Australia's leading aggregators gather around the table to give their take on the state of mortgage broking in 2025

It’s always a sign of a great conversation when the clock outruns the agenda. Such was the situation at MPA’s latest roundtable, which brought together representatives of the biggest and best mortgage aggregators and two top brokerages to discuss the state of broking in 2025.

The spirited discussion covered themes as diverse as dispute resolution, recruitment, artificial intelligence and broker market share.

But if there was just one takeaway from this hour-long discussion, it was this: the broker-aggregator relationship is in a state of change.

The challenges of being a broker are intensifying amid rapid technological evolution, an increasingly demanding client base and sweeping regulatory changes. Add in the pressures of remaining competitive in a saturated mortgage market, not to mention the simple logistics of running a small business, and there’s no doubt that aggregators need to step up and help brokers more than ever.

Discussing these matters and more around a tightly packed Cafe Sydney dining table were Blake Buchanan, general manager at Specialist Finance Group; Tanya Sale, founder and chief executive at outsource Financial; Gerald Foley, managing director at nMB; Brad Cramb, chief distribution officer at Lendi Group; Rob Thomas, national director at LMG; Them Lam, head of sales and distribution at AFG; Daniel Marsi, chief executive at Liberty Network Services; Phillip Horder, director, national panel partner solutions at Mortgage Choice; Mortgage Choice broker and franchise owner Belinda Sugars; and Robyn Russo, broker and director at brokerage Foster Russo & Co.

A packed table indeed.

How do you, as an aggregator, support brokers at different stages of their careers, while helping them attract and retain customers?

In what became a running theme through-out this hour-long roundtable, aggregators touted the many ways they work with brokers along their career journeys.

Phillip Horder at Mortgage Choice highlighted the group’s Broker Success Program for new franchisees, which covers how to build a successful business, including marketing and lead generation.

“We also go through how to use our systems properly, because we’ve seen that this reduces the cycle time from submission to approval by about half,” said Horder. “So systems training helps new brokers get up and running quicker.”

Mortgage Choice has also built out the seven-month Peloton Program for franchisees poised for their next phase of growth.

“Peloton participants hear from internal speakers as well as external industry experts who share ideas, tips and growth strategies – covering everything from business planning and marketing to operations,” Horder said. “Results from the program have been really encouraging – we’ve seen almost double-digit growth in additional settlements from last year’s cohort.”

AFG's Them Lam discussed how not all brokers have the same goals in mind. “Some brokers want to create a lifestyle; some want to create enterprise businesses that one day they might want to IPO ... Our philosophy is more about understanding our brokers’ needs and serving them the way they want to be served,” he said.

Lam sees the critical importance of helping brokers with their customer relationships, saying: “Historically, over the 30 years of the industry, the focus has always been on residential home loans, write more home loans, write more home loans ... But how do we help our brokers better understand the holistic needs of their consumers and provide them the insights to serve them throughout the life cycle of their journey?”

Gerald Foley said that at nMB, “we’ve taken the approach where we talk about the broker-to-broker business journey. Many prospects don’t come to us as a business, they come as a broker, and we help them evolve along the way to building a broking business.”

nMB has a Broker Benchmarking Program that allows both the broker and nMB to look back on what’s happened through the stages of their business and assess where to go next. “Then we can have a conversation over ‘this is the way the portfolio is performing; let’s have a chat to better understand why’. So it gives our partners that really meaningful contact point,” said Foley.

“Not everyone joins the program, and that’s okay. For some, mortgage broking is a lifestyle thing; [they] just get on with it and do it their way. Others have a real drive to create that broker business.”

For Tanya Sale at outsource Financial, conducting an in-depth business review is an essential piece of the aggregator-broker relationship.

“The business review is, first and foremost, about knowing what our members are wanting to achieve or where they want to go,” said Sale. “Because if we don’t do that first and foremost, then we’ll have no idea what type of support mechanisms, processes or systems to put in place for them. That’s been extremely successful for us and allows us to then drive that business review with the member.”

The process also takes a lot of pressure and time away from the business owner, she said.

“We’re all about the broker not just being a mortgage broker – we want our brokers under outsource Financial to be really good business owners. And that’s how we position their journey with us all the way through.”

Daniel Marsi from LNS said the business “was founded upon offering a high-touch support model – and this objective remains true today”.

Broker recruitment is a core focus for aggregators, Marsi said. “We are attracting both new-to-industry brokers and those who have been broking for 20-plus years. For us, it’s about offering an adaptable model that supports all experience levels.”

Marsi touched on an important point: “We’ve found that what makes a good broker doesn’t necessarily make a good business leader or owner. Helping brokers understand this through leadership coaching has therefore been a significant focus for LNS.”

He added, “Another big shift we’ve seen recently has been around brokers looking to retire. We are in an ageing market, so we’re investing resources to help our brokers with succession planning.”

Brad Cramb spoke at length of how Lendi Group is helping brokers under the Aussie franchise banner via a “one network, many pathways” strategy. It’s a staged program whereby early-stage associates do the hard yards of loan qualification and the like before moving into a home loan specialist role.

“In regard to how we’re helping get and retain more customers, that’s a big focus for our Aussie brand. We’ve announced what we call our 'Find, Buy, Own' strategy. What this is – it’s simply an ecosystem strategy,” said Cramb.

Brokers are doing a lot more than just broking, he added. “They’re helping customers identify, find properties, all the way through to key properties, etc. So now we’re bringing all of that into one.”

Cramb also explained that a big part of helping brokers is in establishing a referral network. “For new brokers, that’s very hard. So we’re automating that and making it available through the platform, so they can get those local engagements – and then keep the customers along as well.”

Aggregators must also work on themselves if they hope to help brokers succeed and develop their businesses, according to SFG's Blake Buchanan.

“We need to provide a strong home focused on what today looks like, what tomorrow looks like, and the entire team are educated on what’s coming down the barrel,” he said.

But it’s not the aggregators’ job to tell brokers who and what they should be, said Buchanan. “Our job is to make sure they maintain standards, operate within best practices and principles, and, most importantly, that we understand them, understand their goals and assist them on the journey to achieving those goals.

“And we do that through… individual strategic support and investment in their businesses.”

LMG has been on a big push to clearly define its two main service offerings for brokers under the LMG and Loan Market brands. Naturally, Rob Thomas grasped the opportunity to set the record straight on what each brand offers.

“On the LMG side we have quarterly meetings where we teach them all things around our tech offering with MyCRM to save them time and keep them safe by our compliance design software. We also offer the support of state-based compliance coaches," Thomas said.

“If they do want support in growing their business, they can go on the Loan Market side where we offer monthly support. We’ve also introduced a program in Loan Market called Elevate, which involves peer-to-peer learning as well as personalised coaching. That’s one we’re really focusing on in the coming years.”

While Thomas conceded that the industry probably hasn’t done the best job in guiding brokers through the diversification age, he hopes the MyCRM Diversified tech stack, “which is an all-in-one platform for residential, asset finance and commercial”, will be a game changer.

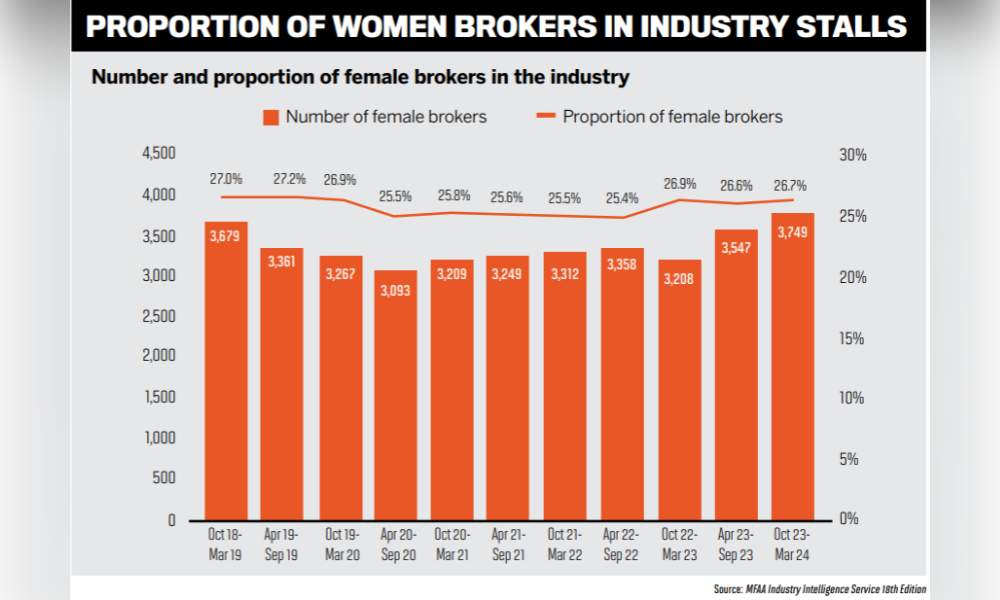

Broker question from Belinda Sugars: Businesses need staff to grow. How can we attract talent – including women who may be juggling family responsibilities – into the industry through training, qualifications and career opportunities?

As always, the discussion heated up following an off-script question from guest broker Belinda Sugars, a franchise owner at Mortgage Choice.

Sugars pressed the roundtable participants on what they’re doing to attract talent to the industry. Women, noted Sugars, are especially underrepresented in the broking industry and, despite efforts, the female-to-male ratio has shown little to no signs of changing.

“So what are we doing to change that? The training, the qualifications – it sounds like you’ve got great things happening, but what is the best practice? What can we do to make this a career that people want to be in?” Sugars asked.

While gender representation is a valid concern, the roundtable ultimately broke out into a discussion about gatekeeping.

As Buchanan said, “It’s still valid that half of new entrants to the market fail in the first couple of years, and it’s been like that for a number of years. That tells me that as an industry we have that part wrong.”

Buchanan drew attention to the insurance broking industry, which, he admitted, “is in some ways more advanced than us in that they’re required to work with a brokerage for two years, not just be mentored by one”.

He continued, “I think we could look at changes here. If we look at the DNA of our industry – over 40% are single-operator brokers. And over the last 10 years, we’ve had a growing burden: more compliance, best interest duty, technological advancements, and so on. So is it fair to say that the broker of yesterday – who could be the business owner, the marketer, compliance and the client manager all at once – can still do all of that today at the same level of applications and quality? Probably not in most cases.”

Sale had some strong thoughts on the matter of bringing talent into the broking industry. “There’s one thing we don’t sway away from: we pick and choose,” she said.

In Sale’s view, the broking industry often gets it wrong with new entrants. “There are aggregators in this industry that put on new entrants for the sake of putting on new entrants, so they can get a nice little cash flow for doing virtually nothing. If we’re going to attract new people into our industry, we must pick and choose what that new entrant is going to look like … We want people who are going to be serious. But then, this industry has to be serious about putting them on.

“We’ve got to have the support mechanisms in there. You can’t let these new entrants go broke within the first six to 12 months.”

Education clearly plays a big part in attracting the right talent. But here, too, the broking industry is lacking.

Thomas has seen this play out in his own home. “I was talking to my kids – they’re all going to school this fall – and none of them knew what mortgage broking is. They’re like, ‘What’s that, Dad?’ So we’re missing something,” he said.

It doesn’t help that school students cannot currently do a Cert IV in mortgage broking. “Why aren’t we going into schools and talking about lending and improving financial literacy before that generation leaves home? We just don’t talk about it as an industry. That’s what I want to change,” said Thomas. “We’ve launched Brokerversity. In less than 12 months, we’ve had 150,000 courses completed. Over 200 people have already completed their Cert IV through the platform.”

Thomas said that LMG doesn’t bring new talent into the industry directly. “We don’t bring people directly into the industry ourselves. As a business owner, we don’t onboard someone fresh unless they come under an existing loan writer – so they join the industry through a current business.”

Unfortunately, decent young brokers face difficulty in commanding respect during the dealmaking process.

“I put a very smart 18-year-old in front of two 40-year-old people buying a house, and they just don’t take them seriously,” guest broker Robyn Russo of Foster Russo & Co told the roundtable. She has even seen decent, intelligent young brokers leave the industry after confrontational, even mortifying, experiences.

However, Sale had limited sympathy with the issue. “You cannot put an 18-year-old in front of people buying a home, which is probably one of the largest transactions they may ever have, because that person does not have any life skills,” she said.

When it comes to the skills new entrants need to make it in the competitive world of broking, Lam stressed that the industry should be looking far beyond the finance space.

“It doesn’t matter what they [studied],” said Lam, “especially because attitude and aptitude often trumps experience. “Because if someone is sitting in front of them looking for a job, and that person is also considering a role at a bank or in a branch, or in a corporate setting, then you – as a small business – have to be that much better at delivering your employee value proposition.”

Attitude is a hard thing to coach, added Lam. “But the truth is, we work in such an amazing industry. Yet we’re still not seen in the same regard as accounting or financial planning, or the rest of it.”

Lam believes there is a generational shift happening in the industry. He said, “We’re seeing a lot more new entrants into our businesses, and we’re fortunate to have broker groups of different sizes that are looking at hiring or adding people into their businesses. It’s about helping our members build an employee or broker value proposition that attracts talent, whether they’re 18 or 19, someone making a career change, or mums or dads returning to work after time off to raise children.”

Unsurprising given the AI buff he is, Cramb sees the latest technological revolution as crucial to spurring broker growth. Lendi Group has already adopted AI for certain high-volume, low-value tasks, with the fundamental purpose of allowing brokers to focus on the important work of growing their businesses. A lot of this comes down to the technologies brokers have at their fingertips.

“If we think about our customer model today, the broker is sitting in the middle of the transaction, relying on providers left and right from that transaction, from property portals all the way through to conveyancers, buyers’ agents and so on,” Cramb said.

“What’s happening is we’re effectively handing the customer off to those third parties. They might be referral partners, but we’re still handing them over.

“Our view is: keep it on your platform – as a franchisee or broker – and also participate in the monetisation of that work. In other words, you’re getting a return from it, and that’s the best model.”

Horder brought the conversation back to the gender divide, highlighting that women represent an above-industry-average 34% of the brokers in Mortgage Choice’s network.

“Through our Aspire program, which supports the female talent in our network, we also focus on attracting women into Mortgage Choice," he said.

“For example, as part of our recruitment strategy, we highlight the benefits of a career in broking to attract more women recruits.

“Each franchisee will approach recruitment in a way that suits their unique business needs. There are some fantastic examples of brokers in our network who have created a supportive working environment that allows their staff, many of whom are working mums, to work flexible hours, outside of a normal nine to five, which has helped them not only attract the right staff but also keep them.”

AI advancements are making everything quicker, easier and much more streamlined, but not necessarily safer. How are you implementing technology in a sustainable way?

The inevitable discussion around AI can be summed up as follows: yes, there is a lot of hype around the word, but brokers risk falling behind if they don’t move with the times.

“AI is something that both scares and excites us,” said Thomas.

But scary or not, “I do think that people who don’t embrace AI will be replaced. I reckon the brokers who embrace it will charge forward,” he added. LMG is in the process of implementing AI features into its MyCRM system, having assembled a team to get the ball rolling.

“Because our idea of AI is this: we want our brokers to use it to get better,” Thomas said. “I think the competition isn’t just with the banks – and yes, they’re coming back pretty hard at us – but the real competition is broker to broker … and we want our brokers to be better.”

LNS “takes a measured approach to AI”, said Marsi, adding, “We want to make sure what we’re incorporating into our business is adding genuine value for our brokers.”

Marsi and the LNS team see the benefits of AI in streamlining broker processes and making existing platforms more efficient, but he stressed the importance of keeping a genuine face-to-face broker-to-customer dynamic.

“It’s not about taking brokers out of the equation, but rather asking how technology can streamline, speed up and enhance day-to-day operations, including engaging with staff and clients,” Marsi said.

Horder discussed the virtues of using AI to eliminate the pain points of writing loans, citing an “intentional approach” to building AI support at Mortgage Choice. “Where are the low-value, repeatable processes that could be automated with AI?” he asked. “How can we solve those problems so brokers can focus on the things that matter most?”

Furthermore, Mortgage Choice is also providing brokers with monthly reports that use AI modelling to identify which customers have the highest propensity to refinance.

Foley came through with a bit of a reality check on the whole AI conversation.

“First, I just want to say – I think we use the term AI too quickly now, when what we actually mean is automation. AI is a component of that,” he said. “Everyone jumps to AI as the total solution, but when you really talk about it, what we’re actually doing is making the whole process better.

“And we’ve always looked to do that. Now there are new tools, yes, but that’s the observation – it just seems trendy to say ‘AI will do this’ when it’s just part of a bigger picture.

“We see AI as just one part of doing things better and faster. It’s not the whole thing, just a piece of the puzzle.”

Buchanan agreed that “a lot of [AI] is hype”. He warned of the monumental risks to data privacy involved in using AI tools, saying, “If you’re going to integrate AI into your business, you really need to study it. Check the words, check the data – because you need to know which country that data is being stored in and who’s going to have access to it.”

Lam also touched on the security issue. He said, “Our priority first and foremost is to ensure a safe and secure environment for our members to operate by way of a robust cybersecurity policy/framework.

“We have a product team that consists of key people across departments that drives the development and implementation of services and digital tools that integrate into AFG’s technology offering. This will continue to evolve, with one of the key drivers being how those tools enhance the productivity of our members and the experience it delivers to their customers.”

The aggregators all agreed that the fundamental purpose of being a broker will never change, regardless of what fancy new technologies emerge.

In Buchanan’s words, “Think about accountants – most of us still go to our accountant every year for validation. We can do our own tax returns, but we need an expert to validate our deductions, our choices, the structural decisions we make in our businesses.

“Likewise, clients will be looking for brokers to help structure home loans, validate their choices and educate them moving forward. AI will be part of our evolution, yes, but it’s not the end of our industry.”

After all, “you can’t license AI to give credit advice”, he said.

Broker question from Robyn Russo: What is the aggregator’s role in handling disputes?

Russo recounted the first serious complaint she received about a lender her brokerage works with, which, as luck would have it, came just a day before the roundtable. While she had managed to talk the customer out of filing a complaint with the Australian Financial Complaints Authority, Russo was keen to hear how aggregators could help brokers facing a similar situation.

Sale responded: “I’m very passionate about this because [aggregators] do need to get involved, especially when you’re dealing with a situation where someone uses those four letters. As soon as AFCA is mentioned, you’d want to get your aggregator involved.

She added, “[outsource] could guide you on things to say, how to alleviate the worries of that client and how to manage the situation. It’s a joint effort – it’s a shared responsibility here.”

Marsi mentioned LNS’s central complaints resolution team, where brokers can come to the group before a situation escalates. “We encourage those discussions to happen,” he said. “We provide general guidance around how to manage the situation and how to engage with the customer.”

Thomas noted that brokers are very rarely the source of complaints (just 0.1% of AFCA complaints are about brokers, he pointed out). But when issues do arise, “we are 100% behind our brokers, and we encourage them to contact us early if they ever come into trouble”.

Brokers should get LMG involved as early as possible, Thomas added.

At Mortgage Choice, “if a broker has an issue, we get involved very early”, said Horder. “We’ll obtain the details, investigate and work out the best path to a resolution. At the end of the day, we want to make sure the broker’s doing the right thing – and that the customer is getting the experience we expect. If there’s been a breakdown, we want to understand where that happened and why, so we can fix it.”

In Lam’s view, dispute resolution should be considered a cornerstone of mortgage aggregation. “Structurally, I think this is core to the value proposition that an aggregator should provide,” he said. “A lot of the things that aggregators do might be underappreciated by members at times – not because they don’t value them but because they don’t always know what’s happening behind the scenes until something goes wrong. It’s a bit like insurance.”

Providing a framework of education for the entire broker network is also essential. As Lam explained, “It’s also about teaching business owners to spend time on the people side of the business, asking, ‘how much time are you spending one-on-one with your staff to ensure they’re capable of performing the functions you’ve hired them for?’ It’s about doing that pre-work so the issues don’t arise in the first place.”

As a senior industry figurehead, Foley has seen AFCA take a more reasonable approach to handling complaints (although Buchanan argued that “nearly every time it goes to AFCA, you’ve already lost the battle in some way anyway”).

Foley stressed the importance of understanding the situation a customer is in and helping them resolve that situation. But he also recommended that brokers maintain a degree of separation in the dispute process.

“Our first step is usually to understand what the complaint is about: is it an unreasonably dissatisfied customer based on a decision they have made, or is the broker or someone else actually at fault?” he said of the nMB process.

However, maintaining a degree of separation can be difficult when, as Sugars pointed out, many brokers have no idea how their aggregator can help in these stressful situations. Hence the importance of having these conversations.

At Lendi Group, licensing plays an important part in handling complaints. Cramb said, “All of our brokers operate under our licence – and that’s different depending on which aggregator you’re with. So there’s a big responsibility on us to make sure things are handled properly.

“We also work with lenders – if a complaint goes through the lender, in many cases we’ll deal with that complaint directly and handle it on the broker’s behalf.”

Buchanan added that SFG “would ensure that the broker knows their obligations. We would communicate with the client, with the broker’s permission”.

You can’t win them all, though. “Sometimes the broker is at fault, and in those cases it’s about saying, ‘Well, listen – have you considered settling? Have you considered making reparations in this way?’” said Buchanan.

What are your predictions for broker share of the mortgage and commercial finance markets over the next 12 months?

Most readers will not need reminding of the immense growth in broker dominance of the mortgage market. At the latest count, nearly 80% of all home loans originated through the broker channel. While commercial loans are closer to 40%, that only means the opportunities for growth are huge.

“I think resi is about there, but we’ll have less brokers owning the share versus a long tail that we currently see,” Foley said of the market. “The current tail is going to have to be chopped somewhere on resi. It would be nice if the share number started with an eight, but around the 75% share is reasonable and sustainable.”

Like all others gathered around the table, Foley believes commercial broker share is set to grow, but he made a salient point about who will be on the other side of the deal, as many commercial lenders are looking to become brokers themselves.

“I do worry about who brokers will be sending their commercial deals to in the near future, because good commercial bankers are becoming brokers. I don’t know what that’s going to look like,” Foley said.

Banks need to evolve quickly, he continued. “They have to build the skills to receive those [commercial] applications properly – and maybe that’s through automation. I think it might go that way, and that worries me as I see the human assessment skills as more important to good decisioning in commercial lending.”

However, Foley took comfort in the fact that banking leaders are aware of these issues and are drawing up plans to address them.

In Horder’s view: “If you look at the macro environment, it’s more complex than ever. There are more legislative and compliance requirements, and we’re seeing a lot of economic uncertainty. So there’s a really big role for brokers to play in helping clients navigate all of that.

“The value of broking – and of being a broker who can provide guidance to help borrowers make the right decision – is even more critical in this market. I think it carries greater consequences.”

Thomas is predicting commercial market share to have a five in front of it, in percentage terms, by 2028. “That’s why we’ve launched MyCRM Diversified – to make it easier,” he said.

Buchanan concurred that commercial deals present the biggest opportunity for broker growth, saying, “The suggestion is that commercial broking represents between 30% and 40% of origination. So just from a data perspective, that is the biggest opportunity in this channel. And for the last three years, it’s been the fastest-growing part of our business – so definitely commercial.”

Cramb continued, “The good news is we don’t have to convince customers to come to brokers; they already are and will continue to do so. For our view, owning more of the experience is part of the growth strategy for brokers. That’s why we’re moving towards the left and right of the transaction, as mentioned earlier – bringing in buyers’ agents, conveyancing, insurance; integrating those into the ecosystem.

“It’s about helping brokers participate in the economics of that journey. These are services customers need. They reduce friction for the customer, reduce friction for the broker – and there’s a monetisation opportunity as well.”

Marsi also contended that commercial is the future. He said, “LNS is focused on supporting brokers with opportunities outside the residential space, including commercial lending. We help provide our brokers with the tools they need to diversify beyond the residential space.

“I believe that given the increased number of brokers in the industry now, you have to diversify your business to remain competitive. We want to make sure we’re providing the support to help them do exactly that.”

At outsource Financial, it’s all about balance, Sale said. “How they’ve achieved that – and how we’ve helped them achieve it – is through commercial, asset and personal loans.”

Sale cited concerns about ill-equipped brokers losing business if they don’t have the right referral mechanisms in place. Some brokers, according to Sale, are concerned that they don’t have the relevant skills to write complex commercial deals, but they’re equally worried about losing clients if and when they need to refer out.

“They still wanted the opportunity to refer it out while maintaining oversight of the transaction,” said Sale. “So we built two internal divisions to cater for that. And through our mentoring programs we’ve also grown the commercial, asset and personal loan space big time over the last two years – all with the goal of creating a fully balanced business.”

Lam has the last word of the day with a prediction of 80%-plus broker dominance in the residential sector.

“When we talk about the next three to five years, I feel like the value of what we do as an industry will continue, and we need to embrace technology as our market share accelerates beyond 80%,” he said.

So, what were the key takeaways from MPA’s latest aggregator roundtable?

Healthy competition is plentiful, the broker-aggregator relationship is only going to become more important, and there is a palpable sense of optimism in the air – as long as the right talent is encouraged into the sector.

Read more: 2025 Brokers on Aggregators