Foreclosures rose again, with experts warning of persistent borrower strain despite Fed rate cuts

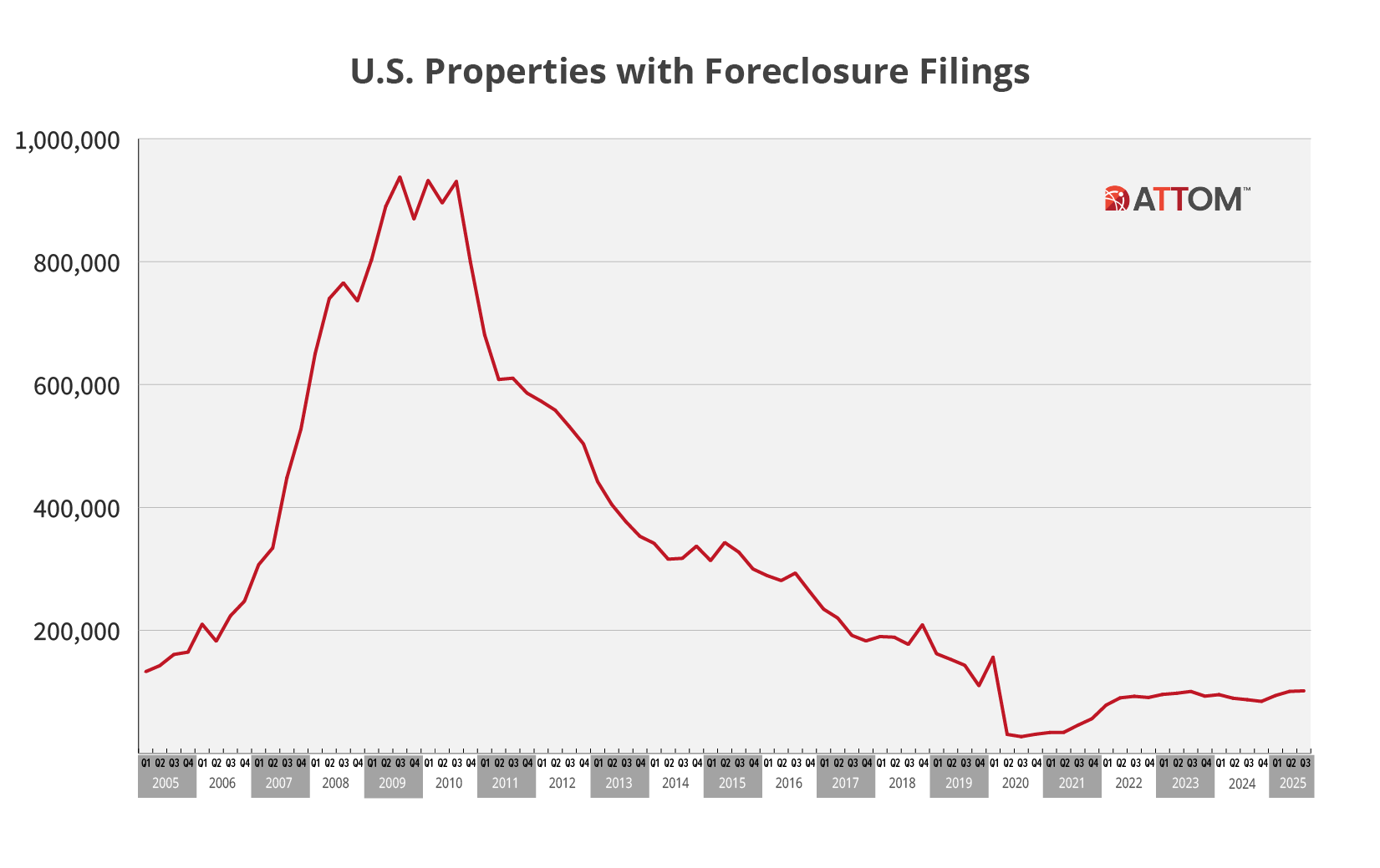

Foreclosure activity in the United States continued its slow climb in the third quarter of 2025, with new data from ATTOM showing a total of 101,513 properties hit with foreclosure filings. That's a 17% jump from a year ago and a marginal uptick from the previous quarter.

“In 2025, we’ve seen a consistent pattern of foreclosure activity trending higher, with both starts and completions posting year-over-year increases for consecutive quarters,” Rob Barber, CEO at ATTOM, said.

“While these figures remain within a historically reasonable range, the persistence of this trend could be an early indicator of emerging borrower strain in some areas.”

Foreclosure starts rose 2% quarter-over-quarter and 16% year-over-year, with TTexas (9,736 foreclosure starts); Florida (8,909 foreclosure starts); California (7,862 foreclosure starts) leading the pack.

Houston, Texas (3,763 foreclosure starts); New York, New York (3,452 foreclosure starts); Chicago, Illinois (3,144 foreclosure starts) topped the list of major metros for new starts, reflecting a broad-based uptick across both Sun Belt and Rust Belt markets.

Florida, Nevada, and South Carolina posted the highest foreclosure rates, with one in every 814, 831, and 867 housing units, respectively, receiving a filing in Q3.

Lakeland, Florida, and Columbia, South Carolina, stood out among metros, each recording rates more than double the national average.

Lenders took back 11,723 properties in Q3—a 33% jump from last year. Texas and California led the nation in repossessions

Despite the increase in activity, the average time to foreclose dropped to 608 days, a 25% decrease from last year, continuing a downward trajectory since mid-2020. Louisiana and Nevada reported the longest timelines, while West Virginia and Texas saw the fastest completions.

Broader economic context and industry outlook

The rise in foreclosures comes as the Federal Reserve’s recent 25-basis-point rate cut has done little to ease pressure on debt-laden homeowners. Fintech company Unlock’s survey found that 59% said the Fed’s rate drop did not motivate them to buy, sell, refinance, or take on new debt.

Rate cuts may offer some relief, but with inflation and mortgage rates still elevated, many borrowers remain on the edge. Glen Weinberg, managing partner at Fairview Commercial Lending pointed to deficit spending, and other macroeconomic factors as reasons why mortgage rates have remained stubbornly high.

"My personal opinion is that the Federal Reserve is going to gradually cut rates, but we're going to see mortgage rates kind of kick around in that 6.5% to 7.25% range through the end of the year. I don't see a huge movement in rates - which is also going to impact foreclosures because the market has this perception that the Federal Reserve is going to bail real estate out, and the Federal Reserve can't," he told Mortgage Professional America.

"Regardless of how much they cut rates, because of inflation and market expectations, mortgage rates are going to stay high - which is going to continue to impact the real estate market."

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.