Borrowers urged to review options carefully

Fixed mortgage fees have increased since 2020, while some cost-saving incentives have become less common, according to analysis by Moneyfactscompare.co.uk.

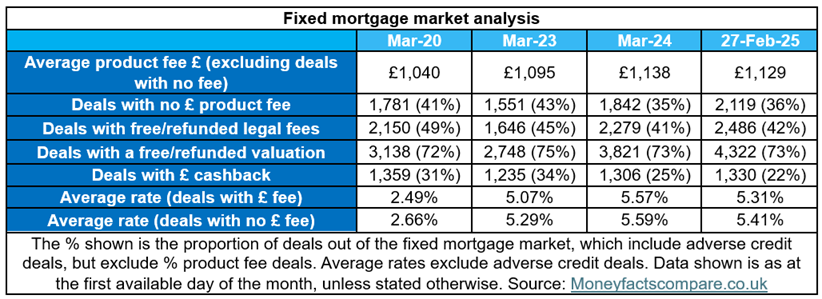

Borrowers looking to refinance this year may face higher costs beyond interest rates as data shows that the average product fee on fixed-rate mortgages — excluding no-fee deals — now stands at £1,129, up £89 from March 2020. Although the figure has dropped slightly from March 2024, it has remained above £1,000 since mid-2017.

The proportion of fixed rate mortgage deals offering free or refunded valuations has increased slightly to 73%, up from 72% in early 2020.

However, deals that include free or refunded legal fees have dropped from 49% to 42% over the same period. Cashback incentives have also declined, with 9% fewer deals offering this benefit compared to four years ago.

“Borrowers who locked into a cheap fixed rate in 2020 and are looking to refinance will find mortgage fees have been on the rise,” said Rachel Springall (pictured), finance expert at Moneyfactscompare.co.uk. “Outside of headline-grabbing low rates, borrowers need to check the overall cost of any mortgage, which includes any fees or cost-saving incentives.

“The best deal depends on someone’s circumstances and how much they need to borrow; someone with a larger debt would typically chase a lower rate, whereas those looking to avoid upfront costs would consider fee-free deals and incentives.”

Springall also pointed out that while fewer mortgage deals now offer cashback, a significant portion still includes valuation and legal fee incentives.

“More often than not, borrowers can find a deal with a free or refunded valuation incentive, and just under half of all fixed deals will cover legal fees,” she said. “Those looking to remortgage will likely want to keep costs down and refinance without too much effort, so mortgage bundles are a great choice to avoid the worries of covering upfront fees.”

For first-time buyers, Springall suggested that cashback deals could be particularly beneficial, as many may have already spent much of their savings on a deposit and other homebuying costs. She advised borrowers to compare their options carefully and seek professional guidance before committing to a new mortgage deal.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.