Momentum returns following post-stamp duty slowdown

The total value of outstanding residential mortgages in the UK edged up by 0.3% over the previous quarter and increased by 2.6 over the past year to £1.7 trillion, according to new figures from the Bank of England.

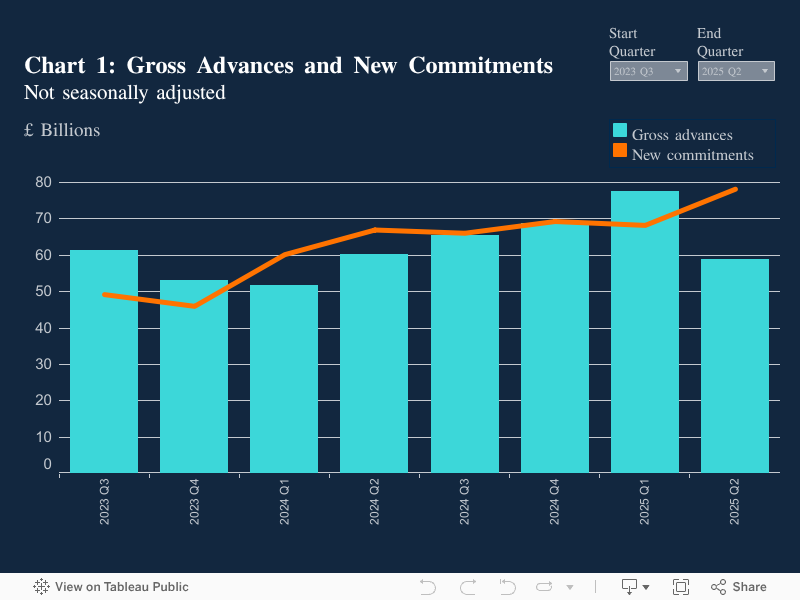

Gross mortgage advances fell sharply, dropping 24.2% from the previous quarter to £58.8 billion, the lowest level since the first quarter of 2024. This figure is also 2.4% below the amount recorded a year earlier.

In contrast, the value of new mortgage commitments – loans agreed but not yet advanced – rose by 14.6% to £78.2 billion, the highest since the third quarter of 2022. This marks a 16.8% increase year-on-year.

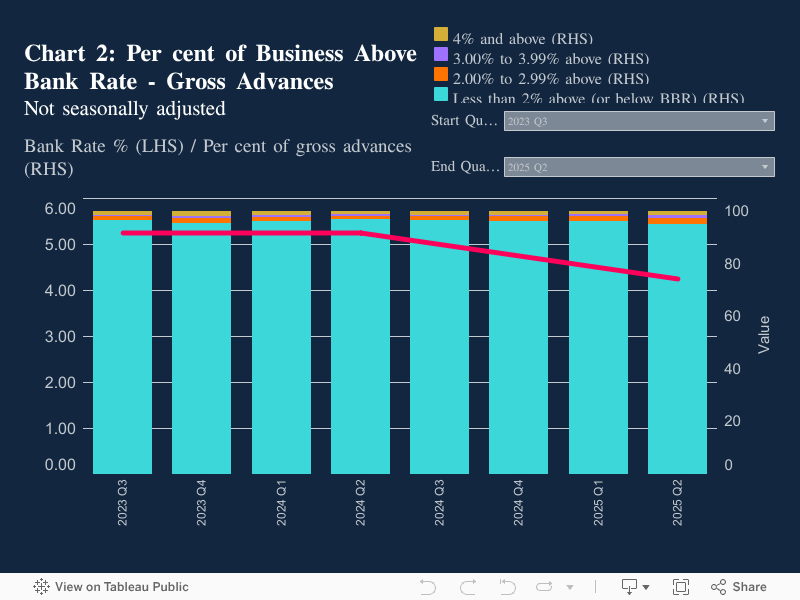

The latest Mortgage Lenders and Administrators Return also showed an increase in the proportion of gross advances with loan-to-value (LTV) ratios above 90%, which went up 0.4 percentage points to 7.1%, the highest share since the second quarter of 2008. This is also 1.1 percentage points higher than a year ago.

Meanwhile, lending to borrowers with high loan-to-income (LTI) ratios fell by 3.7 percentage points to 41.5%, the largest quarterly decline since early 2023, and one percentage point below last year’s level.

The share of gross advances for house purchase by owner-occupiers declined by 10.3 percentage points to 56%, the lowest since early 2024. This is 1.4 percentage points lower than a year earlier. Conversely, remortgage activity for owner-occupiers increased, with its share rising by 7.7 percentage points to 29%, the highest since the first quarter of 2024 and 0.4 percentage points above last year’s figure.

New arrears cases, as a proportion of all outstanding balances in arrears, dropped by 0.4 percentage points to 8.8%, the lowest since the start of 2022. The total value of outstanding mortgage balances with arrears decreased by 1.0% to £20.9 billion, the lowest since late 2023 and 4.6% below the level a year ago.

“The fall in value of gross mortgage advances reflects the end of the stamp duty concession whereby buyers brought forward purchases to the first quarter in order to take advantage of the savings to be made,” said Mark Harris (pictured top left), chief executive of mortgage broker SPF Private Clients. “However, the increase in value of new mortgage commitments to the highest level since Q3 2022, an indicator of future lending activity, indicates a growing resilience in the market, with borrowers confident to take on debt.

“There may no longer be a stamp duty concession available but several base-rate reductions – with the prospect of more to come – are easing affordability and enabling borrowers to plan ahead and commit to purchases. Although lenders have been easing criteria, the decrease in lending to borrowers with a high loan-to-income ratio suggests that borrowers are not overextending themselves and rushing to take out bigger loans.

“However, with lending to first-time buyers decreasing compared with the previous quarter, it remains tricky for those trying to get on the ladder for the first time, particularly if they don’t have help from the Bank of Mum and Dad.”

According to Karen Noye (pictured top centre), mortgage expert at financial services firm Quilter, while the market has been stalling somewhat during the period of adjustment post-stamp duty deadline, “we are beginning to see some momentum pick back up.”

“Stamp duty changes halted sales for a while, but as prospective buyers top up their savings to cover the increased costs, we will gradually see more return to the market,” she said. “However, supply-side challenges persist, and the housing market faces a difficult winter as affordability remains such a barrier.

“Budget rumours are also adding to the uncertainty and talk of new property-related taxes could result in would-be sellers putting their plans on hold until they have a clearer picture, so there is still a risk that the market stalls further in the near term.”

Richard Pinch (pictured top right), senior director of risk at independent financial services consultancy Broadstone, agreed, saying that “with households still facing higher living costs amid a fragile jobs market, there remains a risk that mortgage strain could return.”

“Lenders must continue supporting borrowers through these financial pressures while keeping a close eye on the longer-term outlook,” he added.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.