Land Registry data shows fast resales fell to 1.5% in 2025, with average post-tax gains more than halved over a decade

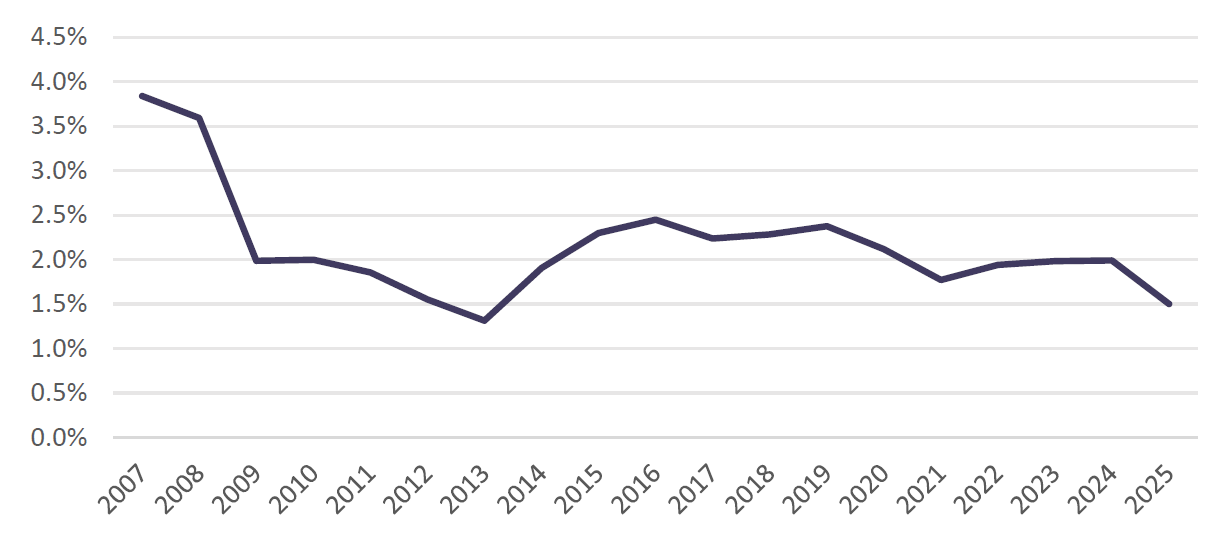

The share of homes in England and Wales bought and resold within 12 months fell to 1.5% in 2025, down from 2% in 2024, based on Land Registry data.

The number of flipped homes has declined since the second home stamp duty land tax (SDLT) surcharge was introduced in 2016, falling from 21,520 in 2016 to 10,570 in 2025. The surcharge started at 3% and rose to 5% in 2024.

Flipped properties as a share of all transactions (England and Wales) Sources: Hamptons, Land Registry

Sources: Hamptons, Land Registry

Average post-SDLT gross profit — resale price minus purchase price after deducting stamp duty paid — fell from £36,500 in 2015 to £16,390 in 2025, a 55.1% drop. The figures exclude refurbishment costs.

In 2025, 73.3% of flipped homes made a gross profit, but that fell to 58.7% after stamp duty. SDLT accounted for 43% of gross profit, or about £12,400 per sale. Profits improved during the pandemic stamp duty holiday but have since weakened.

Profitability has fallen most in southern regions, where stamp duty costs are higher and house price growth has been weaker.

The South West recorded the sharpest fall in average post-SDLT profit, down 80.3% since 2015. By 2025, stamp duty absorbed 71% of average gross profit in the region.

The North East recorded the strongest percentage returns in 2025 at 36.4% and was the only region where post-SDLT profits rose over the decade, up 27% since 2015. Stamp duty averaged around £6,000 per flipped property in 2025 and represented 26.0% of gross profit, compared with 45.6% and about £30,000 in London.

Seventeen percent of flips in the North East were bought for £40,000 or less and incurred no stamp duty. The region also had the highest share of flipped transactions, at 3% in 2025. Hartlepool had the highest share nationally at 7.4%, compared with 0.5% in Brentwood.

Completed flips as a share of total transactions by region in 2025 Sources: Hamptons, Land Registry

Sources: Hamptons, Land Registry

Homes bought for under £100,000 were most likely to make a profit in 2025, with 86% doing so. This fell to 28% for purchases above £350,000. Average returns were 45.8% below £100,000 and negative above £350,000. Most flips (88.8%) were bought for less than £350,000.

“Flipping is no longer the profitable venture it once was,” said Aneisha Beveridge (pictured right), head of research at Hamptons. “There was a time when rundown properties could be bought cheaply, refurbished, and resold at a healthy margin. Today, however, second home stamp duty absorbs nearly half of all gross profits, significantly eroding returns.

“Flipping is no longer the profitable venture it once was,” said Aneisha Beveridge (pictured right), head of research at Hamptons. “There was a time when rundown properties could be bought cheaply, refurbished, and resold at a healthy margin. Today, however, second home stamp duty absorbs nearly half of all gross profits, significantly eroding returns.

“The surcharge was not primarily intended to penalise ‘house flipping’; its primary aim was to support first-time buyers. While it has largely succeeded in that goal, it has left flipping unviable across much of the South of England. These projects deliver much-needed move-in-ready homes, sparing buyers the financial risks and expertise to undertake major works themselves.”

Beveridge, however, pointed out that stamp duty is only part of the challenge. “Falling house prices across many Southern markets have squeezed returns further, while the cost of materials and labour have risen sharply since the pandemic,” she said. “Even before factoring in stamp duty, refurbishment budgets now stretch much further than they once did, pushing profit margins to their thinnest levels in over a decade.

“In contrast, the North - particularly the North East - has remained far more resilient. Lower entry prices keep stamp duty bills modest, meaning more scope to add value through refurbishment. Combined with strong local house price growth, this has created a rare pocket of the country where flipping can still deliver healthy returns.

“Unless a flip is supported by strong underlying house price growth, turning a profit is becoming increasingly difficult. That said, investing in relatively cheaper property in an area where house price growth is strong can still yield solid returns.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.