South surges, capital cities cool as housing rebalances

March’s data portray a housing market still ticking over, but with more measured behaviour from buyers.

“March shows a housing market holding its nerve. Despite rising fuel costs and global uncertainty, buyers didn’t step away, but they are becoming more cautious and taking longer to make decisions,” REINZ chief executive Lizzy Ryley (pictured) said.

National sales were virtually unchanged year‑on‑year at 7,853, and the median price dipped just 0.3% to $788,000. Excluding Auckland, median prices rose 1.4% to $710,000, highlighting that regional performance is diverging even as national figures appear stable.

Seasonally adjusted numbers point to softer undercurrents. Westpac’s analysis of the REINZ data shows its house price index edging up only 0.1% in March, while sales fell around 4% after a February rebound.

With fixed mortgage rates drifting higher since late 2025, many households are more sensitive to repayment pressures and are taking longer to commit to purchases. Even so, participation remains solid, with Cotality’s latest report showing first‑home buyers now taking just over 27% of national purchases, with smaller mortgaged investors also edging back towards their usual market share.

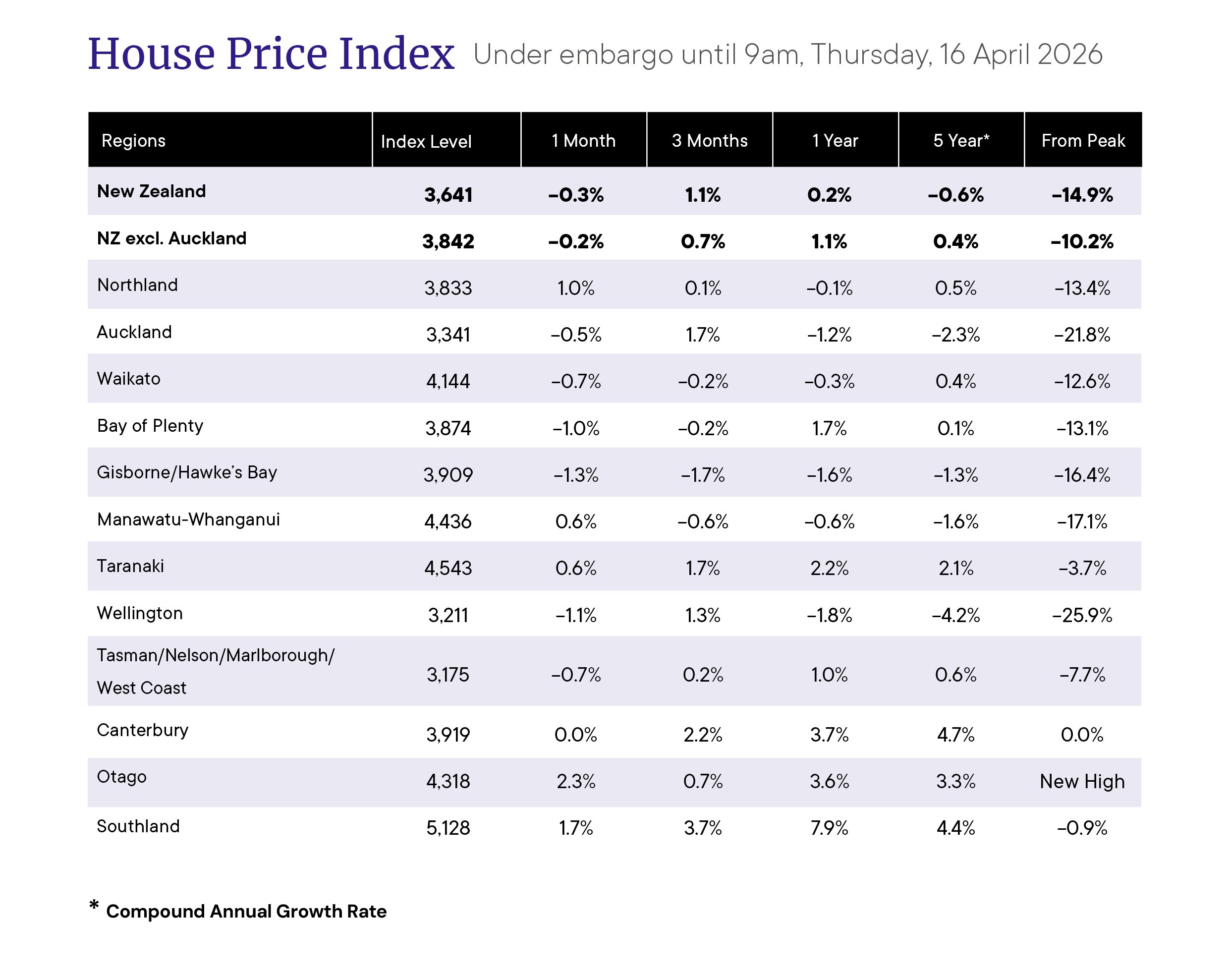

Two‑speed market opens pockets of opportunity

Beneath the flat national picture, regional trends are increasingly important for first‑home buyers, upgraders, and property investors.

Southland led annual median price growth, up 11.8% to $520,000, followed by Nelson at $710,000 and Otago, where the house price index has reached a record high. Canterbury is also close to its previous peak, underlining the relative strength of many South Island markets.

In contrast, Wellington’s median slipped 2.5% to $780,000, while Hawke’s Bay and Gisborne also recorded annual declines. These areas now offer more negotiating power for buyers with solid deposits and serviceability, particularly those entering the market for the first time.

Auctions, days to sell, and the outlook

Nationally, the median days to sell held at 41, the same as a year earlier but 15 days faster than February. This suggests vendors are adjusting expectations rather than withdrawing listings. Auctions remain concentrated in Auckland, Bay of Plenty and Canterbury, where competitive bidding still draws interest for well‑located stock.

Looking ahead, Ryley cautions that “the focus now shifts to what happens next. Any early signs of a ceasefire have been overshadowed by renewed tensions, leaving uncertainty around fuel costs for New Zealand households, and whether confidence begins to rebuild over the coming months.”ASB shares that cautious view, expecting demand to “decrease further over the coming months” amid elevated living costs, rising job insecurity, and higher mortgage interest rates, and seeing subdued demand plus very high inventory as leaving “little likelihood of a lift in nationwide house prices”.

Taken together, those risks suggest the housing market is likely to stay steady but finely balanced through 2026.

Stay informed with the latest housing market trends and mortgage insights — subscribe to our free daily newsletter.