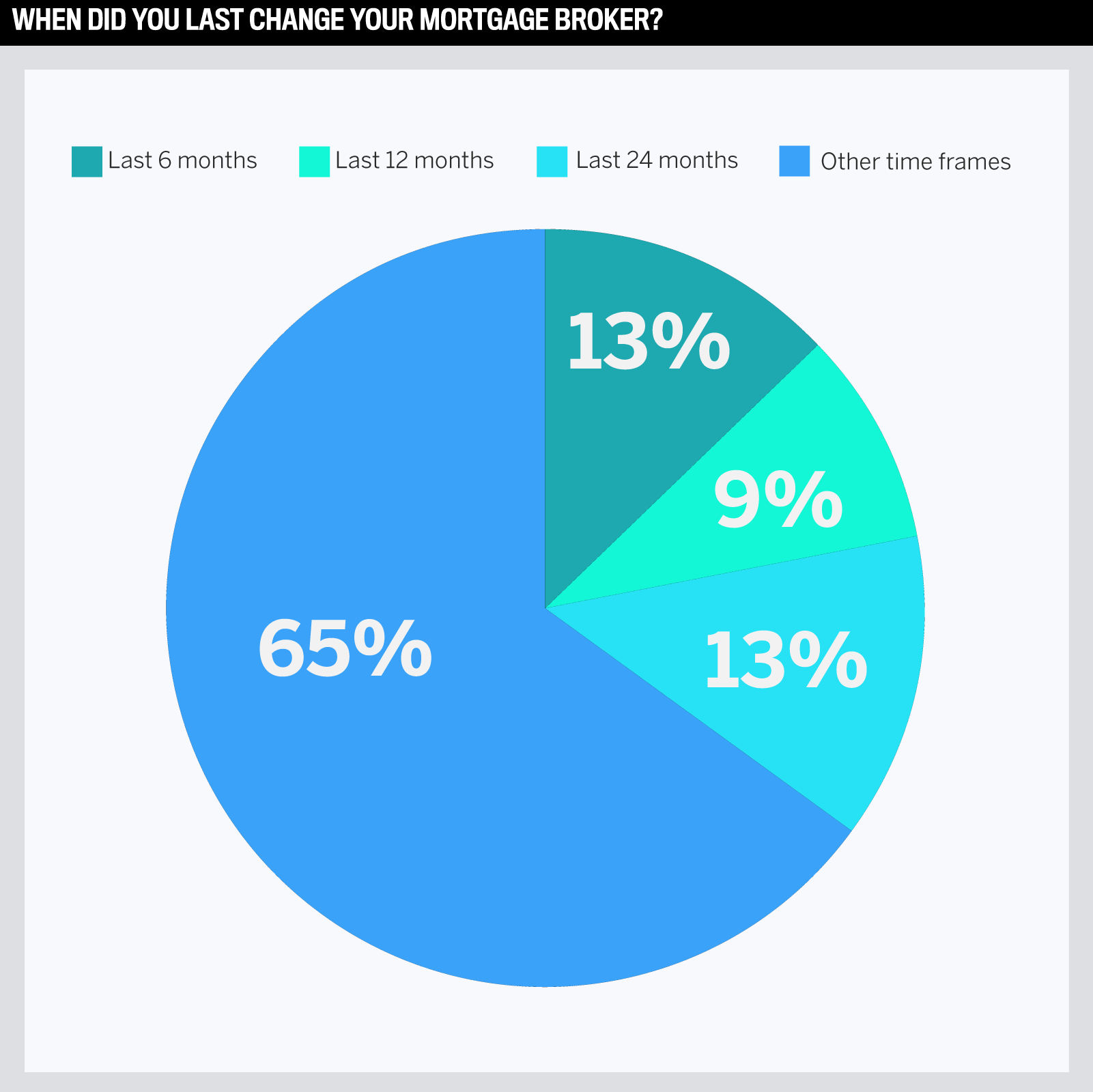

New Zealand’s mortgage market is loyalty-driven. Nearly two-thirds of clients haven’t changed advisers in more than two years or ever. That kind of retention is uncommon in financial services and speaks to the strength of the relationships many advisers are building.

Short-term switching remains low. Just over 21% of clients moved in the past year. Even over two years, fewer than 35% have made a change. When clients do switch, it’s often due to major life events, not dissatisfaction with service.

Trust is durable for the best mortgage advisers but needs maintenance. Advisers who stay visible through check-ins, refinancing reviews or just ongoing advice are the ones who keep that loyalty intact.

As industry expert Roberts sees it, the best mortgage advisers are setting new standards. “Across multiple sectors, clients are seeking more personalised, end-to-end financial advice,” he remarks. “Advisers are well positioned to meet this demand, not just by keeping up, but by leading the way. Their evolving role brings greater responsibility and significant opportunity to deliver long-term value.”

He notes a key differentiator for advisers is operating under a Financial Advice Provider licence as an authorised body, which Link Financial Group offers. Roberts adds that this structure enhances compliance and client confidence while delivering significant time and cost efficiencies, allowing advisers to spend more time building relationships and growing their businesses.

Broker rating: 9.86

Top scoring for understanding clients’ loan needs and a tie for personalised service and simplifying the process

Jacob Teleiai believes advice should be a conversation, not a pitch. The mortgage adviser listens first, simplifies the process and builds trust by helping clients feel heard and informed. That focus on service over sales helped place him among the best client-first advisers of 2025.

“Every qualified mortgage adviser should be able to do the job, but it’s about letting the client build trust through the conversation,” he says. “If they walk away thinking, ‘I got some value out of that,’ and they understand what’s going on, that’s what matters. I like to educate people so they understand what they’re signing up for and how I’m helping them get there.”

Most of his clients are first home buyers or people buying their first investment property, and Teleiai supports them at their own pace until they’re ready. “One client came to me in 2022 and just bought their property this year (2025),” he says. “It can be a long journey, but they got in touch again and said they appreciated the advice and were ready to move forward. They could’ve gone to someone else, but came to me because of that original conversation.”

That approach is echoed in client feedback. “Jacob is the first person we ring whenever we want to pursue a major financial milestone,” said one client. Another highlighted his ability to meet them where they are: “He made sure to understand our life priorities, without judgement, and gave advice that suited our stage of life.”

Teleiai also shared a case where a client had already gone unconditional on a plan to build three homes, but no bank would back it. One non-bank lender was interested, but the fees were steep, about $80k, and the rate was 11.45%. Then, they pulled out after seeing the valuation.

“I stepped in, helped restructure the deal to two homes with civil works for the third and got it approved through his existing bank at under 6% interest, with no fees, saving him over $200k. It took about four months, but it was worth it,” he reflects.

He brings a hospitality mindset to mortgage advice, a way of working he’s carried with him since his early days in restaurants. A former employer once told him, “Treat every person who walks through that door like they’re walking into your home.” That idea stuck. It shaped how he treats clients with warmth, attentiveness, and a strong sense of service.

“That’s just me in a nutshell,” he says.

Teleiai sees his role as cutting through the noise. Clients often come to him after hearing advice from all directions: family members, friends, and people reminiscing about property deals from decades ago. His goal is to help them sort facts from opinions. “If someone can walk away from our conversation and explain their position with confidence, not second-guessing themselves, that’s success,” he says.

Even if they don’t end up using his services, what matters to Teleiai is that they leave with a stronger understanding of where they stand and what’s possible.

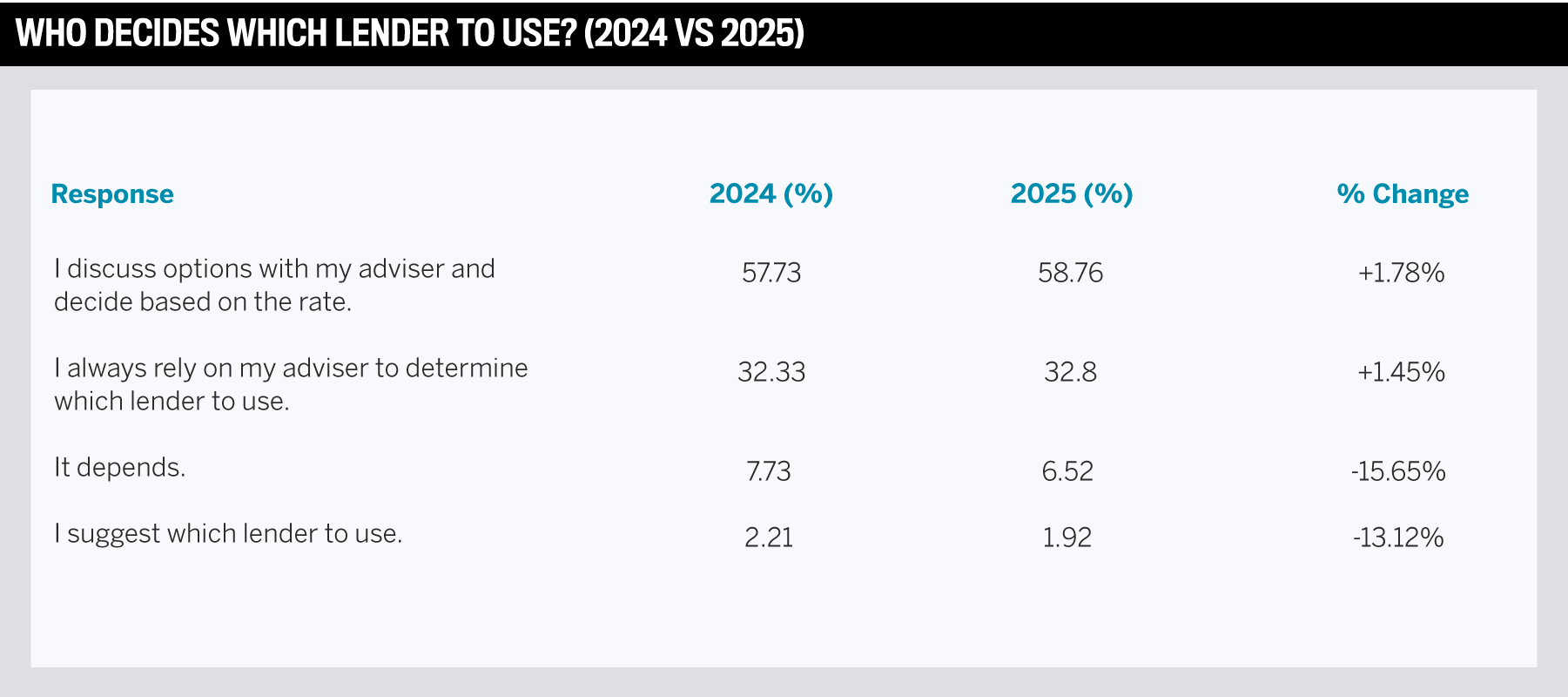

The adviser-client relationship is built on collaboration, but for most, that collaboration leans heavily on expert guidance. In 2025, nearly 60% of borrowers said they discussed lender options with their adviser but let the final choice hinge on the rate. A further 33% deferred entirely to their broker. Taken together, more than 9 in 10 clients don’t want to make this decision on their own.

What’s changed since 2024 is subtle but telling. Fewer respondents say, “It depends,” and fewer suggest the lender themselves. That shift suggests that clients are growing more confident in the process and more decisive in engaging with their advisers. They’re either leading the conversation with support or handing it over entirely.

For advisers, this reinforces the importance of transparency and structure. Clients want to feel involved but not overwhelmed. The best mortgage advisers can walk clients through the options, explain the trade-offs and simplify the decision without removing agency. That’s what good communication and skilled advising look like in 2025.

This year’s top advisers are winning trust by giving clients a voice. They’re guiding decisions in a way that makes clients feel informed and supported without asking them to manage the details alone. Top advisers can focus on better outcomes with the right support systems in place, whether personal or tech-enabled.

Roberts says, “We’re excited about AI’s potential to boost adviser productivity and improve client outcomes. It allows advisers to focus on what matters most: delivering high-quality service.”

Broker rating: 9.97

Top scoring for personalised service; being proactive; fast and easy communication and simplifying the process

For Saneel Kumar, it’s not enough to land the deal. What matters most to him is leaving clients better off long after settlement. That mindset shaped his approach to trust, transparency and long-term guidance, earning him a spot among this year’s Top 25 advisers.

At the heart of his success is a philosophy that combines:

simplifying the process

consistency and ongoing support

reliability and responsiveness

“We try to make every interaction meaningful by removing jargon and complexity,” he says. “That means using plain language, staying consistent and showing up, whether it’s through after-hours texts or weekend video calls. It’s about being confident in every situation, keeping clients informed and treating everyone equally.”

Kumar recently helped a client who’d been burned by past experiences and had nearly given up on property ownership. Instead of diving into an application, he took a coaching-first approach.

He reviewed their finances, mapped a clear path forward and set up fortnightly check-ins to track progress, from budgeting to credit conduct. When the time came, the client was ready, and the financing was approved.

What sets Kumar apart is his focus on building trust by following through on every promise, no matter how many clients he’s working with. He offers expert advice on products, but it’s his focus on helping people understand their options and make informed decisions that builds lasting relationships.

He stays on top of industry trends, including Reserve Bank updates, and breaks those down for clients to see how they apply to their situation. He’s also made the process easy to access, offering free discovery sessions through Outlook or the company website, with plenty of flexible time slots, including evenings and weekends.

Clients appreciate Kumar’s skill and integrity. One respondent noted, “Saneel is very honest and ethical in his practice.” Others praised his follow-through: “He does what he says he’ll do. He’s reliable, knowledgeable, and makes things simple.”

Whether helping first home buyers or seasoned investors, he delivers credible, value-backed advice. Many clients come to him after negative experiences elsewhere and stay because they trust his transparency and commitment.

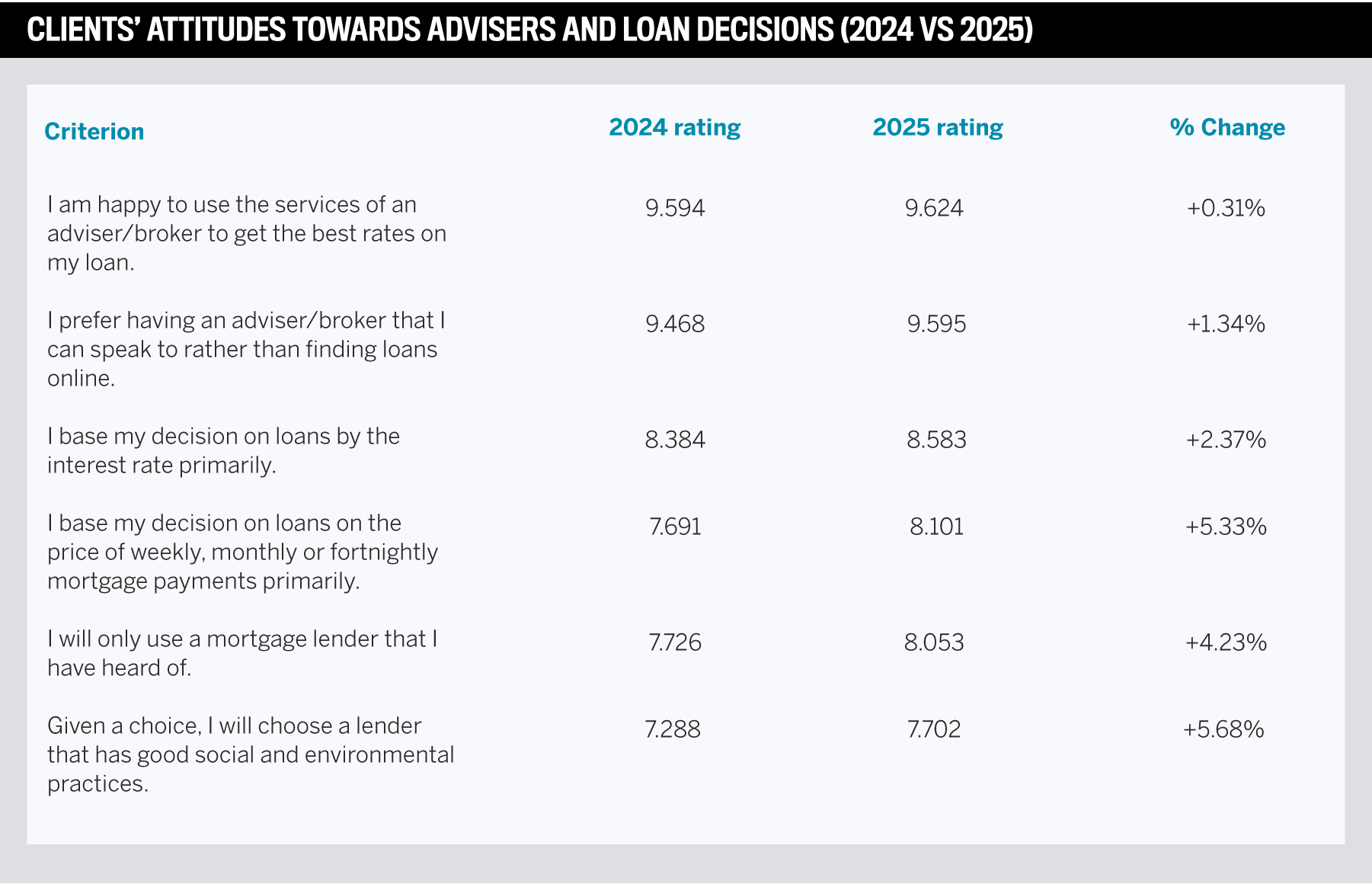

NZA’s data confirms that client reliance on mortgage advisers is strong and deepening. The top two statements related to adviser preference continue to hold the highest ratings and have even edged up slightly from 2024. This reflects a deliberate preference for personalised, expert guidance over self-directed digital tools.

Clients are also getting more discerning in how they weigh affordability. Ratings rose for both interest rate and payment amount as primary decision factors. That shows a borrower who is informed, cost-aware and actively comparing outcomes but still turns to advisers to make sense of the details.

Meanwhile, brand recognition and ESG values remain further down the list, even as their scores improve. Clients care about these elements, but they don’t drive the decision. Social alignment and name familiarity are secondary to rate strategy and adviser trust in a cost-sensitive environment.

Clients still want human expertise, but now it comes with higher expectations. They’re looking for advisers who combine relationship-building with technical expertise. That means being able to speak plainly about loan structure, repayment outcomes, and lender selection. The advisers recognised in 2025 by NZA are meeting that standard. They’re making recommendations and translating complexity into confident decisions. And clients are noticing.

Roberts believes there’s strong potential for growth in New Zealand’s mortgage market. “In Australia, third-party mortgage lending has reached 77%, and New Zealand has a real opportunity to follow suit,” he reflects. “We’re actively advocating for channel parity and maintaining an ongoing dialogue with the banks to support our advisers. By positioning themselves as full-service financial advisers, they can build lasting client relationships and meaningfully expand their market share.”

Broker rating: 9.70

Top scoring for: fast and easy communication and simplifying the process

When clients describe Debbie Reed, one word keeps coming up: present. Not just in terms of availability, though she’s known for picking up the phone after hours, but also emotionally present.

Reed builds trust by leading with empathy, listening intently and supporting clients through moments far beyond the loan itself. “For me, it’s about engaging with the individual and being there to hear and understand what the client is looking for, what they want and answering their questions,” she explains. “I’m naturally relational, so I genuinely want to engage with my clients. I care about them. I want to help them get to where they want to go. I don’t give up easily, and they know I’ve got their back.”

One of her very early clients was a mother who faced some incredibly tough circumstances but was determined to buy a home for her children. After being turned away by multiple banks, Reed found one willing to say yes.

“She told me, ‘Now I know they’ll have a place to call home,’” she recalls. Another client later said, “I’m the first person in my family to buy a house, and you helped us do that.”

Personal relationships underscore Reed’s overall approach to mortgage advising. She’s straightforward but never clinical. “People want someone who’ll say, ‘Let’s work through this,’” she explains. That care and emotional intelligence resonate through her work. One client said, “She was there for me like I’d just spoken to her last week, even after years of absence.”

Another says, “Debbie always has time to answer questions, no matter how silly they may seem. She explains everything thoroughly and ensures you understand how things work.”

Whether a client is going through a separation, grief or first home nerves, Reed becomes a constant, someone invested in the outcome. Clients call her “worth her weight in gold” and say she’s “literally changing lives”.

That trust, forged under often stressful circumstances, keeps clients returning years later, even across multiple property sales and regions.

Reed doesn’t claim to do anything others can’t. But what sets her apart is her investment in her clients. Helping people reach their financial goals is something she approaches with unwavering commitment.

That drive is evident in her emphasis on empowering clients to feel confident and informed. The goal is to keep them in control by understanding their current position, what comes next, and which options are on the table.

Technical skill is the baseline: Top advisers go further by building trust and simplifying complex financial decisions.

Service is the differentiator: Consistent, relationship-led guidance stands out in a volatile lending environment.

Client expectations are rising: Communication, engagement and full-service advice are now table stakes.

Loyalty must be earned: Advisers are proving that long-term relationships stem from honest conversations and real value.

Growth potential is strong: With adviser-led lending still trailing Australia’s 77% third-party share, there’s room for market expansion.

NZ Adviser’s second annual Top 25 Brokers initiative celebrates the mortgage professionals across New Zealand who go above and beyond in serving their clients’ best interests.

Drawing from a wide and diverse pool of advisers, the campaign highlighted standout individuals who demonstrated exceptional passion, dedication and client-first commitment.

Between 10 March and 4 April, the NZA team rolled out an extensive marketing and survey campaign, engaging thousands of readers nationwide. Participants were invited to nominate their brokers and rate them across six key criteria.

Brokers who received the most nominations and earned an average score of 9.0 or higher were named as New Zealand’s Top 25 Brokers, an honour based not on revenue, but on outstanding client service.