Rates seem to have plateaued for now, says finance expert

After weeks of mortgage rate increases driven by market volatility linked to the Iran conflict and renewed inflation concerns, several major lenders have cut interest rates this week, with HSBC and Halifax repricing core mortgage ranges from tomorrow, 17 April.

HSBC UK has announced reductions across a broad set of mortgage products, including first-time buyer, home mover and remortgage business, alongside buy-to-let purchase and buy-to-let remortgage products.

HSBC said the cuts apply across multiple loan-to-value (LTV) tiers, including higher-LTV options, and extend to selected energy efficient home propositions for properties rated EPC ‘A’ or ‘B’.

Within residential lending, the reductions include fixed-rate “Fee Saver” and “Standard” products at a range of LTVs, as well as selected high-value and Premier-exclusive fixes. HSBC’s remortgage range is also being reduced, including its remortgage cashback offering and the equivalent energy efficient variants.

In buy-to-let, the high street lender is cutting rates across purchase and remortgage fixed-rate deals, including products at 60% to 80% LTV, as well as selected fee and non-fee options. International residential and international buy-to-let ranges are also included in the repricing.

Against the backdrop of the move, market analysts point to a more stable – though still fragile – funding environment. “Rising mortgage rates seem to have plateaued for now,” said Adam French (pictured right), head of consumer finance at price comparison site Moneyfacts.

Against the backdrop of the move, market analysts point to a more stable – though still fragile – funding environment. “Rising mortgage rates seem to have plateaued for now,” said Adam French (pictured right), head of consumer finance at price comparison site Moneyfacts.

“Product numbers have also been steadily improving; 809 deals have returned to the market since it hit a low of 5,856 available products on 24 March. However, this is still 973 (12.7%) fewer than before the conflict in Iran began.”

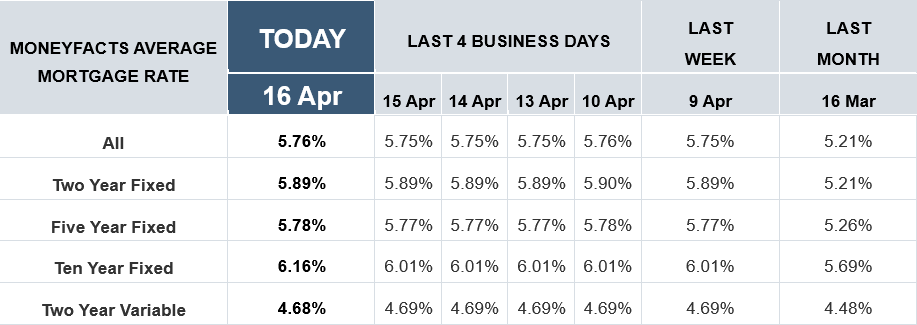

According to data from Moneyfacts, the average two‑year fixed residential mortgage rate stood at 5.89% on Thursday, same as on the previous day. The typical five‑year fixed residential rate was 5.77%, the same level as on Wednesday.

At the beginning of March, the average two‑year fix was 4.83%, while the standard five‑year fixed deal was 4.95%.

French noted that money markets are now pricing in fewer base rate rises than a few weeks ago, with swap rates easing towards 4% from previous highs of about 4.4%.

“This has given several lenders, such as Santander, Atom bank and Skipton Building Society, the headroom to make a few meaningful cuts over the last few days,” he said.

“However, mortgage pricing is driven more by expectations than current rates and borrowers are still exposed to sudden shifts. Ongoing uncertainty in the Middle East and the looming threat of ‘Trumpflation’ mean the path to cheaper borrowing remains fragile.”

Nicholas Mendes (pictured right), mortgage technical manager at London broker John Charcol, said HSBC’s decision adds weight to signs that sentiment among major lenders is starting to improve. “HSBC is the latest lender joining TSB and Santander with rate reductions this week is another positive step, and probably the clearest sign yet that lender confidence is starting to come back,” he said.

Nicholas Mendes (pictured right), mortgage technical manager at London broker John Charcol, said HSBC’s decision adds weight to signs that sentiment among major lenders is starting to improve. “HSBC is the latest lender joining TSB and Santander with rate reductions this week is another positive step, and probably the clearest sign yet that lender confidence is starting to come back,” he said.

“What gives this move a bit more weight is that HSBC is one of the major high street lenders. When a lender of that size starts repricing, it does tend to give the wider market a nudge and adds to the sense that this could help kick start further reductions from other big names over the coming days. That is especially encouraging after the volatility of the last few weeks, where lenders were far more focused on protecting margins and managing risk than competing hard on price.

“It is also a broader move, covering areas including first-time buyer, home mover, remortgage and buy-to-let business, which makes it more meaningful than a small, isolated tweak to one corner of the range.”

Meanwhile, Halifax also confirmed changes to its mortgage range, including rate reductions of up to 0.35 percentage points on fixed-rate products for homemovers and first-time buyers.

Aaron Strutt (pictured right), product director at Trinity Financial, noted that the pace of repricing among large lenders appeared to be accelerating. “The big lenders really are lowering their rates now and the price cuts are getting more momentum,” he said.

Aaron Strutt (pictured right), product director at Trinity Financial, noted that the pace of repricing among large lenders appeared to be accelerating. “The big lenders really are lowering their rates now and the price cuts are getting more momentum,” he said.

“With HSBC, Santander, and now Halifax making some pretty chunky rate cuts, NatWest and Nationwide may well follow soon. Santander is giving Nationwide a bit more competition with its latest rate changes and it now has two-year fixes from 4.7%, three-year fixes from 4.78% and five-year rates from 4.76%.

“None of these really get anywhere near the tracker rate Halifax is still offering at 3.96% even if it does have a £1499 fee. These rate changes will come as a relief for many borrowers keen to get on the property ladder soon.”

Mendes, however, advised borrowers not to just sit back and wait for the perfect moment. “Anyone buying, remortgaging, or coming off a fixed rate in the next three to six months should be using this window to get prepared now,” he said.

“The best approach is usually to secure a rate early, then keep reviewing it. That gives protection if markets turn again but still leaves room to benefit if lenders continue trimming rates.

“That is where broker advice really matters, because in a market like this, best practice is not just finding the cheapest rate on the day. It is about securing an option, keeping flexibility, and being ready to move quickly if a better deal comes through before completion.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.