Rent yields aren't the be all, end all for property investment clients

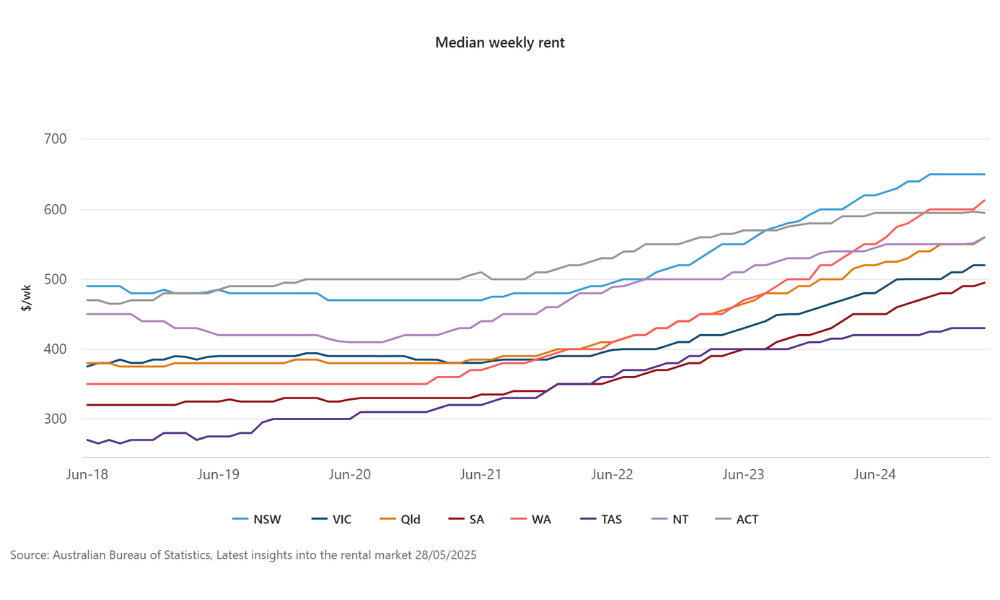

Australia’s rental market became a hot topic this week after Domain’s June 2025 Quarter Rental Report detailed the weakest growth in years for house rents in several major cities, with annual gains at multi-year lows.

Sydney and Adelaide hit five-year lows, Brisbane and Melbourne hit nearly four-year lows, and Darwin hit a one-year low.

For the first time since 2019, combined capital house rents have stayed put for four consecutive quarters.

For units, Sydney, Brisbane and Melbourne had their slowest June quarter since 2021, although Adelaide, Hobart, Canberra, and Perth saw their strongest in years.

Domain contended that “Australia’s rental market is clearly losing steam… With cost-of-living pressures squeezing budgets, many tenants have reached their affordability ceiling, curbing landlords’ ability to push asking rents higher”.

From the tenants’ perspective, this simply suggests that their paychecks have been juiced by the landlords for as much as market dynamics will allow for. As for property investors, they will be weighing up what weaker rental yield growth will mean for future investments.

But Tim Lawless (pictured directly above), Head of research at CoreLogic Asia Pacific, believes that rental yields, while important for property investors, aren’t the be all and end all.

All about the gains

Speaking to MPA, Lawless acknowledged that slowing rental growth “is clearly a disincentive to investors”, but maintained that the prospect of capital gains “will continue to be the primary driver of investor decision making in Australia”.

This preference for capital gains has been evident in recent years. Even as the gap between mortgage rates and gross rental yields widened to levels not seen since the global financial crisis, investor activity surged as buyers pursued capital growth.

With house prices continuing to hit record highs, the bias for capital appreciation is likely to serve investors well for now, particularly with negative gearing remaining a popular investment strategy.

Still, Lawless cautioned that brokers shouldn’t totally ignore rental trends, given the role rental income plays in serviceability assessments. He highlighted extremely low vacancy rates of less than 2% in every capital city, which should help prevent rental yields from falling further, even if they’ve currently plateaued.

Lawless also warned against drawing too many parallels to previous cycles.

“The catalysts for inflections in the housing cycle are actually quite diverse. Historically, interest rate settings play an important role, but so too do access to credit, global shocks and fiscal policy settings," he said.

The role of credit availability was particularly evident during the period of macroprudential policy implementation between 2015 and 2018, noted Lawless, adding that this was amplified by the Royal Commission.

“Previous periods of rate cutting have generally been accompanied by stronger housing market conditions, and we are expecting home values to show a broad-based but modest rise as interest rates trend lower through the year and into next year," he said.

“However, a variety of factors remain that are likely to contain the pace of growth in home values, including stretched affordability, lower rates of population growth and elevated levels of household debt.”

The rental slowdown will have a material impact on the Reserve Bank of Australia (RBA)’s interest rate policy, given the influence rent has on the Consumer Price Index (CPI). Lower rental growth will alleviate inflationary pressures, theoretically allowing the RBA to cut rates faster.

Ironically, this could serve to increase house prices, as more first-home buyers enter the market, enticed by cheaper mortgage rates.

Cheaper rates will also kick the refinancing market up a notch – this is already happening.

Refi boom emerging

Recent data published by the Australian Bureau of Statistics (ABS) showed that refinancing volumes accounted for 40% of all lending commitments in the March quarter. While this was below the refinancing groundswell seen when the fixed-rate mortgage cliff peaked in mid-2023, it was comfortably above the 36% decade average.

Additional data shared with MPA by Commonwealth Bank was even more upbeat on refinancing – it showed that refinancers accounted for 44% of mortgage market share in April 2025, with the banking major anticipating continual growth throughout the rest of 2025.

“As interest rates come down and the lending sector remains intensely competitive, it seems logical borrowers will be hunting for the best mortgage rates,” said Lawless.