Base rate expected to drop to 3.75%

The chief executive of the UK's largest mortgage lender expects the Bank of England (BoE) to reduce interest rates twice more before the end of 2025, potentially lowering the base rate to 3.75%.

Speaking to Sky News, Lloyds Banking Group CEO Charlie Nunn said two further rate reductions are likely, with the first expected to be a 0.25 percentage point cut next month. Investors have already priced in two cuts this year.

The BoE is also widely expected by analysts to lower its base interest rate to 4% when officials meet next month, with markets pricing in more than an 80% chance of a 25-basis-point cut. Bloomberg Economics’ Bespeak model suggests policymakers are adopting a more dovish stance, influenced by signs of slack in the UK labour market.

However, central bank governor Andrew Bailey has reinforced the preference for a gradual approach to monetary easing and cautioned that an August rate cut is not guaranteed, citing persistent inflation concerns.

Late last year, the bank said it could cut interest rates four times in 2025 if economic conditions allowed. Global bank Goldman Sachs also predicted that the Bank of England might implement up to six interest rate cuts by the middle of next year.

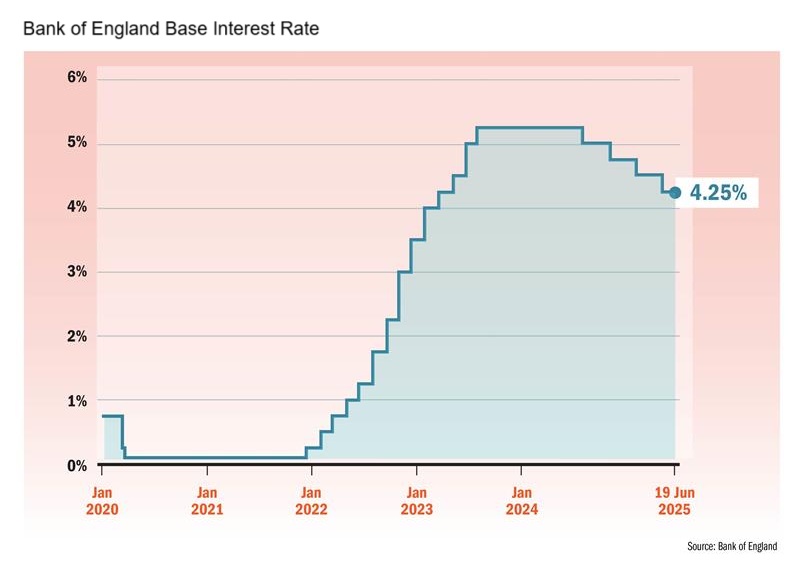

So far, the BoE has made two cuts this year — one in February and another in May — each by 0.25 percentage points, bringing the base rate to 4.25%. The central bank left the rate unchanged in June.

Changes to the base rate have an immediate effect on those with tracker and standard variable rate (SVR) mortgages. About 600,000 homeowners currently have tracker mortgages. According to UK Finance, a 0.25 percentage point change in the base rate translates to about a £29 monthly adjustment for tracker mortgage holders and around £14 for those on SVR deals. For example, a 0.50 percentage point increase would add nearly £58 to a tracker mortgage and about £28 to an SVR mortgage each month. A 0.50 percentage point cut would lower payments by similar amounts. Fixed rate mortgage holders, however, do not see any immediate change in their payments, as their rates are locked in for the duration of their deal.

While most borrowers are on fixed rate deals and are shielded from immediate changes, future mortgage rates are influenced by shifts in the base rate. Despite expectations of rate cuts, mortgage rates remain significantly higher than they were for much of the past decade. As of July 16, the average two-year fixed mortgage rate stood at 5.03%, while the average five-year fixed rate was 5.01%, according to price comparison webiste Moneyfacts. The typical two-year tracker rate was 4.91%. This means that many homebuyers and those looking to remortgage are facing much higher costs than if they had secured a loan several years ago.

Looking ahead, around 800,000 fixed rate mortgages with interest rates of 3% or below are set to expire each year, on average, until the end of 2027. Borrowers coming off these deals are expected to see a sharp increase in their monthly payments.

“We helped 34,000 first-time buyers in the first half [of the year] alone, 64,000 last year,” Nunn said. “And of course, it was driven by the stamp duty changes in Q1. So Q2 was a bit slower, but we continue to see real strength in customers wanting to buy homes and take mortgages. So we think that will continue,” said Charlie Nunn, chief executive officer at Lloyds Banking Group.

The comments follow Lloyds’ latest financial results, which showed half-year profits of £3.5 billion, surpassing analyst expectations. The bank reported increased lending and deposits, with higher interest rates boosting income from loans.

The Bank of England’s base rate, still relatively high at 4.25%, has raised borrowing costs for households and businesses. Over the past six months, Lloyds’ net interest margin — the gap between what it earns on loans and pays on deposits — has widened. The banking giant posted a 14% increase in gross new mortgage lending to £5.6 billion.

While Nunn acknowledged the profit growth due to a larger share of the mortgage and small business lending markets, he was wary about further tax increases on financial services.

In an interview with The Guardian, Chancellor Rachel Reeves did not rule out the possibility of tax increases later in the year, stating there were “costs” to watering down the welfare bill.

“I’m not going to [rule out tax rises], because it would be irresponsible for a chancellor to do that,” Reeves said. “We took the decisions last year to draw a line under unfunded commitments and economic mismanagement. So we’ll never have to do something like that again. But there are costs to what happened.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.