Property sales rise, but prices dip in April

New Zealand’s housing market softened slightly in April as cooler weather, public holidays, and persistent inventory weighed on activity.

While sales rose compared to last year, prices eased and listings declined, with affordability pressures persisting.

Median prices slip as buyers remain price-sensitive

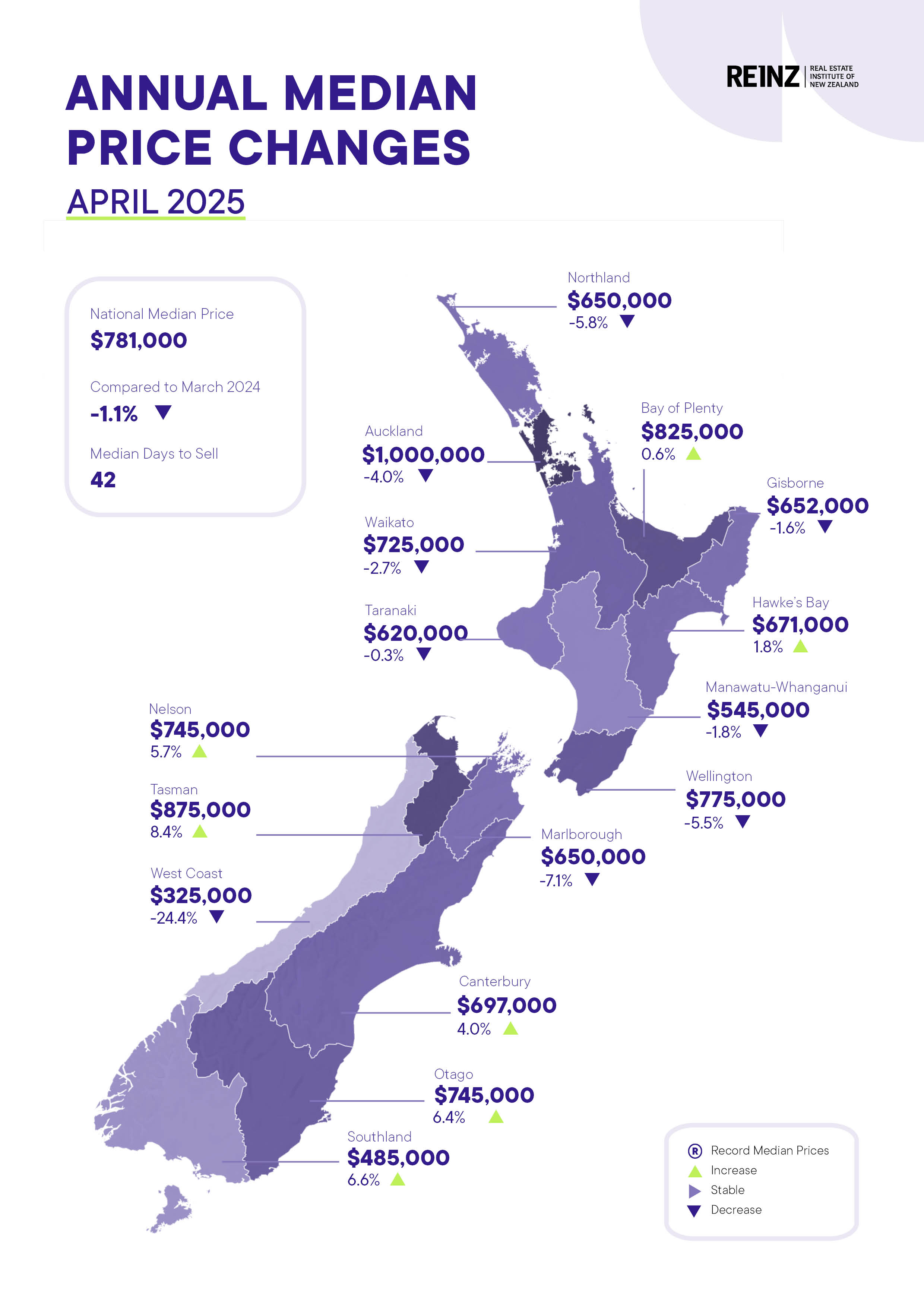

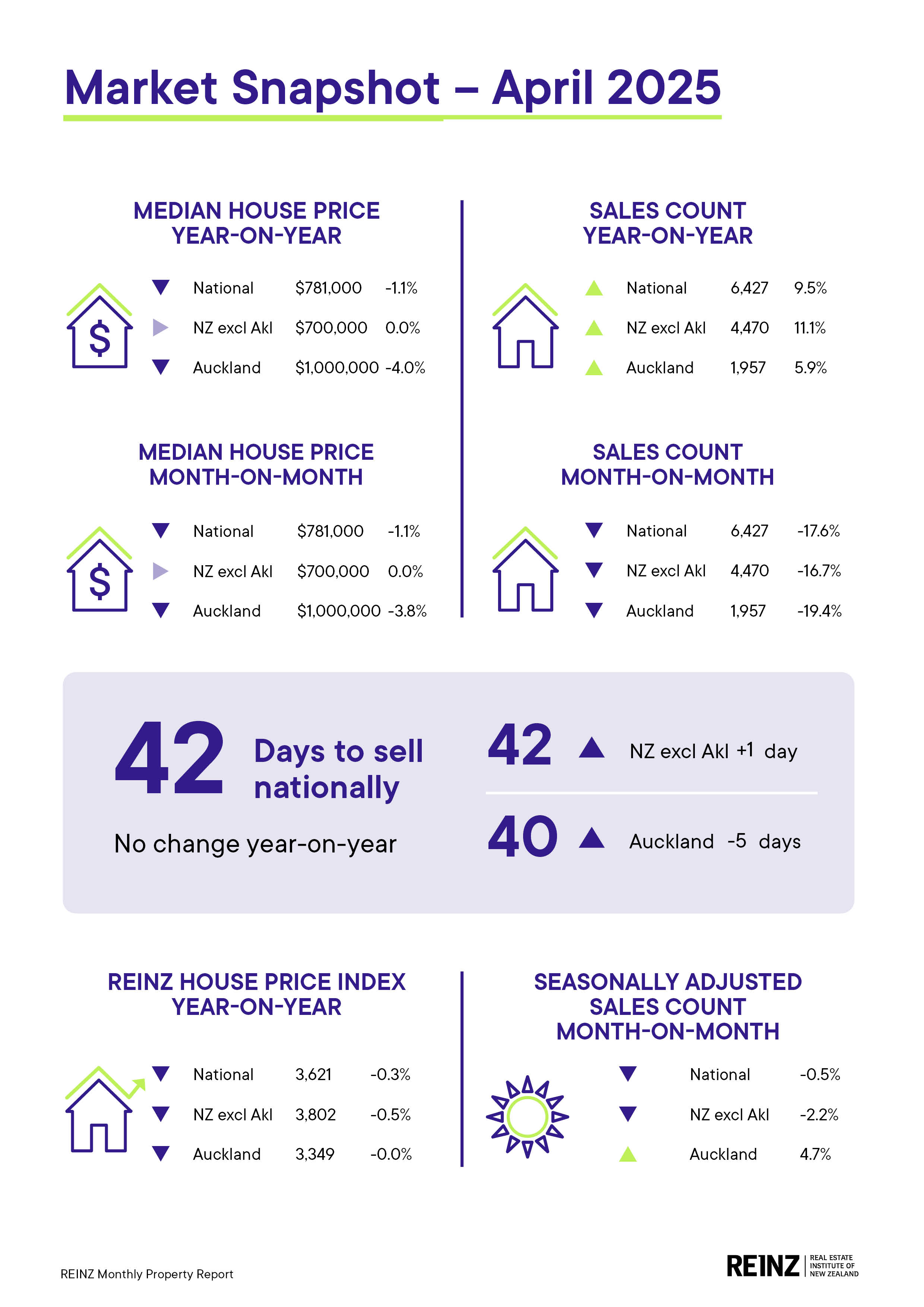

According to the Real Estate Institute of New Zealand (REINZ), the national median house price fell by 1.1% year-on-year to $781,000, with Auckland down 4.0% to $1 million.

Excluding Auckland, prices held steady at $700,000. Seven of 16 regions recorded annual price gains, with Tasman (+8.4%) and Southland (+6.6%) leading.

“There has been a notable increase in sales across the country. However, despite this upward trend, property prices continue to decline due to a significant number of properties still available on the market,” said Rowan Dixon (pictured left), REINZ acting chief executive.

“Buyers are seeking properties at lower price points, and they are willing to explore alternative options if they view prices as being excessively high.”

Sales volumes up, but seasonally flat

National sales volumes rose 9.5% year-on-year, reaching 6,427. Excluding Auckland, the increase was 11.1%. Southland saw the strongest regional growth in sales, up 28.7%, followed by Manawatu/Whanganui (+19%) and Waikato (+17.3%).

However, Dixon noted that seasonal factors distorted the raw sales data.

“Looking at sales activity across New Zealand, the raw data shows a 17.6% drop in activity from March to April 2025,” he said. “However, when seasonally adjusted, this substantial decline becomes just a 0.5% decrease.”

Interest rates ease, but inventory still high

Market sentiment was mixed in April as buyers responded to lower interest rates, yet vendors faced a slower adjustment in pricing expectations.

New listings dropped 11.6% nationally, and inventory climbed 6.2% year-on-year, bringing total inventory to 35,924 properties.

“As interest rates decrease, we can expect an increase in market activity. However, vendors should be aware that prices haven’t yet aligned with these changes and should be ready to adapt to evolving market dynamics,” Dixon said.

The national House Price Index (HPI) slipped 0.3% year-on-year and month-on-month, despite a five-year average annual growth rate of 4%.

Westpac: House price gains gradual, recovery uneven

Michael Gordon (pictured centre), Westpac NZ senior economist, said April’s figures showed continued signs of recovery, helped by easing mortgage rates.

“The REINZ report for April showed a continuation of the gradual recovery in New Zealand’s housing market,” Gordon said. “The house price index rose by 0.4% in seasonally adjusted terms, a modest pickup from the 0.1–0.2% gains in each of the previous five months.”

He noted the strongest gains were seen in Canterbury, Southland, and parts of Auckland, while Wellington continued to lag.

“Lower mortgage rates have helped to revive interest among potential buyers since late last year… we expect to see house price growth pick up over the course of 2025,” Gordon said.

ASB: Market remains subdued, listings key to turnaround

Nick Tuffley (pictured right), ASB chief economist, offered a cautious view, describing the market as mixed and lacking clear momentum.

“The REINZ data for April present a mixed picture, with the overall housing market remaining subdued and without significant movement,” Tuffley said.

“House prices showed a 0.4% increase over the month (seasonally adjusted)… but sales turnover softened after modest upward momentum in Q1, dropping by 1.3% mom.”

Tuffley flagged persistently high inventory levels as a key barrier to price recovery, despite easing new listings in April.

“The primary obstacle to the recovery of house prices remains high inventory levels,” he said. “Although new listings and inventory saw a decline in April for the first time in four months, the decrease is minimal and still leaves the outstanding stock at a decade high.”

Regional standouts: Southland leads gains, Wellington stalls

- Southland continues to top the HPI growth rankings, followed by Canterbury and Otago.

- Wellington saw a monthly HPI drop of 0.3% and remains one of the weakest-performing regions.

- Carterton District was the only territorial authority to hit a new price record, with a median of $790,000 (+46.3% y/y).

Read the full REINZ report here. Also see the Westpac and ASB insights.