One sector is seeing the worst delinquency surge in years

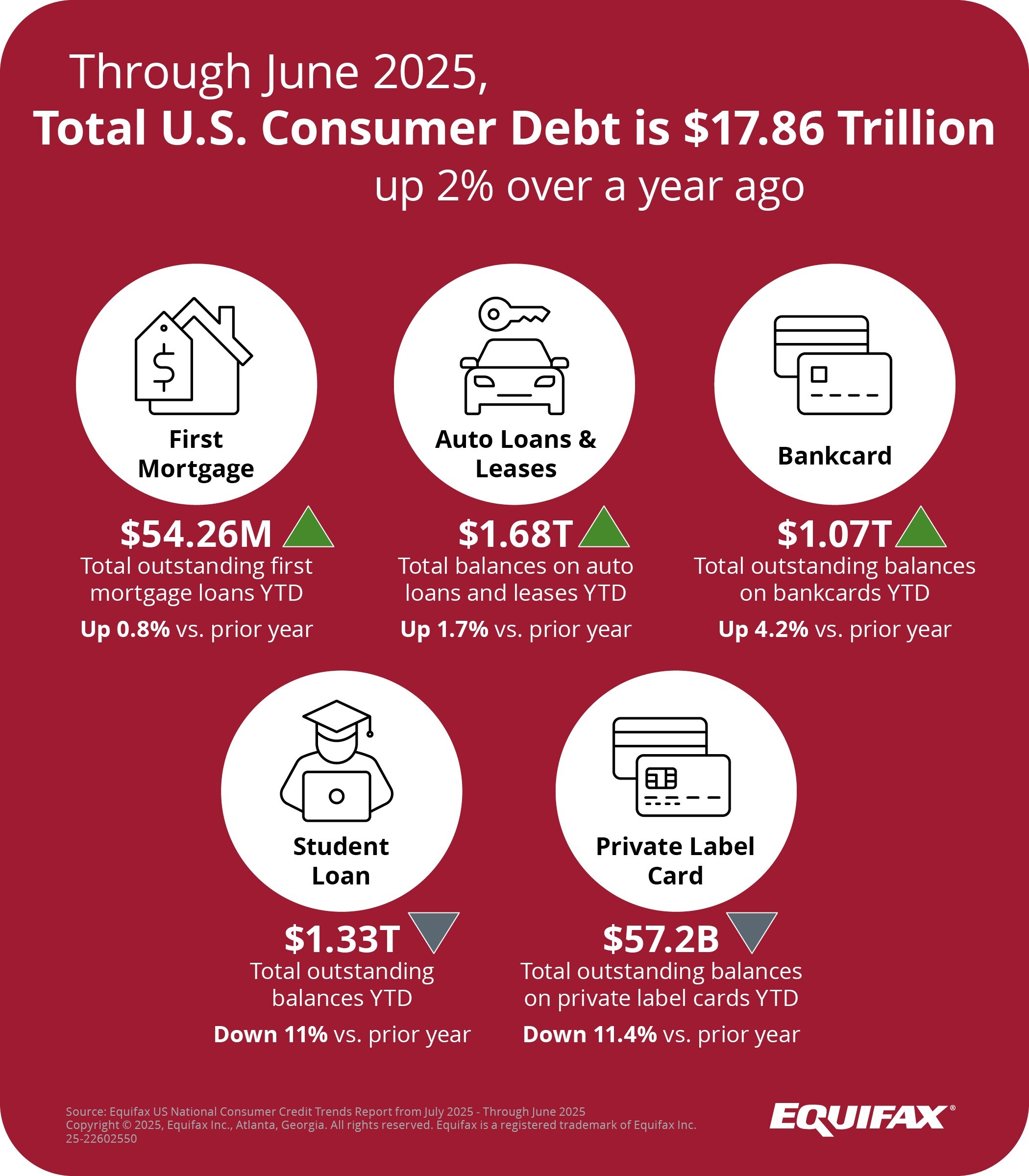

Consumer debt in the United States climbed to $17.86 trillion in June 2025, marking a 2% increase from the previous year, according to Equifax’s second quarter Market Pulse report. Despite the rising debt levels, overall delinquency rates held steady at 1.5% for the third consecutive month.

The Atlanta-based credit reporting company’s data reveals a complex picture of American consumer finances, with spending continuing across categories while certain borrower segments show increasing strain.

Subprime borrowers face growing pressure

The report highlights a concerning trend among subprime borrowers, who now hold 22.1% of all bankcard debt as of May 2025. This represents a 3.5% increase from May 2024 and a significant 50.9% jump from the pandemic low of 14.7% in May 2021.

“At the surface level, our second quarter data showed that consumers are continuing to spend and avoid delinquency. However, there’s a growing K-shaped split in the consumer landscape, with subprime borrowers falling behind,” said Tom O'Neill, market pulse advisor at Equifax.

Total bankcard debt for subprime borrowers surged 135% to $233.1 billion in May 2025, compared to $99.4 billion in May 2021, while overall consumer bankcard debt grew just 54% during the same period.

Student loan crisis emerges

Student loan debt presented the most severe deterioration among major lending sectors. After resuming delinquency reporting in 2025 following a five-year suspension, severe delinquency rates doubled from 6.48% to 13.49% in March, climbing to 18.73% in May before declining slightly to 17.95% in June.

Outstanding student loan debt dropped sharply to $1.33 trillion in June 2025, representing an 11% decrease year-over-year. The number of active accounts fell 15.6% to 146.7 million.

Credit cards show stability

Bankcard credit balances reached $1.07 trillion in June, up 4.2% year-over-year, with total accounts increasing 5.7% to 581.6 million. Delinquency rates showed improvement, falling 4.4% year-over-year to 2.79% in June 2025, down from a peak of 3.22% in November 2024.

Auto market shifts to leases

Auto loan and lease debt totaled $1.68 trillion in June, with lease balances surging 13.6% while auto loan balances rose just 1.1%. Lease delinquencies dropped to 0.42%, contrasting with auto loan delinquencies that edged up to 1.5%.

What are your thoughts on the latest findings? Share your insights in the comments below.