Net lending hit £13 billion in March despite drop in approvals

Mortgage borrowing saw a significant increase in March, according to the Bank of England’s latest Money and Credit report, highlighting a rebound in housing market activity despite a decline in purchase approvals.

Net mortgage borrowing rose to £13 billion in March, up from £3.3 billion in the previous month. Annual growth in net mortgage lending accelerated to 2.7% — the fastest pace since March last year.

Gross mortgage lending also picked up, climbing to £39.9 billion from £24.9 billion in February. At the same time, gross repayments rose to £23.7 billion, the highest level since October 2022.

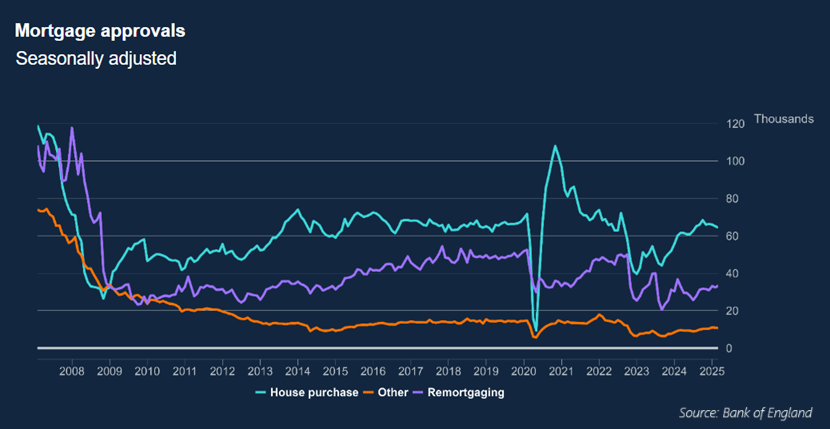

Despite the strong lending figures, the latest BoE figures showed that the number of approvals for house purchases fell for a third straight month. There were 64,300 approvals in March, down by 800 from the previous month. However, remortgage approvals, which only include deals involving a switch to a new lender, rose by 1,000 to 33,400.

Interest rates on new home loans edged lower. The average rate paid on new mortgages dipped slightly to 4.5% in March, down three basis points from February. Rates on existing loans also eased, falling to 3.84% from 3.87%.

“The stampede for house buyers to complete on property transactions before the Stamp Duty threshold change led to a surge in mortgage borrowing in March,” said Richard Pinch (pictured left), senior risk director at financial services consultancy Broadstone. “Mortgage borrowing increased by 292%, or £9.7 billion, through the month to reach its highest level since before the conclusion of the stamp duty holiday introduced in the teeth of the global pandemic.

“The wider picture, however, is not quite as rosy as April data shows house prices slumping quicker than expected which is backed up by the Bank of England’s figures finding that mortgage approvals for house purchases – a proxy for future borrowing – decreased for a third consecutive month. There is an element of a bring-forward effect in these numbers from the stamp duty change which will most likely impact next month’s figures as well.”

“A lack of any further incentives for first time buyers in the recent Spring Statement will likely lead to a drop-off in mortgage applications and approvals in the coming months as affordability challenges bite and first-time buyers take time to assess their plans,” added Emma Cox (pictured centre), managing director of real estate at specialist lender Shawbrook.

However, for Stephanie Daley (pictured right), director of partnerships at mortgage advisor Alexander Hall, buyer market activity will continue to strengthen as the year progresses.

“We’ve already seen many lenders act in anticipation of a May base rate reduction, with some offering fixed rate deals with sub-4% interest rates,” Daley said. “However, this means that should the base rate fall next week, there’s no guarantee that mortgage rates will follow suit, as these lenders have already factored this into existing offers.

“As always, the best course of action for homebuyers and remortgagers is to get a whole of market view in order to ensure that the deal being offered to them is the best one available for their individual circumstances.”

Any thoughts on the figures revealed in this Bank of England report? Share them with us by leaving a comment in the discussion box at the bottom of the page.