With rate cuts boosting borrower confidence and competitive rates for the taking, refinancing demand is heating up

Refinancing is having a moment.

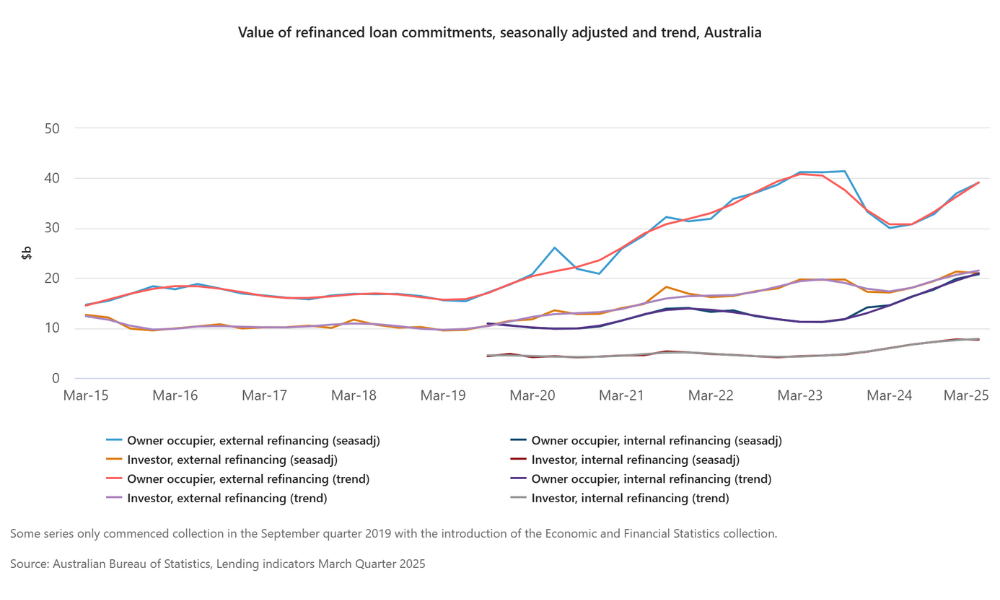

Data shared with MPA by Commonwealth Bank shows that refinancers accounted for 44% of mortgage market share in April 2025, with the banking major anticipating sustained growth throughout the rest of 2025.

ANZ, meanwhile, highlights that refinancing volumes have surged by up to 40%, with a 20-30% increase in the number of transactions, per Australian Bureau of Statistics data.

No prizes for guessing why: with Reserve Bank of Australia rate cuts in the bag and more (probably) to come, customers are making a move.

“We’ve certainly seen a shift in momentum,” Natalie Smith (pictured, centre), ANZ’s general manager, retail broker, told MPA. Brokers are reporting that customers are becoming more active in reviewing their home loans, “particularly as interest rates begin to ease”.

The significant uptick in refinancing market share “reflects a growing confidence among homeowners and investors to take advantage of the lower interest rates," said Baber Zaka (pictured, right), CommBank’s general manager, third party banking.

“This trend suggests that the refinancing market is continuing to pick up pace, with more individuals seeking to benefit from the current rate conditions,” Zaka told MPA.

Meanwhile, at ING Australia, “we've seen a noticeable increase in refinancing activity, and we expect this trend to continue throughout the year," said the non-major’s national sales manager, Sergio Delvescovo (pictured, left).

Factors such as potential rate reductions, a rise in market confidence (particularly among investors), increasing cost of living pressures and the expiration of customers’ fixed loans “will likely contribute to ongoing refinancing demand”, Delvescovo said.

Read more: RBA rate cut could save homeowners over $1,200 a year

While banks have their own thoughts about what the RBA is planning next, they all agree on one thing – more cuts are likely on the way. And that means the refinancing market can only get hotter.

But while this presents opportunities for brokers and banks alike, market saturation on both sides of the transaction makes for a hotly competitive refinancing environment.

Adapting to change

“In an environment where there is a lot of focus on cost of living pressures, it is crucial to view an entire product offering when customers are considering shopping elsewhere,” said Zaka. “While interest rates are undeniably important, it's essential to consider all facets of a home loan product.”

Zaka said that “CommBank is always looking to adapt our policies to support our brokers and their customers with ways to increase borrowing capacity” – a key factor in customer decision-making.

To give an example, CommBank recently made headlines after changing the way it factors HELP Debt into home loan applications. Customers who repay their HELP Debts within 12 months have the debt excluded from the servicing calculation, reducing the lending buffers applied to longer debt horizons.

“Customers looking to refinance to CommBank can take advantage of our flexible home lending policies, competitive pricing and access to the CommBank app where they can change the date and frequency of their payments to suit their financial situation,” Zaka said.

Customer retention “is about continually providing a second-to-none customer experience”, Delvescovo said. “At ING we continuously evolve our home loan products to meet the changing needs of our customers. We focus on offering competitive rates, flexible banking solutions and innovative digital experiences to enhance convenience and value.”

He also stressed the importance of listening to broker and customer feedback, saying ING refines its offerings accordingly, “ensuring they align with market trends and individual financial goals”.

At ANZ, Smith said, “We know that customers have more choice than ever, so it’s critical that we continue to evolve our offering to meet their expectations – including when they come to us through a broker.”

Addressing the loyalty tax

While lenders need to entice customers with competitive products, existing customers have expressed frustration with the "lender loyalty tax", whereby they miss out on rates offered to new borrowers.

When questioned on the matter, Smith said transparency is essential. “It’s important to us that our existing customers can have confidence that they’re receiving a good deal,” she said. “This is why we share the latest home loan rate changes on our website, as well as making customers’ interest rates easy to find via ANZ Internet Banking and the ANZ app.

“We also proactively contact broker-introduced customers who are about to roll off fixed rates at various points of their journey.

“Our aim is to ensure customers feel supported, know what to expect in terms of the process and understand their options when their fixed rate expires. Where the customer wishes to update their loan or apply for further lending, we’ll refer them to their broker in the first instance.”

Zaka highlighted the actions CommBank has taken in the latest monetary easing cycle. “This year, the Reserve Bank of Australia has reduced the official cash rate twice, and CommBank has passed the full cut on to all customers with a variable rate home loan," he said.

“Following each rate reduction, we proactively contact all impacted customers, advising them of their new interest rate and informing them that they may be eligible to reduce their direct debit repayments.”

"CommBank is always looking to adapt our policies to support our brokers and their customers with ways to increase borrowing capacity" - Baber Zaka, CommBank

At ING, Delvescovo said, “We encourage brokers to conduct regular health checks with their clients to ensure their loan remains suitable. We also provide competitive variable rates; clear, straightforward and simple home loan products so customers can easily access alternatives within ING.”

Seizing the opportunity

All in all, it looks like refinancing is set to go gangbusters in the second half of 2025. But how can brokers best equip themselves to make the most of it?

“Brokers should prioritise understanding their customers' unique situations to offer tailored refinancing advice effectively,” said Zaka. “Utilising CommBank's available material can be invaluable in this regard, as it helps clients understand refinance options and the associated benefits.”

Zaka recommended sharing this material directly or using it as a discussion tool to facilitate better conversations, “enabling clients to make well-informed decisions about their refinancing possibilities”.

“At CommBank, we offer exceptional self-service and support, alongside our award-winning app, to manage finances effectively," he said. "By providing brokers access to customer loan information in Your Loans, we improve the experience.”

Delvescovo advised brokers to be proactive. “Regularly check in with your customers to ensure their home loan continues to meet their needs,” he said. “As circumstances change over time, brokers are well positioned to help customers reassess their financial situation and identify better loan products or structures, ensuring they secure the best possible deal.”

“We know that customers have more choice than ever, so it’s critical that we continue to evolve our offering to meet their expectations” - Natalie Smith, ANZ

Smith drew attention to ANZ’s residential broker learning and development program, Brokerology. “Not only does this cover our home loan products, policies and processes, but it also provides brokers with access to resources and insights that can help them elevate their business and stand out in the market," she said.

“We also recently launched our new ANZ Home Loan Calculator via the ANZ Broker Portal, so brokers can quickly estimate their customers’ home loan fees, repayments and serviceability.”

As for customer trends, Zaka said that “both owner-occupier and investor customer segments are taking advantage of the favourable conditions.” However, he is seeing more activity on the owner-occupier side, “driven largely by the desire to reduce monthly repayments and alleviate cost of living pressures.”

The story is the same at ANZ, where owner-occupiers “might be more likely than investors to review their loan structures and reduce their debt as quickly as possible," said Smith.

“That said, both segments remain active,” she said. “At ANZ, we’ll continue supporting our brokers to ensure they’re well placed to provide all borrowers with tailored advice – whether that’s helping owner-occupiers review their home loan or guiding investors through more complex lending structures.”

ING, meanwhile, has seen significant growth among investor customers, with activity rising six times the market average. “This surge is likely driven by recent policy enhancements to help facilitate market entry, along with renewed investor confidence amid lower interest rates,” said Delvescovo.

“We've seen increased activity from SME customers following recent policy changes designed to make it easy for them to borrow with ING” - Sergio Delvescovo, ING

Additionally, Delvescovo is noticing increased engagement from owner-occupiers seeking upgrades, as well as first-time buyers stepping into the market. “There's a clear sense of market confidence returning,” he said.

“We've also seen increased activity from SME customers following recent policy changes designed to make it easy for them to borrow with ING. Many of these customers are drawn to our investor offering.”

The lenders also advised brokers to keep an eye out for fees that could catch their clients unaware and to generally be proactive with their clients.

Read more: Buyer confidence up as housing markets close financial year strong

“At CommBank there are no additional fees specifically for people looking to refinance their loan with CommBank,” Zaka said. “However, customers should be aware of early exit fees from their current lender, as well as general costs associated with a new loan, including application, valuation and legal fees.”

During the refinancing process, Smith also advises brokers to look out for discharge fees from the existing lender, as well as application or establishment fees from the new lender. Other hidden costs, warns Smith, could include lenders mortgage insurance if the customer’s equity position changes, ongoing loan-servicing fees, or break costs for those exiting a fixed rate early.

It’s these potential pitfalls that really bring the broker role into focus.

“Refinancers are an important segment for brokers, making up about a third of their customer base," Smith said. "In the current environment, we expect these borrowers will continue to seek expert guidance from brokers who understand their needs, provide accurate information and explain their loan options.”