Higher inflation risks from the Iran conflict are feeding into pricing and affordability

The International Monetary Fund (IMF) has lowered its forecast for UK economic growth in 2026, warning that the conflict involving Iran is weighing on prospects across advanced economies and could keep inflation risks elevated.

In its latest World Economic Outlook, the IMF cut its UK growth forecast for the year to 0.8% from 1.3%, the sharpest downgrade among the G7, as it assessed the fallout from the Iran war.

The IMF said the global economy is being tested after last year’s trade and tariff disruption, and that a wider or longer conflict could further worsen the outlook. It also cautioned that the US-Israel war on Iran risks creating an “energy crisis of an unprecedented scale” that could push the global economy towards recession.

In an earlier separate assessment, the Organisation for Economic Co-operation and Development (OECD) has lowered its forecast for UK growth this year to 0.7%, from 1.2% previously, saying that Britain is likely to be hit harder by the Middle East conflict than any other major economy.

Susannah Streeter, chief investment strategist at investment platform Wealth Club, said the downgrade on the UK growth forecast added to the government’s difficulties in lifting growth. “The IMF downgrade is a fresh blow to Chancellor Rachel Reeves and the government’s elusive search for growth,” she said.

“The UK is set to be battered by hot oil prices, an energy bill crisis and a tightening of consumer spending. The economy was already flatlining even before war erupted in the Middle East, and now there is little means of resuscitation available given that interest rates look set to ramp up to curb inflation.

“One to two interest rate increases are now being priced into financial markets instead of the scary three to even four hikes temporarily forecast, but it’s still going to be tough going ahead if borrowing costs rise further. Plans for a big bang of home construction with 1.5 million new dwellings targeted by the government have turned into more of a whimper. Property companies have scaled back ambitions as the Middle East crisis has hurt demand, and high uncertainty lingers.

“The UK is stuck in a stagflation scenario and risks of a recession are rising fast.”

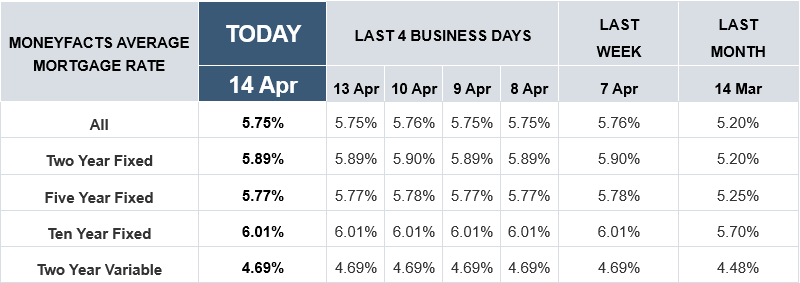

Financial comparison website Moneyfacts said the shift in inflation expectations has already pushed up mortgage pricing, with knock-on effects for affordability and for borrowers approaching the end of fixed-rate terms.

“The conflict in Iran quickly upended rate expectations and sent borrowing costs skyrocketing as money markets adjusted to substantially higher inflation expectations which is set to further squeeze UK households,” said Adam French (pictured right), head of consumer finance at Moneyfacts.

“The conflict in Iran quickly upended rate expectations and sent borrowing costs skyrocketing as money markets adjusted to substantially higher inflation expectations which is set to further squeeze UK households,” said Adam French (pictured right), head of consumer finance at Moneyfacts.

“Typical mortgage rates have already rocketed to meet these forecasts, with two-year fixes increasing by more than 100 basis points from 4.84% to 5.89% in little over a month since the conflict began and five-year fixes up by over 80 basis points, from 4.96% to 5.77%.

“The cheapest deals available to borrowers have moved dramatically too, the lowest two-year fixed rate available to borrowers across the UK at 60% LTV has increased by over 100 basis points from 3.51% to 4.66%.”

French pointed out that the additional cost could be significant for many borrowers. “Someone taking out a typical two-year fix will find it costs hundreds of pounds more per month on average compared to just a few weeks ago,” he said.

“However, the real payment shock will be felt by those coming off older five-year deals, where rates have more than doubled, pushing up repayments by many hundreds of pounds per month.”

| Mortgage rate changes (Remortgage scenarios) | |||||

|---|---|---|---|---|---|

| Mortgage term & LTV | Old rate | New rate (2-yr fix) | Difference | Monthly difference | Annual difference |

| Remortgage from a 2-year fix – average rate | 5.80% | 5.89% | +9 bps | +£14 | +£168 |

| Remortgage from a 2-year fix – lowest rate | 4.46% | 4.79% | +33 bps | +£47 | +£564 |

| Remortgage from a 5-year fix – average rate | 2.77% | 5.89% | +312 bps | +£438 | +£5,256 |

| Remortgage from a 5-year fix – lowest rate | 1.23% | 4.79% | +356 bps | +£463 | +£5,556 |

| Source: Moneyfactscompare.co.uk. Note: Two-year average mortgage rate and lowest rate available to remortgage customers as per 1 April 2024. Five-year average mortgage rates and lowest rate available as per 1 April 2021 compared to cost of borrowing £250,000 over 25 years to average and lowest two-year fixed rate available to remortgage borrowers as per 14 April 2026. | |||||

For lenders and brokers, the combination of weaker growth and higher rates typically raises the risk of tighter affordability, slower purchase activity and elevated remortgage churn, while also increasing the chance of arrears among stretched households.

The IMF said the balance of risks remains to the downside, including renewed trade tensions and deeper geopolitical fragmentation, and argued that credible policy frameworks and international cooperation would be needed to navigate the shock.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.