Pass this article on to clients with questions about reverse mortgages, or scroll to the bottom to read the latest reverse mortgage news!

The most common term for reverse mortgages in the UK is equity release.

A reverse mortgage is a loan that lets you get money from your home equity—and without having to sell your home. In the UK, you must be at least 55 years to take out a reverse mortgage. If you are that age, and you decide a reverse mortgage is the best move for you financially, you can borrow between 40% or 60% of the current value of your property.

This article will teach you the finer points of how you can get a reverse mortgage in the UK. For the mortgage professionals who typically come to our site, this can be an excellent article to send along to any client with questions about reverse mortgages.

In the UK, a reverse mortgage is for homeowners who are typically 55 years of age or older who want to release some of the equity they have accrued in their property. While there is no pre-paid term, the loan that you take out against the equity in your home is repaid when you either pass away, move into a long-term facility, or sell the house.

Additionally, there are usually no monthly repayments; instead, the interest is included in and added to the initial capital when you repay the loan.

Unlike a standard mortgage application, reverse mortgage applications do not require the typical affordability assessment and credit checks. The reason these are foregone is because your property is used as the security for the loan.

If you own a home outright and it is your main residence in the UK, you can usually take a reverse mortgage out. Most of the time, a lifetime mortgage—which is the preferred term for a reverse mortgage in the UK—can be taken out if you live in the UK for at least six months of the year.

There is also a flexible reverse mortgage option, which allows the borrower to make monthly repayments. Typically, a flexible mortgage is used by homeowners who are still employed, who are relatively young, and who want to release equity while protecting their children’s inheritance.

With a flexible reverse mortgage, the balance of your account will not increase if you repay the interest each month. Instead, when the time comes, you will only need to repay the initial amount borrowed.

In the UK, you usually need to be at least 55 years old to take out a lifetime mortgage/reverse mortgage. Some lenders do, however, have a higher minimum age. In fact, there are also lenders that have a maximum age cap at the time of taking out the reverse mortgage.

While the most common age cap is 85, there are also lenders whose age cap is as high as 95 years old. There are no upper limits on the end of the loan due to the nature of the type of borrowing.

The most you can borrow using a reverse mortgage depends on various factors, including:

Reverse mortgages, or lifetime mortgages, benefit retirees who do not have a lot of cash savings or investments, but who do have wealth built up in their properties. Reverse mortgages let you turn your asset into cash, which you can then use to pay for expenses that come with retirement.

There are, however, other benefits. Here is a list of some of the advantages of taking out a reverse mortgage in the UK:

As with any mortgage deal, it is important to weigh the disadvantages of reverse mortgages as well. The biggest downside is that it can become quite costly. If you continue to live for a significant period after taking out the reverse mortgage, the interest can accumulate and affect the value of your estate.

Here are some of the disadvantages of getting a reverse mortgage in the UK:

There are multiple factors that determine how much money you can get from a reverse mortgage in the UK. Here is a list of what will factor into your total loan amount:

Let’s take a closer look at the factors that determine how much money you get from a reverse mortgage:

The value of your property is one of the most significant factors when determining how much money you can borrow with a reverse mortgage. Usually, you can get between 40% and 60% of the appraised value of the property. The more your property is worth, the more funds you will potentially be able to access.

Your lender may require that you use the proceeds from your reverse mortgage to pay off any remaining balance on your main mortgage. That means that if your current mortgage balance is significant, the money you can get from your reverse mortgage will be limited.

Another factor is the type of payments you choose. A line of credit, which lets you withdraw money over a period, like a credit card, will likely offer you more money. Lump-sum payments, meanwhile, offer the smallest amount. If you choose monthly payments, you will be offered payments that fall in the middle of a line of credit and a lump sum.

Market interest rates will impact how much money your reverse mortgage will get you. If interest rates are low, there will be less interest added to your loan over the long term. In this case, lenders usually offer you a higher loan amount up front. If, on the other hand, rates are high, loan amounts are more likely to be lower.

Just like more traditional mortgages, reverse mortgages also have closing costs, which you can pay out of the proceeds of the loan. Therefore, the higher the closing costs, the less you will be able to borrow. It is another reason that you should shop around for your reverse mortgage.

Read more: Closing costs in the UK that home buyers should know

Many lenders in the UK offer reverse mortgages, each with its own criteria, which includes the following:

Choosing the best reverse mortgage for you is more important than a headline rate, even if rates significantly vary.

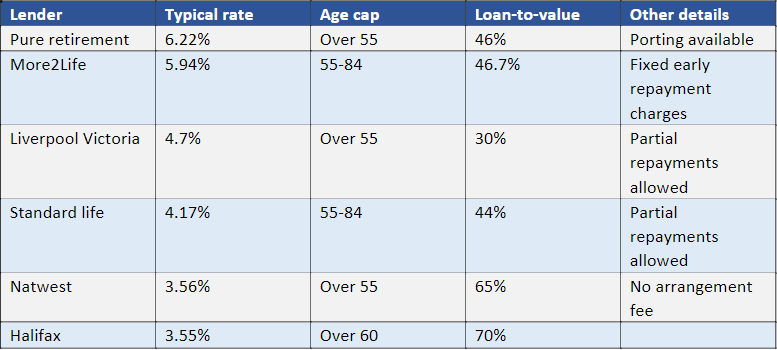

To give you an idea of typical rates and age caps, following graph is a breakdown of which lenders offer reverse mortgages in the UK:

Prior to taking out a reverse mortgage, it is important to understand what you are getting into. Here is a list of questions that you can ask your lender about reverse mortgages in the UK:

A reverse mortgage is essentially a loan that you can take out on your home while still living in it. Now that you know which lenders offer reverse mortgages in the UK, as well as which questions to ask them, you can decide whether it is the right move for you. Remember: while there are many benefits, there are also risks.

Before committing yourself to getting your reverse mortgage, do your research, such as checking in on what the best mortgage lenders in your area can do for you.

Scroll down to see al the latest reverse mortgage news in the UK!

The biggest mortgage lenders in the world are global banking giants. In this article, we ranked the 10 largest mortgage banks by their market capitalization