Two- and five-year fixed deals drop slightly; gap between terms narrows further

The pace of mortgage rate cuts in the UK decelerated in June, according to Moneyfacts’ latest Treasury Report, which noted only modest declines in average fixed rates.

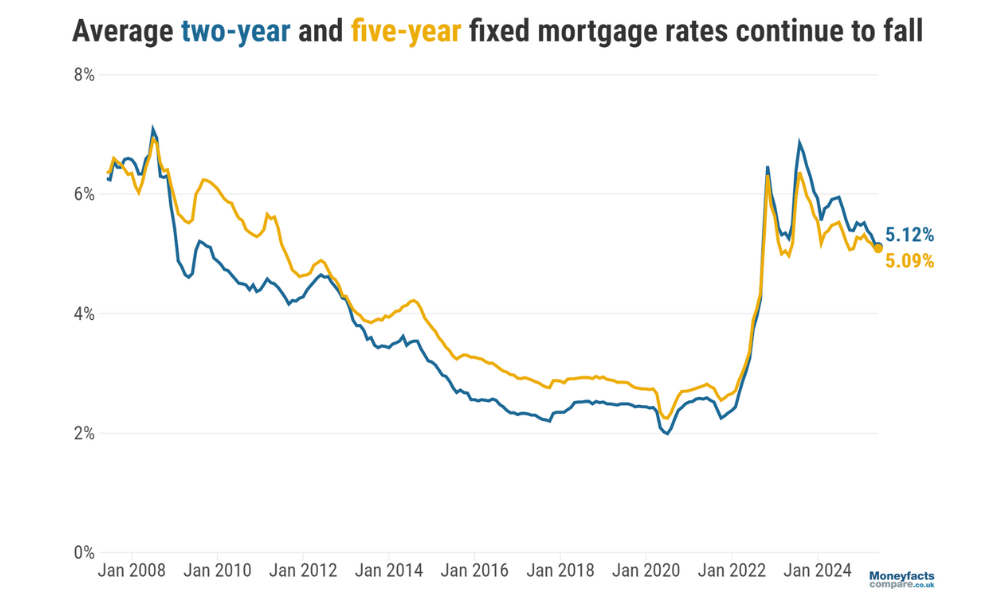

Data showed that the average two-year fixed mortgage rate decreased by just 0.06 percentage points to 5.12%, while the five-year equivalent slipped by 0.01 points to 5.09%. These are much smaller moves compared to May’s drops of 0.14 and 0.08 points respectively.

The two-year fixed rate average is now slightly above the five-year fix’s, with a margin of just 0.03 percentage points — its narrowest since October 2022 when the fixed rate curve inverted.

On a broader timeline, the two-year rate is down 0.81 points since June 2024, having fallen from 5.93%. The five-year rate declined by 0.41 points over the same period.

The typical shelf-life of a mortgage deal shortened to 17 days in June, down from 19 days the previous month, marking its lowest point since March.

Total product availability dropped to 6,843, down month-on-month, although still higher than the 6,629 recorded a year ago.

Variable rates also shifted, with the average two-year tracker falling below 5% for the first time since March 2023, now at 4.91%. Standard variable rates (SVRs) also declined to 7.48%, easing from a high of 8.19% seen in late 2023.

“Lenders were busy repricing their mortgage ranges during May, but the margins of cuts to the overall two- and five-year fixed average rates were much smaller than seen a month prior,” said Rachel Springall (pictured), finance expert at Moneyfacts. “While the Bank of England base rate cut last month could be celebrated by borrowers, lenders can move rates in the opposite direction if swap rates rise. This can also cause opposing rate moves on longer-term fixed versus short-term, depending on the divergence of swap rates.”

Despite the slight reduction in available products, Springall said options remain relatively strong, especially at higher loan-to-value (LTV) tiers. The shortened deal shelf-life may pressure borrowers approaching refinancing to act quickly.

“First-time buyers, on the other hand, may feel it’s not quite the right time to get a mortgage if they are struggling with the cost of living,” she said. “Lenders have been reviewing their stress testing over recent weeks, so some first-time buyers who have struggled with affordability criteria might be surprised to find they could now be eligible.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.