New analysis found trimming small luxuries could shave years off saving timelines

For young renters staring down six‑figure home prices and 6% mortgage rates, the problem often looks too big to solve. A new analysis from Mortgage Research Network argued the first step might be as mundane as cancelling a subscription or skipping a delivery.

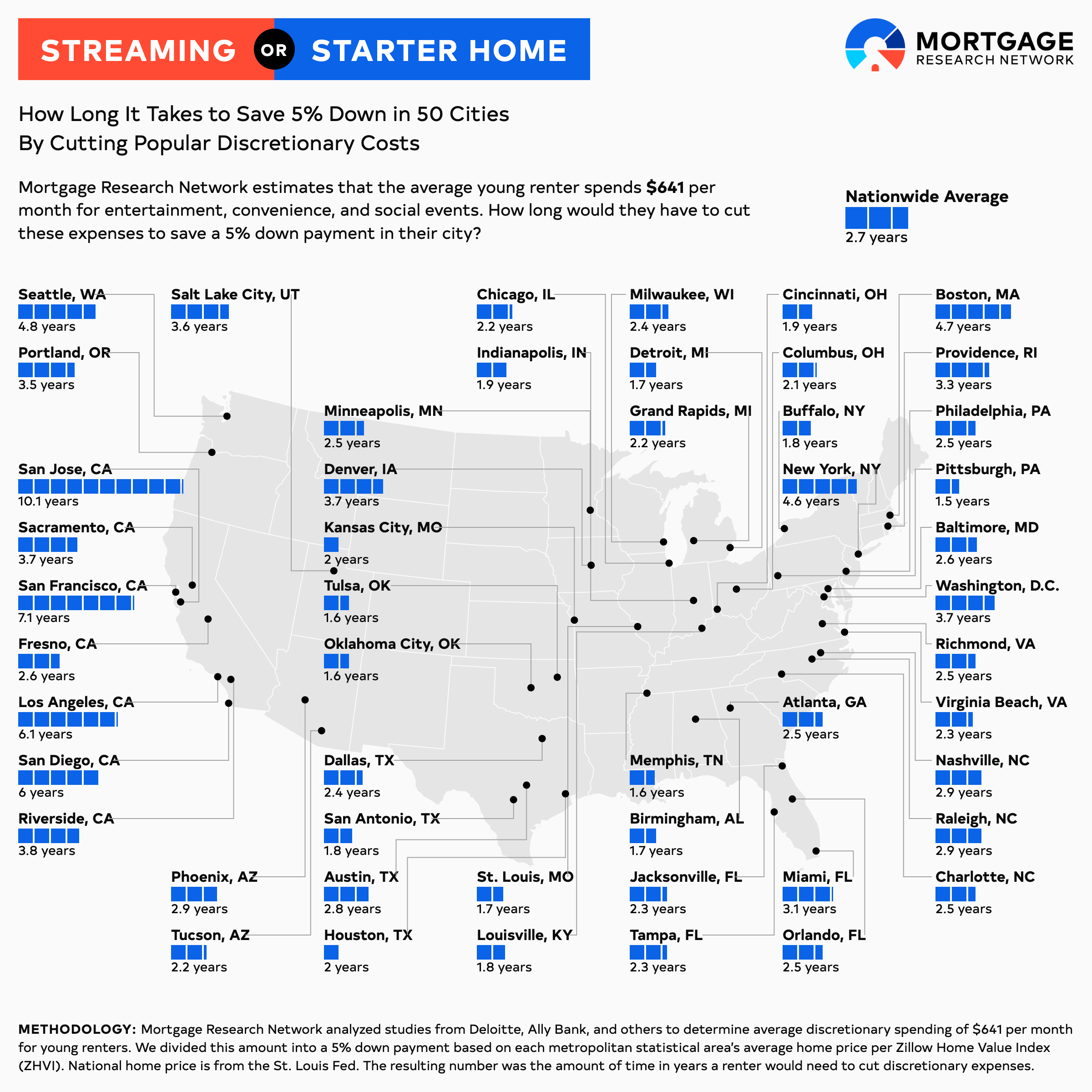

The study, “Streaming or Starter Home?,” examined four common categories of discretionary spending among Gen Z renters – video and music streaming, food delivery, social activities and shopping. The study estimated they totaled about $641 a month, or nearly $7,700 a year, based on data from Deloitte, Ally Bank and other industry surveys.

Redirected into savings, that sum would have been enough to fund a 5% down payment on a median‑priced home in roughly 2.7 years nationally, and in three years or less in 35 of the 50 largest US markets, assuming prices and spending patterns stayed constant.

Renters in Pittsburgh could have reached a 5% down payment in about 1.5 years. In high‑cost markets, the math looked punishing: the same savings rate would have taken more than seven years in San Francisco and just over a decade in San Jose.

“Gen Z isn't going to give up every convenience any more than Gen X would have given up buying Nirvana CDs,” Tim Lucas, report author and lead analyst at Mortgage Research Network, said.

“But this study shows that there are non‑essential expenses almost anyone can cut to reach a financial goal, whether that's homeownership, investing or building an emergency fund. Starting small can create a snowball effect that puts homeownership within reach in just a few years.”

Discretionary cuts versus a structural affordability crunch

Even a perfectly disciplined budget, however, would not have solved what housing economists described as a structural affordability crisis. The National Association of Realtors reported in November that first‑time buyers made up just 21% of all purchasers between mid‑2024 and mid‑2025, an all‑time low, while the median age of a first‑time buyer climbed to 40.

“The historically low share of first‑time buyers underscores the real‑world consequences of a housing market starved for affordable inventory,” Jessica Lautz, NAR deputy chief economist and vice president of research, said.

“The share of first-time buyers in the market has contracted by 50% since 2007—right before the Great Recession. The implications for the housing market are staggering. Today’s first-time buyers are building less housing wealth and will likely have fewer moves over a lifetime as a result.”

Gen Z and millennial homeownership rates flattened in 2024 despite rising household formation, as typical monthly payments pushed toward $2,800 and entry‑level inventory remained scarce. Another survey‑driven feature found nearly two‑thirds of Gen Z adults feared they would never afford a home at all, with three‑quarters saying the cost of living made saving for a down payment impossible.

Lifestyle creep meets lender reality

Lucas said the analysis was aimed less at blaming “lattes and Netflix” and more at illustrating trade‑offs.

“What is true is that nearly everyone has experienced lifestyle creep,” the report noted, pointing to the gradual accumulation of streaming services, ride‑hailing, and impulse shopping.

Redirecting even half of the modeled $641 per month would have generated about $3,800 a year – still enough to move the needle in many lower‑cost markets.

Although a 5% down payment is not required for every mortgage program, the report said it often helped buyers qualify for better pricing and lower mortgage insurance costs. Any additional savings could be directed to reserves, furnishings or early repairs once they owned a home, Lucas said.

Front‑line loan officers described a similar tension between lifestyle and access. “They’re nervous, anxious, unprepared,” Northern California mortgage specialist Risha Kilaru said of Gen Z borrowers, adding that many needed help mapping everyday spending decisions to long‑term goals.

The Mortgage Research Network model relied on averages for both spending and home prices, and assumed renters could reallocate those dollars consistently over several years – conditions that may not hold for every household or market.

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.