From tavern handshake deals to a possible Fannie Mae IPO, the loan that built the American middle class has never stopped changing shape

In 1776, a Massachusetts farmer looking to buy land had no bank to walk into, no rate sheet to compare, and no standardized form to sign. He found a parcel through word of mouth or a notice tacked up in a tavern, negotiated a private multi-year loan with a wealthier neighbor or merchant, and paid in Massachusetts pounds, shillings, and pence — the US dollar did not yet exist, as a recent retrospective on colonial-era home buying notes.

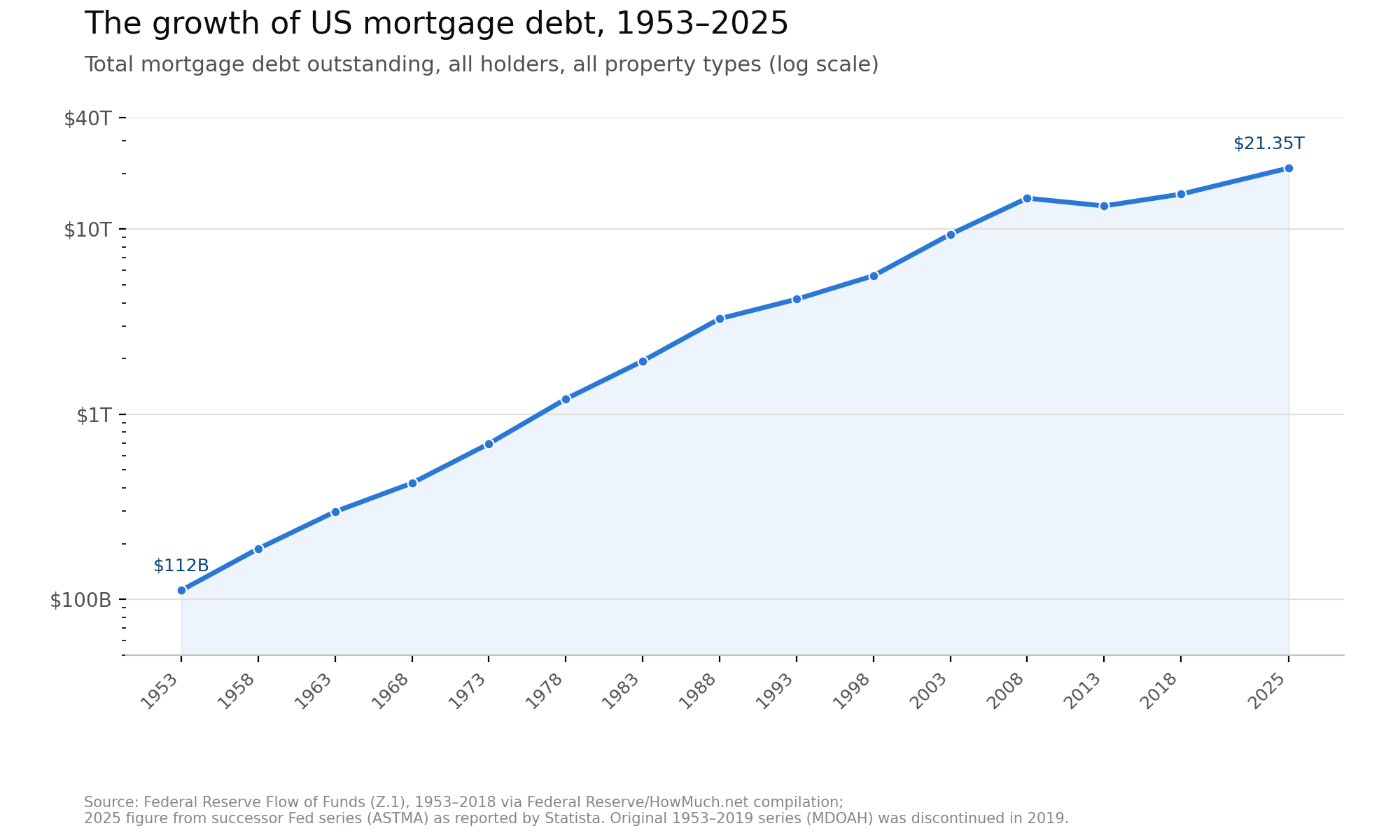

Two hundred and fifty years later, that same transaction underpins $13.19 trillion in outstanding US household mortgage debt as of early 2026, according to the Federal Reserve Bank of New York's quarterly household debt data — a market backed by government-chartered entities, securitized into bonds traded by investors worldwide, and currently the subject of one of the biggest privatization debates in Washington. The story of how American home finance got from a tavern handshake to a possible trillion-dollar IPO is really the story of the country figuring out, generation after generation, how much risk a private lender should carry — and how much the government should carry instead.

A young nation without a mortgage market

For its first several decades, the United States had no mortgage industry in any recognizable sense. Land was the young republic's core asset, but formal, standardized lending against it barely existed. English common law supplied the basic legal scaffolding for secured lending, and the chartering of the Bank of North America in 1781 and the First Bank of the United States in 1791 gave the country its earliest institutional lenders, according to a history of US mortgage lending. But terms, rates, and repayment schedules varied enormously by lender and region, with no federal oversight and no consumer protection to speak of.

That informality persisted for most of the nineteenth century. State-chartered banks multiplied between 1820 and 1860, issuing what one historical account estimates was between $55 million and $700 million in mortgage loans during that period, but the market remained geographically lopsided — capital concentrated in the urbanizing Northeast while farmers and settlers in the expanding West paid higher rates for scarcer credit, according to a history of American mortgage lending.

The National Bank Act of 1863, amended the following year, created a system of federally chartered national banks and a nationalized currency, but it also barred those national banks from directly investing in long-term mortgages — a restriction that pushed real-estate lending toward state banks, trust companies, and a new kind of institution altogether: the mortgage company.

Wall Street discovers the mortgage

The most important financial innovation of the post–Civil War building boom did not come from a bank at all. In 1871, a group of New York financiers — including a young J. Pierpont Morgan on its board — founded the United States Mortgage Company, which originated loans, held them, and then issued its own bonds backed by the value of that mortgage pool, according to a history of long-term mortgages published by the Federal Reserve Bank of Richmond. It was, in essence, a nineteenth-century mortgage-backed security, decades before the term existed, and it funneled European investment capital into American land at a scale individual local lenders never could.

Yet for the ordinary homebuyer, none of this translated into anything like today's mortgage. By the early 1900s, a buyer typically needed a down payment as steep as 40 to 50 percent, and the loan itself ran only five or six years, with interest-only payments followed by a lump-sum balloon payment at the end, the Richmond Fed's history notes.

Building and loan associations, member-funded cooperatives that pooled local savings to lend to their own members, filled much of the gap that banks left, but their loans carried the same short, punishing structure. It was a system that worked reasonably well for the modestly prosperous and shut out almost everyone else — as of the early 1930s, only about one in ten American households owned their home, according to Rocket Mortgage's history of the 30-year fixed-rate loan.

The Depression rebuilds the mortgage from scratch

The system's fragility became catastrophically clear after 1929. Easy, interest-only lending throughout the 1920s had encouraged buyers to take on more than they could sustain, and when the crash hit, an estimated 40 to 50 percent of all home mortgages were in default by 1933, according to a history of mortgage lending published by The CE Shop. Balloon-payment structures that had been merely uncomfortable in good times became a mass foreclosure machine in bad ones, and neither borrowers nor the banks holding their defaulted paper had any real path out.

Franklin D. Roosevelt's response effectively invented the mortgage instrument the industry still sells today. The Home Owners' Loan Corporation, created in 1933, refinanced distressed mortgages directly to keep families in their homes. The National Housing Act of 1934 then created the Federal Housing Administration, which insured lenders against loss on a new kind of loan: fully amortizing, with a term of 20 to 30 years and a down payment as low as 10 percent, according to the Richmond Fed's history cited above.

That structure — a long, fixed, steadily paid-down loan — was so much more attractive to borrowers than the old short-term balloon note that private lenders adopted it themselves to stay competitive. In 1938, the government layered on a second innovation: the Federal National Mortgage Association, or Fannie Mae, created to buy FHA loans from originating lenders and free up their capital to make new ones, establishing the secondary mortgage market that still funds the bulk of American home lending.

The GI Bill, the suburbs, and a hidden ceiling on the dream

The postwar period turned the FHA-style mortgage into a mass phenomenon, and largely for one policy reason: the Servicemen's Readjustment Act of 1944, known as the GI Bill, offered veterans low-interest, low-down-payment home loans through the Department of Veterans Affairs. Combined with a booming postwar economy, the effect on the housing market was extraordinary — the national homeownership rate climbed from 44 percent to 62 percent between 1940 and 1960, according to a retrospective on American mortgage history published by Better.

That boom, however, was not evenly shared. The same VA and FHA underwriting systems that made homeownership newly attainable also formalized racial discrimination through redlining — the practice of systematically denying or pricing loans differently based on a neighborhood's racial composition — and the GI Bill's benefits were, in practice, largely denied to returning Black servicemen, Better's history notes.

The consequences did not stay confined to the twentieth century: a 2022 analysis reported by MPA found that the gap between white and Black homeownership rates had actually widened since the 1968 Fair Housing Act, which Congress passed in the wake of Martin Luther King Jr.'s assassination specifically to outlaw the discriminatory practices the postwar boom had entrenched.

Wall Street returns, and this time it stays

The late 1960s and 1970s rebuilt the plumbing of the mortgage market in ways still visible today. Fannie Mae was privatized in 1968, partly to move its debt off the federal balance sheet, and Congress chartered a competitor, the Federal Home Loan Mortgage Corporation — Freddie Mac — in 1970 to keep the newly private secondary market competitive, according to MPA's profile of Freddie Mac.

Ginnie Mae, created alongside these changes, is generally credited with inventing the modern mortgage-backed security, an innovation that shifted mortgage funding away from local bank deposits and toward the global capital markets — a transformation a ScienceDirect history of mortgage finance calls one of the two truly disruptive periods in American mortgage history, on par with the Depression-era reforms that preceded it.

The 1970s also brought the era's foundational consumer protections: the Equal Credit Opportunity Act barred lenders from discriminating based on race, sex, or marital status; the Home Mortgage Disclosure Act required lenders to report loan data publicly; and the Community Reinvestment Act pushed banks to lend within the low-income communities their deposits came from. None of these fully closed the racial gaps the postwar system had built, but together they represented Washington's first sustained attempt to regulate mortgage lending as a civil-rights issue rather than a purely financial one.

Double-digit rates, deregulation, and the birth of the ARM

Then came the Great Inflation. As the Federal Reserve under Paul Volcker drove interest rates to historic highs to break double-digit inflation, the 30-year fixed mortgage rate followed it upward, hitting an all-time weekly record of 18.63 percent during the week of October 9, 1981, according to MPA's own guide to historical mortgage rates.

Home sales collapsed, and both borrowers and the savings-and-loan associations that held most existing mortgages were caught holding decades-old loans paying far below the cost of the money funding them — a mismatch that helped trigger the savings-and-loan crisis of the late 1980s and early 1990s.

The industry's response was the adjustable-rate mortgage, which shifted interest-rate risk from lender to borrower and, alongside a wave of banking deregulation, permanently diversified the products available to American homebuyers beyond the fixed-rate standard the New Deal had established.

Securitization's long, uneven arc

From the 1980s through the early 2000s, the machinery Ginnie Mae had built in the 1970s scaled dramatically, and Wall Street began packaging not just conventional, GSE-eligible loans but increasingly risky ones as well.

By the mid-2000s, private-label mortgage-backed securities — those without a Fannie Mae, Freddie Mac, or Ginnie Mae guarantee — had grown enormously, financing a wave of subprime lending to borrowers who would not have qualified under FHA-era underwriting standards. When home prices stopped rising in 2007 and 2008, that structure unwound catastrophically, feeding directly into the broader financial crisis and forcing Fannie Mae and Freddie Mac into federal conservatorship in September 2008 — a status neither company has yet fully exited, seventeen years and counting.

The regulatory response, the 2010 Dodd-Frank Act, created the Consumer Financial Protection Bureau and, through it, the "qualified mortgage" rule that now defines the boundaries of safe, standard lending: verified income, a reasonable debt-to-income ratio, and a ban on the interest-only and negative-amortization features that had fueled the crash. It is, in a sense, the FHA's 1934 bargain reasserted for a securitized age — the government setting the terms of a "safe" mortgage in exchange for making that mortgage broadly available.

The conservatorship that would not end

Here is where the history stops being history. Fannie Mae and Freddie Mac remain in conservatorship today, and the Trump administration has spent much of the past year actively exploring what could be the largest initial public offering ever attempted, potentially valuing the two companies at roughly $500 billion, MPA has reported.

Investor Bill Ackman, a longtime holder of stakes in both companies, has put their combined guarantee book at more than $7 trillion — a figure reported by MPA as part of his own case for privatization rather than an independently audited total. FHFA director William Pulte has removed board members at both companies and named himself chairman of each, fueling what Mortgage Professional America described as active preparation for a post-conservatorship future, while forty-six independent mortgage banks have separately pressed regulators to preserve competitive pricing and mission-based lending programs — for manufactured homes, rural borrowers, and condominiums — that a newly shareholder-driven GSE might otherwise be tempted to abandon.

The current housing-affordability crisis has also revived questions about the mortgage's basic shape for the first time in decades. President Trump's floated 50-year mortgage term — described by Pulte as "a complete game changer" — has drawn sharp pushback from brokers doing the underlying math.

Charlotte broker Rebecca Richardson calculated that stretching a $425,000 loan from 30 to 50 years would save a borrower only $290 a month while adding more than $470,000 in lifetime interest, telling MPA flatly: "You're not saving money… you're just dragging out the debt." Fannie Mae and Freddie Mac are currently barred by charter from insuring loans longer than 30 years, meaning any 50-year product would need congressional action and would likely trade as a non-qualifying, harder-to-securitize loan — precisely the kind of product the post-2008 reforms were built to discourage.

Even home insurance, long a peripheral concern for mortgage underwriting, has become a front-line affordability issue: the Federal Housing Finance Agency recently loosened Fannie and Freddie's insurance requirements after premiums hit record levels nationally, with some carriers retreating from high-risk markets altogether and pricing buyers out of homes their mortgage payments alone would have covered.

What 250 years actually taught the industry

Strip away the specific instruments — the balloon note, the FHA loan, the mortgage-backed security, the qualified mortgage — and the through-line of American mortgage history is a single recurring argument about risk. Colonial lenders bore all of it personally and priced accordingly, which is why credit was scarce and homeownership rare.

The New Deal shifted a meaningful share of that risk onto the federal government, in exchange for standardizing the loan into something safer for everyone. Securitization spread the risk further still, across global capital markets, until the underwriting discipline meant to accompany that risk-spreading broke down in the mid-2000s. And the industry's current moment — a possible privatization of Fannie and Freddie, a floated 50-year term, an insurance market straining under climate costs — is, at bottom, the same argument being had again: who bears the risk when a young family signs a thirty-year promise to pay, and what does the government owe them in return for making that promise possible in the first place.

Two hundred fifty years on, the mortgage professionals in that argument have far better tools than a tavern notice board — but the question at its center has not changed nearly as much as the paperwork around it.

For ongoing coverage of the GSE conservatorship exit, mortgage rate trends, and today's affordability debates, see Mortgage Professional America's full industry coverage.