Northern regions lead in fast-growing first-home prices

First-time buyers across Britain are experiencing a surge in property prices, with new analysis revealing that prices paid for their initial homes have risen 2.5 times faster than those paid by existing homeowners since the start of 2025. This escalation coincides with record levels of mortgage lending to first-time buyers, as confirmed by the Bank of England.

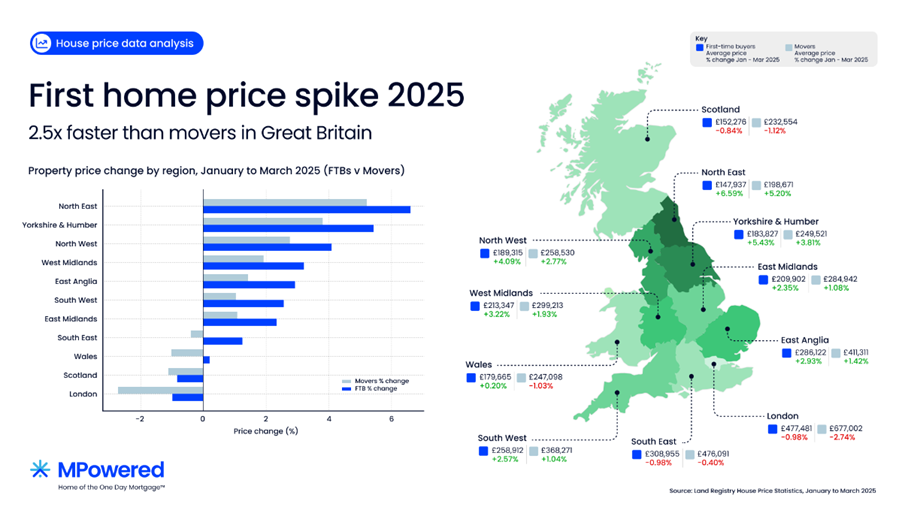

According to data analysed by mortgage lender MPowered, the average price for a first home reached nearly £231,000 in March, marking an increase of £15,350 from March 2024. This trend highlights a sustained period of growth for new entrants to the property market; since 2020, the average price of a first home in Britain has climbed by 27.1%, outstripping the 25.2% rise for movers.

In just the first two months of this year, the average price paid by first-time buyers increased by £4,772, a 2.1% rise, compared to a mere 0.8% for buyers who already own a home. This disparity underscores the unique pressures facing the first-time buyer segment.

Northern regions record steepest increases

This trend is particularly pronounced in northern England. First-time buyers in Yorkshire and the Humber paid an average of £9,467 more for their homes between January and March, while those in North East England saw a £9,151 increase, representing a 6.6% jump in two months. The North East has experienced a substantial 15.1% rise in average first home prices over the past year, and an “incredible” 40% increase over five years.

East Anglia also saw a notable jump, with prices for first homes rising by £8,148, a 2.9% increase. Conversely, London bucked the trend, experiencing price falls across the board; however, first-time buyers in the capital saw a smaller average decrease of £4,742 compared to the £19,048 drop for existing homeowners.

Peter Stimson, director of mortgages at MPowered, attributes this boom to a combination of lower mortgage interest rates and a relaxation of lending criteria. “Buyers are routinely being offered loans up to 20% larger than they were a year ago,” Stimson noted. He explained that “lower stress tests have replaced the stamp duty deadline as the fuel for a first-time buyer boom,” allowing first-time buyers, who typically borrow near their maximum, to push prices higher.

While a rush to beat the stamp duty deadline, which concluded at the end of March, contributed to early 2025 inflation, MPowered’s analysis suggests that prices for first homes could continue their upward trajectory, driven by the ongoing flexibility in lending.

What are your thoughts on the first-time buyer price surge in Britain? Share your insights below.