NZ economy rebounds, but risks remain beneath surface

New Zealand’s economy is expected to show early signs of recovery when March quarter GDP figures are released next week.

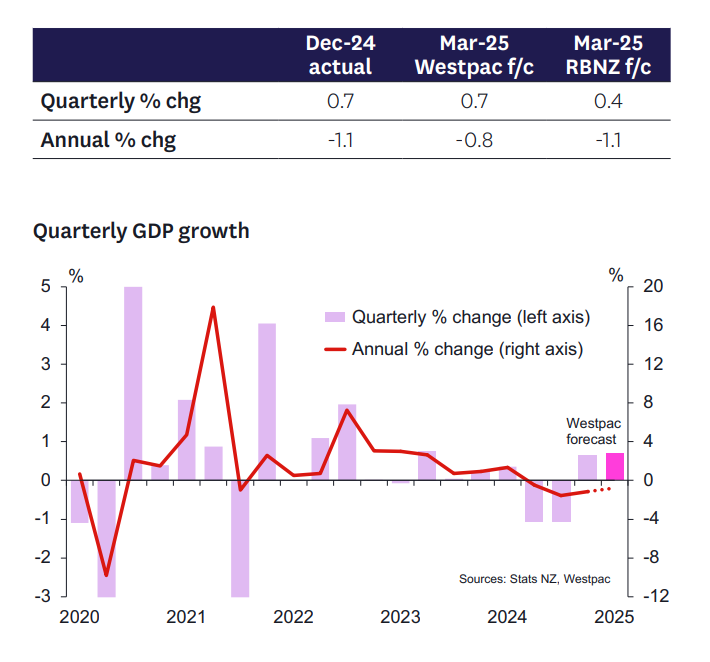

Westpac’s updated forecast now anticipates 0.7% growth for the quarter — an upgrade from its previous estimate of 0.4% — thanks to stronger-than-expected sectoral data released earlier this week.

“Next Thursday’s GDP report is expected to show some green shoots taking hold in the New Zealand economy in the first quarter of the year,” said Michael Gordon (pictured), Westpac senior economist. “Our forecast is for a 0.7% increase in GDP, on top of a similar 0.7% rise in the December quarter.”

Despite the improvement, Gordon noted the economy still faces a weak annual backdrop.

“This follows a sharp downturn through the middle of 2024, and on our forecast would still leave output down by 0.8% on a year ago (and -1.7% in per capita terms).”

Revised GDP forecast strengthens case for OCR hold

The March GDP upgrade aligns Westpac’s view with the Reserve Bank (RBNZ), which also forecast a 0.4% rise in its May Monetary Policy Statement. Gordon noted the better-than-expected data reinforces the likelihood RBNZ will keep the official cash rate on hold at its July 9 policy review.

“Combined with the RBNZ’s declaration of ‘no bias’ going into the July 9 policy review (and no quarterly CPI until after that date), a better-than-expected GDP result would make a strong case for leaving the OCR unchanged on that occasion,” he said

ASB’s Wesley Tanuvasa agreed: “On balance, a more resilient economy supports our view that the RBNZ will pause in July.” Still, he noted that “the behavioural implications of the near-term spike in inflation complicate that task.”

Broad-based growth, but with caveats

Gordon said the signs of strength in the latest data were unexpected, and that the bank’s nowcast model had been sitting much lower — at just 0.2%.

“That does raise a flag for us that some of the upside surprises could be survey noise that won’t be sustained. But nevertheless, they are what goes into the GDP calculations, so we’ve updated our pick accordingly.”

Importantly, the data now suggests a widening base for growth across sectors.

“One thing that we find encouraging is the increasing breadth of the upturn... our indicators suggest that most sectors will report at least some modest growth,” Gordon said.

What’s driving the momentum?

Gordon pointed to several factors behind the lift in activity:

- Easing monetary policy: “New Zealand’s easing cycle is further advanced than most other developed economies.”

- Improving farm incomes: “Agricultural output has been broadly flat... rather, the effect has been through higher farm incomes.”

- Tourism rebound: “It’s an industry with some momentum that has otherwise been lacking in the domestic economy.”

- Possibly softer downturn than reported: “Only time, and data revisions, will tell on that front.”

Productivity rebound or labour lag?

Interestingly, the GDP upturn has occurred alongside a flat labour market - suggesting a spike in labour productivity.

“Putting the two together implies quite a strong rebound in labour productivity, with GDP per hour worked approaching its post-COVID boom levels,” Gordon said.

He cautioned against overinterpreting this as a productivity breakthrough.

“More likely it reflects the usual lags in the labour market cycle... many are finding themselves overstaffed even as demand picks up again,” the Westpac economist said.

Sector highlights: manufacturing, services lead gains

Two sectors are expected to be standout contributors:

- Non-food manufacturing (up 4.6%) led by metals and machinery/equipment.

- Professional and administrative services, although Westpac noted low confidence in indicators for this segment.

“Some of the rise was in metals manufacturing... but the biggest gain was in machinery and equipment manufacturing,” Gordon said.

“The activity data was surprisingly strong given the substantial and ongoing job losses in this area.”

Other sectors expected to post modest gains include construction, retail, wholesale trade, arts and recreation, and forestry. A partial rebound in telecommunications is also forecast.

ASB, which also expects the economy expanded by 0.7% in the March quarter, echoed this mixed picture.

“Services are expected to stay mixed, with resilient tourism supporting strength in wholesale and discretionary services, while pockets of weakness in public services remain,” Tanuvasa said. “But Kiwi spending still looked cautious to start 2025. There seems to be a two-speed economy at play.”

Follow this link to access the full Westpac Economic Bulletin.